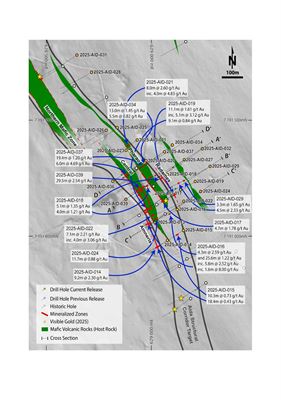

Goldsky Resources (TSX‑V: GSKR) reported final assays from its 2025 Aida diamond drill program (10,296.9 m in 39 holes), with gold mineralization in 33 of 39 holes and visible gold in seven; standout intercepts include 26.4 m @ 2.80 g/t Au (AID‑039), 21.4 m @ 1.17 g/t Au (AID‑037), and high‑grade 11.42 g/t Au over 1.45 m (AID‑027) and 8.00 g/t Au over 1.6 m (AID‑016). The program identified two new zones (Radames and Amneris), extended the Aida structural corridor testing to ~2.1 km of strike (remaining open along a >2 km trend), and the company plans modelling and follow‑up drilling in 2026 — positive exploration results that could meaningfully de‑risk and expand the target but remain at an early, resource‑definition stage.

Market structure: Goldsky (GSKR) and nearby operators (Svartliden mill participants, plus JV partner Agnico Eagle AEM) are primary beneficiaries — discovery adds optionality: >2 km untested strike, multiple broad intercepts (e.g., 26.4m @2.8 g/t, narrow 11.4 g/t highs) imply multi-heading potential rather than a single vein. Immediate effect on global gold supply/pricing is negligible, but local M&A and toll-milling dynamics can shift regional economics and acquirers’ willingness to pay a district premium (10–30% bid uplift seen historically in Sweden). Losers: generic juniors without mill access or district leverage will relatively underperform as capital chases district-scale targets. Risk assessment: Key tail risks are rapid dilution (explorers typically raise equity within 6–12 months), permitting/social license setbacks in Sweden, and metallurgical/continuity failure converting intercepts to a resource; a >10% drop in gold spot would materially re-rate juniors. Timing: days = headline-driven volatility, weeks–months = modeling/2026 drill planning and potential farm-in, years = mine development/capex. Hidden dependency: proximity to Svartliden mill materially reduces capital intensity if tolling or offtake negotiated; success depends on JV/farm-in decisions by deep-pocket partners (AEM). Trade implications: Tactical asymmetric plays — small-cap GSKR offers high beta to discovery: consider a 1–3% NAV equity allocation with strict risk control (30% stop). For lower volatility, use AEM (Agnico) as takeover/optionalty exposure via 6–12 month call spreads (target 15–30% return if consolidation). Relative-value: long GSKR / short GDXJ equal notional to capture idiosyncratic discovery upside while hedging gold beta; re-evaluate on 2026 resource model release. Contrarian angles: Consensus likely overestimates speed-to-mine and underestimates dilution — value crystallization will be via M&A or a maiden resource, not rapid production. Headline-driven pops in GSKR may be overdone while AEM call spreads are underpriced for 12–24 month consolidation risk. Historical analogs in Sweden show majors acquire district players within 12–24 months; prepare for both bidding wars (positive) and high dilution financing (negative).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment