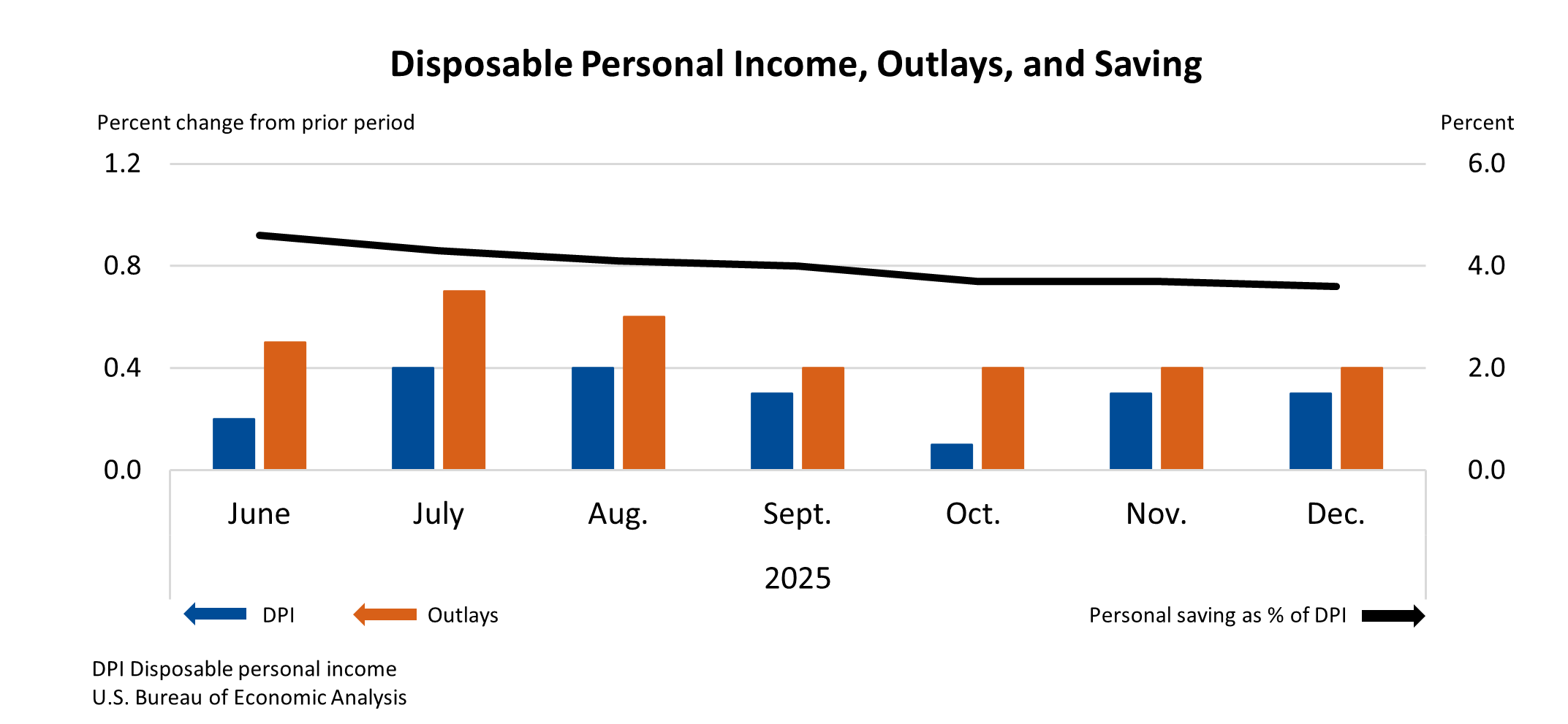

December 2025 personal income rose $86.2 billion (0.3% m/m) and disposable personal income rose $75.7 billion (0.3%), while personal consumption expenditures increased $91.0 billion (0.4%) and real PCE rose 0.1%. The PCE price index increased 0.4% month‑over‑month and 2.9% year‑over‑year (core +3.0% y/y); the personal saving rate was 3.6%. Income gains were driven by a $38.4 billion rise in transfer receipts — including a settlement related to the 2023 Maui wildfire — and a $31.0 billion increase in compensation. The combination of resilient consumption and still-elevated PCE inflation is a key datapoint for Fed policy watchers.

Market structure: December shows services-led consumption (PCE services +$98.5B vs goods -$7.5B) with headline PCE +0.4% m/m and core PCE +0.4% m/m (3.0% YoY). Winners: travel, restaurants, leisure and service-platforms that can sustain pricing power; losers: big-box/goods retailers and discretionary durables. Cross-asset: stickier services inflation supports higher nominal yields and a stronger USD; expect risk-off for long-duration growth and mixed commodity signals (industrial demand pressure vs energy resilience). Risk assessment: the headline income bump was partly one‑off (Maui utility settlement ~$23B) and government transfers (Medicare +$15.4B), while the personal saving rate is low at 3.6% — limited buffers to absorb shocks. Tail risks include a reversal in disposable income when one-offs fade, a hawkish Fed response to ~3% core PCE that forces a sharper tightening, and revisions to BLS/CES data; catalysts are next two PCE prints, Feb–Mar CPI and Fed minutes. Trade implications: tactical overweight services/cyclicals and underweight goods retailers; prefer short-duration interest-rate exposure and explicit inflation hedges. Immediate (days–weeks): implement pair trades that long consumer-services exposure and short goods retail; short-duration TIPS or TIPs to protect real returns. Medium (1–6 months): if core PCE holds ≥3.1% YoY or 10y yields rise >25bp, increase rate-short and inflation-hedge sizes. Contrarian angles: consensus may dismiss December as noise from settlements; with savings near multi-decade lows and services inflation sticky, the market likely underestimates persistent policy risk and duration repricing. Historical parallel: 2018 services-driven inflation triggered a rapid bond selloff — a muted consensus reaction today suggests mispricing in long-duration assets. Hedging cyclicals against a policy‑induced slowdown is prudent.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00