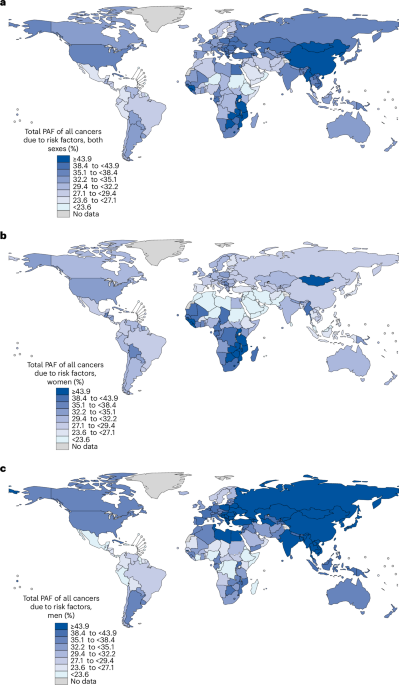

A global analysis published in Nature Medicine estimates that in 2022 some 7.1 million of 18.7 million new cancer cases (37.8%) were attributable to 30 modifiable risk factors, including 2.7 million cases in women (29.7%) and 4.3 million in men (45.4%). Smoking (15.1%), infections (10.2%) and alcohol (3.2%) were the largest contributors, with lung, stomach and cervical cancers accounting for nearly half of preventable cases; the share of preventable cancers varied markedly by region and sex. The findings underscore sizable preventive opportunities that could shift public-health spending, vaccination and screening programs, and environmental and occupational regulation — factors relevant to insurers, pharma/biotech exposure to prevention and treatment demand, and long-term health-care cost projections.

Market structure: Prevention and early-detection winners include large vaccine and biologics makers (MRK, GSK) and diagnostics/screening franchises (EXAS, GH, ILMN, GEHC) as payers and national programs shift funding from late‑stage treatment to prevention; tobacco (PM, MO, BTI) and premium alcohol (STZ) face structural demand headwinds—smoking accounts for ~15% of attributable cases so expect gradual volume decline over 5–15 years. Competitive dynamics: incumbents with integrated pipelines (MRK) and reimbursable, population-level screening products (EXAS Cologuard) gain pricing power; fragmented OTC/cessation markets are ripe for consolidation, compressing margins for smaller players. Supply/demand: demand for vaccines, HPV/HBV programs, and H. pylori eradication campaigns implies durable demand growth (mid‑single to low‑double digit CAGR in vaccine sales in targeted LMIC rollouts over 3–7 years) while antibiotic supply remains commoditized — capacity and cold‑chain logistics are potential bottlenecks. Cross-asset: stronger pharma cashflows support credit spreads tightening for IG pharma; sovereigns with rising healthcare burdens (EMs) may see wider spreads; USD likely to strengthen modestly if global public-health spending shifts to US/EU suppliers; commodity impact limited but sterile manufacturing inputs and cold‑chain materials may see price upticks. Risk assessment: Tail risks include rapid regulatory shifts (e.g., mandated HPV vaccination in large markets), vaccine safety scares or antibiotic resistance undermining H. pylori programs, and sudden policy reversals in LMICs; low‑probability/ high‑impact events could re‑rate entire sub‑sectors in 6–24 months. Time horizons: immediate (days) — negligible market moves; short (3–12 months) — policy announcements, WHO/CDC guidance, major trial readouts; long (2–7 years) — measurable declines in incidence and durable revenue ramps for prevention players. Hidden dependencies: reimbursement dynamics, screening guideline changes, and public trust drive uptake more than clinical efficacy; donor funding and procurement deals (Gavi, WHO) are binary catalysts. Catalysts: large national programs (China/India HPV/H. pylori policies), WHO guideline updates, and positive population eradication trial results within 12–36 months. Trade implications: Direct plays — establish 2–3% long positions in MRK and GSK (12–36 month horizon) to capture vaccine program rollouts; 1–2% long in EXAS (12–24 months) to play screening adoption; accumulate 0.5–1% short in PM/MO (3–7 year horizon) on secular volume decline. Pair trades — long EXAS (EXAS) 1% vs short PM 1% to capture differential secular growth; alternative pair: long GH 1% vs short ILMN 0.8% to play liquid biopsy commercialization vs infrastructure cyclicality. Options — buy 12–18 month LEAP calls on EXAS and GH (cost <3% portfolio each) or call spreads to cap premium if implied vol >40%. Rotate 5–10% from late‑stage oncology therapeutics into prevention/diagnostics over 6–24 months. Contrarian angles: Consensus underestimates time lag — prevention reduces incidence over years, so near‑term benefit accrues to diagnostics and screening (demand surge) more than immediate vaccine revenue; markets may be slow to reprice diagnostics innovators. Reaction risk: tobacco selloffs may be overdone if emerging‑market consumption declines slower than projected — keep short size capped and horizon multi‑year. Historical parallels: tobacco declines mirrored by long transition (decades) after policy shifts; HPV/HBV campaigns show measurable cancer reductions after 5–15 years, not months. Unintended consequences: higher screening can transiently raise oncology drug demand (overdiagnosis), benefiting therapeutics makers (BMY, LLY) contrary to pure prevention narratives — hedge positions accordingly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00