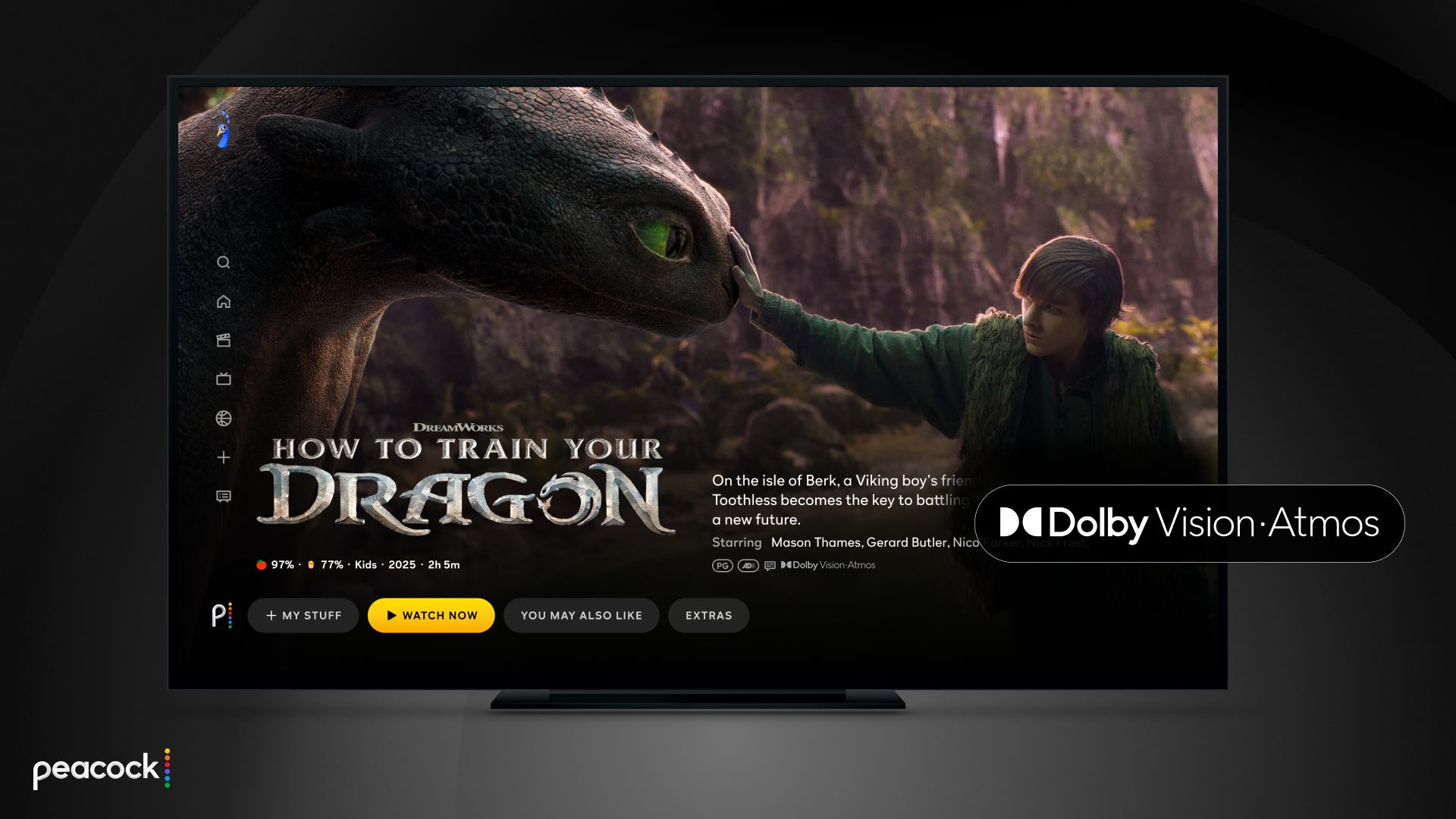

Peacock announced at CES 2026 it will be the first streaming platform to support Dolby Vision 2 HDR and Dolby AC-4, planning a rollout later this year that will include live sports and Peacock Originals with Dolby Atmos and Vision 2. Hardware limitations may constrain near-term adoption: LG confirmed none of its 2026 TVs will support Vision 2 and Samsung is promoting a rival HDR10+ Advanced standard, leaving uncertainty over the addressable audience and timing for broader uptake. The integration offers Peacock a content-differentiation advantage and potential upside for Dolby licensing, but meaningful commercial or market-moving impact depends on TV vendor support and consumer hardware upgrade cycles.

Market Structure: Dolby Vision 2 adoption by Peacock (Comcast/CMCSA) creates a narrow, near-term winner set: Dolby Labs (DLB) via licensing, Peacock via product differentiation, and downstream suppliers (SoC vendors like QCOM) if hardware updates are required. TV OEM fragmentation (LG declining 2026 support; Samsung pushing HDR10+ Advanced) creates a two-horse meta-standard battle that will compress pricing power for HDR premium TVs and slow a broad upgrade cycle in 2026–2027 if interoperability is unclear. Risk Assessment: Tail risks include an industry-standard war (HDR10+ Advanced vs Dolby Vision 2) leading to slower consumer adoption or antitrust/licensing disputes that could delay rollouts by 6–18 months. Near-term (days–weeks) impact is limited; expect material effects in quarters (Q3–Q4 2026) as content, chipset, and TV support converge or diverge. Hidden dependencies: OEM firmware/SoC upgrades, HDMI/DRM chip compatibility, and agreements between content owners and Dolby. Trade Implications: Favor plays that profit from codec licensing and selective content differentiation: long DLB and small overweight to CMCSA (Peacock), while avoiding outright long positions in premium-TV OEMs that do not commit to a standard (LG/LPL risk). Use options to express asymmetric upside (DLB LEAP call spreads) and hedge through shorts or put spreads on incumbents slow to adopt (select TV supply names). Contrarian Angles: Consensus may underweight the risk that hardware fragmentation stalls demand — not all consumers will upgrade in 2026, making panel suppliers vulnerable to a 5–15% revenue reset versus base case. Conversely, if Dolby secures 2–3 additional major platform deals inside 6 months, DLB upside could be front-loaded; fast-flow catalysts (CES follow-ups, licensing announcements) will be binary drivers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.15

Ticker Sentiment