Dutch Bros (BROS) currently holds an optimistic Average Brokerage Recommendation (ABR) of 1.34, reflecting a generally positive Wall Street outlook. However, the article cautions against relying solely on ABRs due to inherent analyst bias and instead highlights the Zacks Rank, a quantitative model based on earnings estimate revisions, as a more reliable indicator. Notably, BROS's Zacks Consensus Estimate for current year EPS recently declined 2.5% to $0.59, resulting in a Zacks Rank #4 (Sell), which suggests potential near-term downside for the stock despite the favorable ABR.

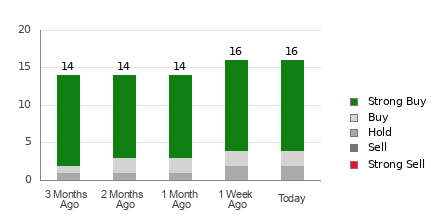

Dutch Bros (BROS) presents a conflicting profile for investors, characterized by a highly optimistic Wall Street consensus that is directly contradicted by negative underlying earnings estimate revisions. The company holds an Average Brokerage Recommendation (ABR) of 1.34, which falls between a 'Strong Buy' and 'Buy', with 14 out of 16 covering analysts rating the stock favorably. However, this bullish sentiment is challenged by the proprietary Zacks Rank system, which assigns BROS a #4 (Sell) rating. The primary driver for this bearish quantitative signal is a deterioration in the company's earnings outlook. Specifically, the Zacks Consensus Estimate for current-year earnings per share has declined 2.5% over the past month to $0.59, indicating a growing pessimism among analysts regarding near-term profitability. The article suggests this trend in earnings revisions is a more reliable predictor of near-term stock performance than the often-biased ABR, flagging it as a potential precursor to a stock price decline.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.50

Ticker Sentiment