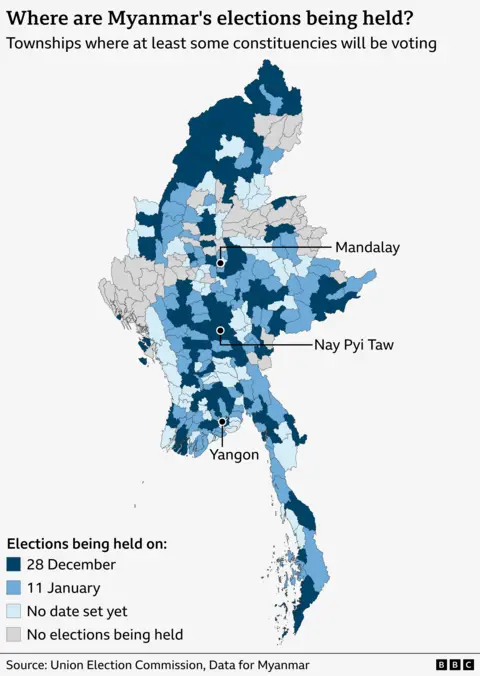

Myanmar's military junta is holding a phased election in 274 of 330 townships—with as much as half the country effectively excluded—after banning roughly 40 parties including Aung San Suu Kyi's NLD and jailing many opponents; results are expected around the end of January. Backed tactically by China and Russia, the junta has sought to reclaim territory via airstrikes amid a civil war that has killed thousands, displaced millions and been worsened by a March earthquake and international funding cuts. The vote and associated repression significantly raise political and sovereign risk for investors with exposure to Myanmar and create broader regional geopolitical and humanitarian tail risks.

Market structure: The junta election entrenches a high-risk, low-investment environment in Myanmar — immediate winners are Chinese/Russian equipment suppliers, illicit commodity middlemen and safe-haven assets (gold, USD, UST); losers are Myanmar domestic assets, frontier EM funds and regional tourism/consumer-facing businesses. Expect capital flight and MMK weakness (20–40% downside vs USD is plausible under sustained sanctions/refugee flows), pressuring local credit and trade finance. Risk assessment: Near-term (days–weeks) tail risks include major escalation of cross-border fighting or targeted sanctions disrupting China-backed energy projects (1–3% of regional gas flows) which would sharply widen credit spreads for ASEAN banks with Myanmar exposure. Medium-term (3–12 months) risks: protracted civil war lowering export volumes (timber, gas, minerals) and creating refugee-driven fiscal burdens for neighbours; long-term (1–3 years) risk is prolonged sanction networks isolating Chinese counterparties politically. Trade implications: Reduce/hedge frontier exposure, increase liquid safe havens and selective defense exposure. Volatility is likely to spike in EM equity and FX — use short-dated put spreads on EEM and rotate into GLD and USTs; consider small, diversified exposure to global defense names and regional winners (Singapore exporters) as a relative hedge. Contrarian angles: Consensus may over-penalize ASEAN high-quality exporters with no Myanmar revenue; look for idiosyncratic buying opportunities in Singapore-listed industrials and shipping that trade 10–25% off pre-crisis levels with limited direct Myanmar exposure. Also monitor rerating of Chinese state-owned contractors that could replace western firms — political risk creates both dislocation and concentrated winners.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.70