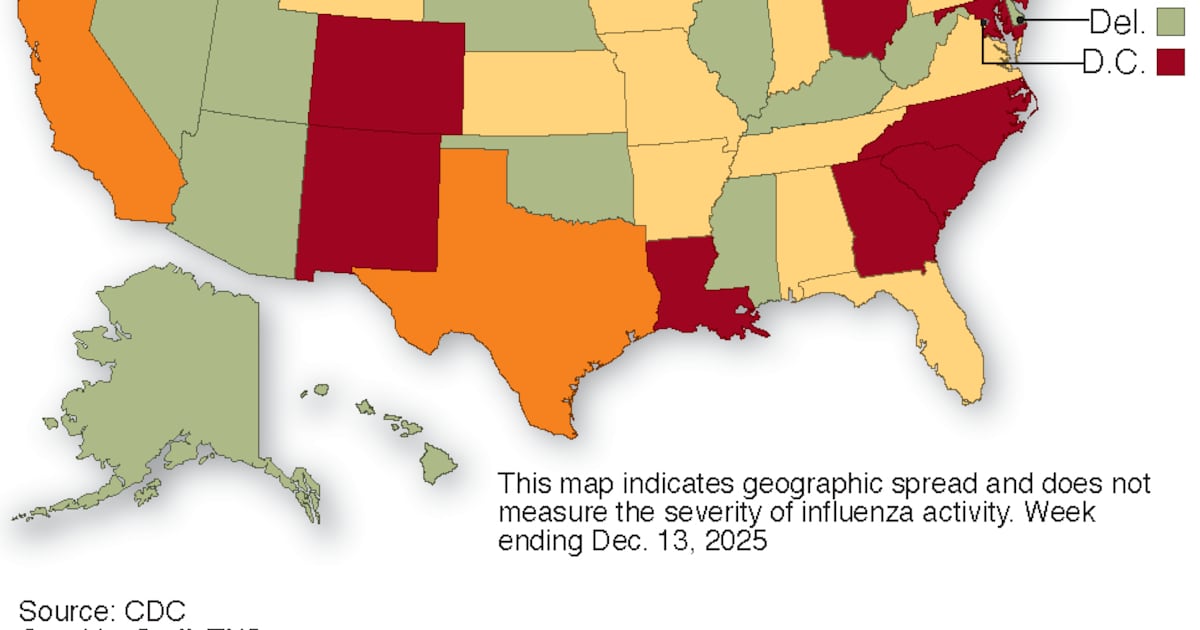

Ohio reported its first pediatric flu-related death of the season (a 16-year-old) and sharp county-level increases in hospitalizations for the week ending Dec. 27—Montgomery County rose to 194 from 86 (historical avg. 35), Greene to 30 from 9 (historical 9), with several other counties also up. The CDC says U.S. flu hospitalizations nearly doubled to 19,000 over two weeks, estimates ~7.5 million illnesses and 3,100 deaths, and attributes the surge to an influenza A strain from Australia that partly evades this season’s vaccine; regional hospitals have imposed visitor restrictions as capacity concerns mount.

Market structure: Short-term winners are retail pharmacies (CVS, WBA) and outpatient diagnostics/telehealth (QDEL, TDOC) from higher vaccine, antiviral and test volumes; vaccine manufacturers (SNY, GSK, MRNA) gain optionality for updated formulations longer-term. Losers are regional hospital operators (HCA, UHS) facing margin compression from staffing costs and potential elective-surgery deferrals, and health insurers (UNH, ANTM) who may see a quarterly spike in claims. Cross-asset: expect a mild risk‑off bid into Treasuries if hospitalizations accelerate (yields down ~5–15bps intraday) and elevated equity implied vol in affected healthcare names. Risk assessment: Tail risk is a vaccine-evading strain forcing prolonged season and federal emergency measures that shift reimbursement rules or cap prices—this would materially hit hospital/insurer margins (Q1–Q2 results). Timeframes: immediate (days) — hospitalization data and visitor restrictions; short (4–12 weeks) — realized claims and Q1 earnings; long (6–18 months) — vaccine reformulation benefits mRNA/platform names. Hidden dependencies include local labor markets for nurses and supply-chain limits for antivirals; catalysts are CDC/FDA updates and wholesale vaccine supply announcements. Trade implications: Construct short‑duration trades (30–90 days): long CVS (CVS) and QDEL (QDEL) for transactional flow; hedge hospitals via HCA put spreads. Use options to buy downside protection on insurers if weekly national hospitalizations exceed +30% week‑over‑week. Rotate portfolio overweight to pharmacies/diagnostics and underweight regional hospitals for the next 1–3 quarters. Contrarian angle: Market may overprice permanent damage — historical severe-flu seasons (e.g., 2017–18) caused 1–2 quarter hits then normalization. If CDC signals peak by February, hospital stocks can mean‑revert 15–30% from oversold levels; conversely underinvestment in updated vaccines is a multi‑quarter mispricing opportunity for MRNA and SNY if regulatory authorization timelines accelerate.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35