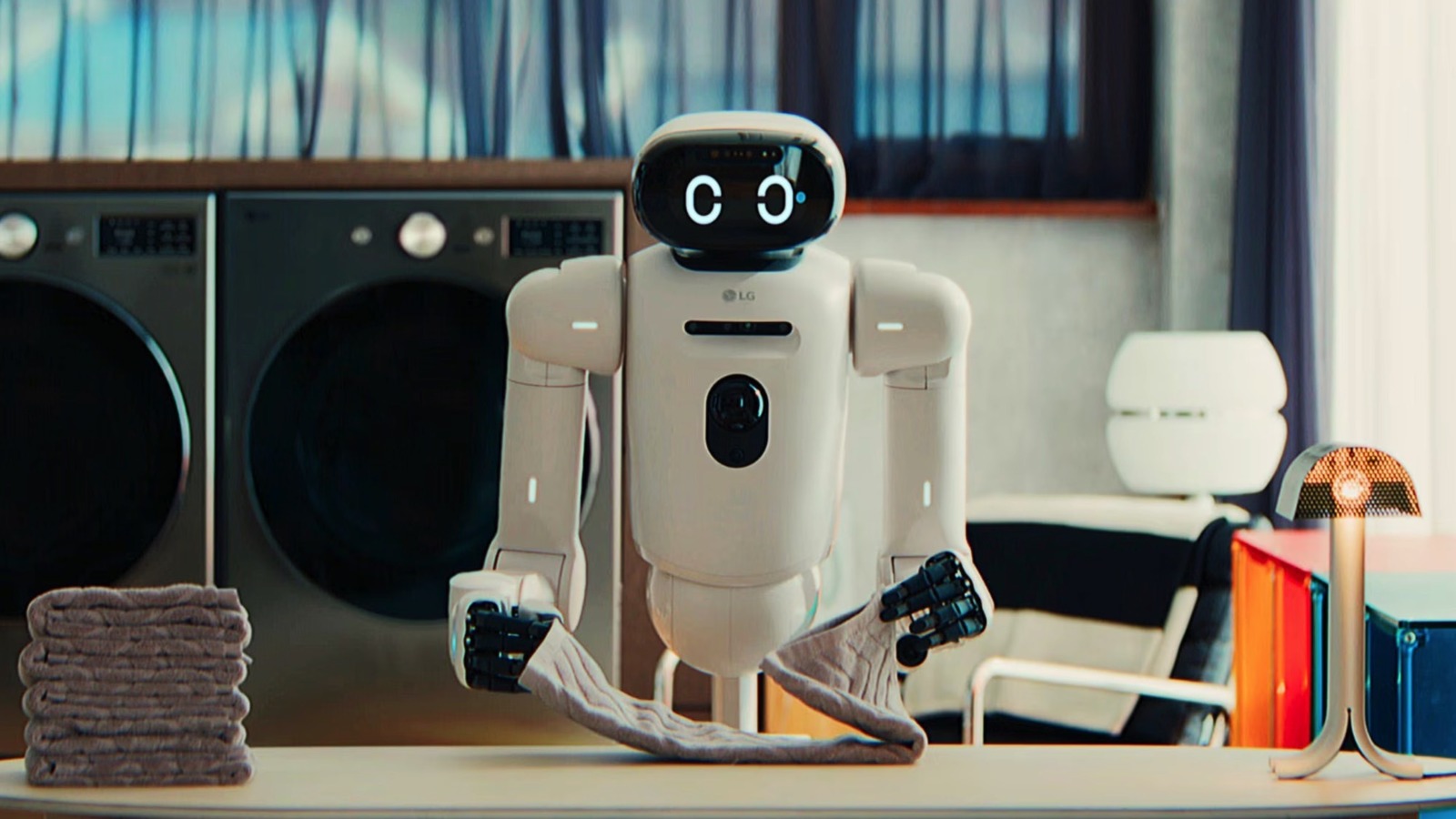

LG unveiled CLOiD at CES 2026, a wheeled domestic robot that folds laundry and coordinates smart-home devices using integrated Vision Language Model (VLM) and Vision Language Action (VLA) AI trained on tens of thousands of hours of household tasks. The unit features two seven-degree-of-freedom arms with five-fingered hands, a new Axium joint actuator with regenerative slowing, and ThinQ platform integration, but LG disclosed no pricing, availability or battery-life estimates, leaving near-term revenue and adoption implications uncertain.

Market structure: LG Electronics (066570.KS) and its ecosystem partners (actuator/motor suppliers like Nidec 6594.T, semiconductor vendors such as NVDA) are the primary beneficiaries if CLOiD converts from demo to commercial product — think potential ASPs of $3k–$8k and margin uplift from service/ThinQ subscriptions that could add 2–4% incremental EBITDA over 2–3 years. Losers include low‑end appliance makers and independent laundromats whose price-sensitive customers won’t buy premium robots, and retailers with thin service networks that can’t support installation/maintenance. The shift favors vertically integrated incumbents with platform lock‑in, raising pricing power for bundled home-automation offers. Risk assessment: Tail risks include product‑liability incidents, EU/US privacy or AI safety regulation (AI Act enforcement, consumer-robot safety rules) and battery/thermal failures that could force recalls — low-probability but >50% portfolio impact for OEMs. Time horizons split: immediate (days) = limited PR-driven moves; short (3–9 months) = supply orders for actuators/chips and partner deals; long (12–36 months) = revenue recognition and recurring service monetization. Hidden dependencies: ThinQ ecosystem adoption rate, installer/service network scale, and household layout (staircase limitation cuts addressable market by ~20–30% in multi‑story markets). Catalysts: preorder launches, LG guidance, supplier bookings, and regulatory announcements. Trade implications: Direct plays — establish a tactical 1.5–3% long in 066570.KS on a 12–18 month horizon targeting +25–35% if robots reach ~5% appliance revenue; buy NVDA (NVDA) exposure via a 9–12 month call spread to capture edge AI inference demand (see below). Buy Nidec (6594.T) or ABB (ABB) exposure (1–2% each) to play actuator content growth. Relative trade — long LG (066570.KS) / short Whirlpool (WHR) 0.5–1% pair over 12 months to express platform vs commodity appliance dispersion. Options — consider NVDA 12‑month call spread (buy 1x 12‑month ITM call, sell higher strike to finance) sized to 1–2% notional. Contrarian angles: Consensus will overestimate near-term unit volumes and underestimate service/warranty costs; assume pacing where initial unit sales are low (<=50k units first 12 months) and ASPs high (> $4k), so suppliers of actuators may see steadier near-term revenue than OEMs. The stairs limitation and slow consumer switching imply adoption curves more S‑shaped over 3–5 years, creating short windows for outsized supplier earnings upgrades. Watch for mispricings: if LG stock retraces >15% on execution skepticism, add to exposure; conversely, if preorders >50k in 3 months at < $2k ASP, reduce supplier longs and rotate into OEMs quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25