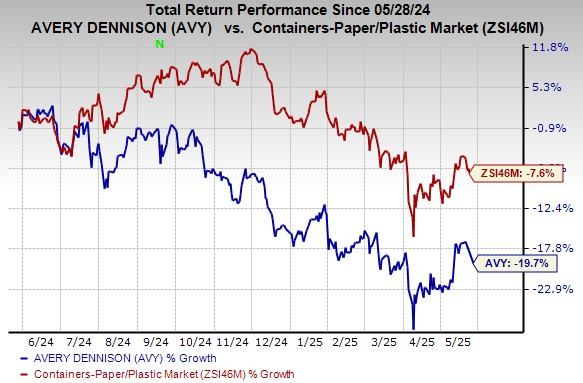

Avery Dennison (AVY) is benefiting from strong demand in consumer-packaged goods and e-commerce, driving growth in its Materials group segment, along with strategic restructuring to focus on high-value categories; however, rising raw material costs and supply chain challenges are expected to pressure margins, leading to an anticipated 1% year-over-year dip in adjusted EPS for Q2 2025, and the stock has underperformed its industry over the past year, declining 19.7%.

Avery Dennison (AVY) presents a dichotomous outlook, characterized by strong underlying demand offset by significant cost pressures. Approximately 40% of its revenue stems from labeling non-durable consumer goods and 15% from e-commerce-linked logistics, both experiencing robust demand which supported volume and productivity gains in its Materials and Solutions Groups in Q1 2025. The company's strategic focus on high-value categories, such as Intelligent Labels which are projected for over 15% growth in 2025, and a historical four-year adjusted EBITDA CAGR of 8% and sales CAGR of 7% highlight its growth initiatives. However, persistent inflation in raw materials like paper and energy, coupled with supply chain challenges and rising labor costs, are expected to compress margins, leading to a guided 1% year-over-year midpoint decline in Q2 2025 adjusted EPS, projected between $2.30 and $2.50. High debt levels and unfavorable currency translation add to these concerns. This challenging environment is reflected in AVY's stock underperformance, declining 19.7% in the past year versus the industry's 7.6% fall, and its current Zacks Rank #4 (Sell).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

-0.10

Ticker Sentiment