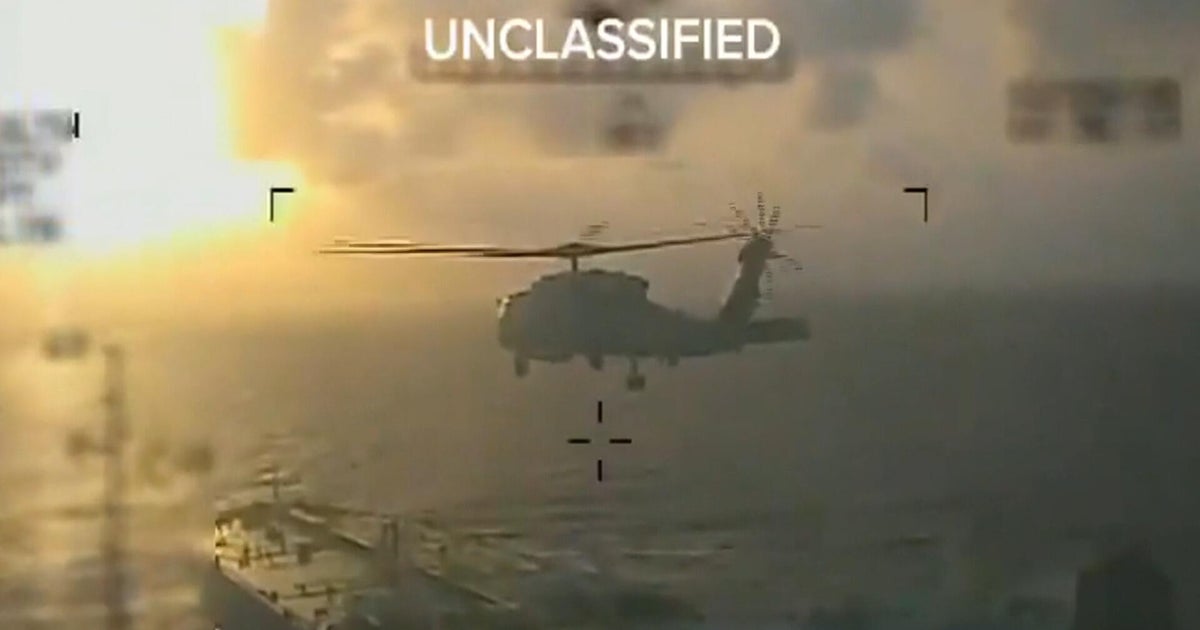

U.S. Coast Guard forces pursued a sanctioned 'dark fleet' oil tanker off Venezuela — the second such operation over the weekend and third in under a week — and on Saturday seized the Panama‑flagged tanker Centuries, which U.S. officials say was falsely flagged and used to evade sanctions to traffic oil for the Maduro regime. The operations follow President Trump's call for a blockade of sanctioned tankers and coincide with Defense Department orders to attack vessels allegedly smuggling fentanyl, a campaign that U.S. officials argue is limited in scale but which Caracas condemned as 'piracy' and threatens diplomatic escalation. While U.S. officials contend the seizures should not materially raise U.S. fuel prices, the actions raise regional geopolitical risk and uncertainty around Venezuelan oil flows and emerging‑market exposure.

Market structure: U.S. interdictions of Venezuelan tankers tighten an already constrained marginal supply band (dark fleet crude flows ≈100–300 kb/d). Near-term winners are defense/maritime security contractors and P&I/war-risk insurers (upward pressure on premiums +10–25% possible); losers are owners/operators of older tankers (EURN, FRO, NAT) who face arrest/seizure and reflagging costs. Cross-asset: expect idiosyncratic widening in tanker equity CDS and higher oil freight (TC) rates, modest bullish tilt to Brent/WTI (+$1–$3/bbl near term) and temporary USD safe-haven strength versus EM FX. Risk assessment: tail risks include retaliatory seizures or escalation leading to a >1% hit to global seaborne crude causing Brent spikes of +10–20% (months). Immediate (0–7 days): volatility in tanker names and insurer spreads; short-term (1–3 months): freight rate and insurance-cost repricing; long-term (3–18 months): structural shift toward higher compliance costs and reflagging increasing OPEX by 5–15%. Hidden dependencies: China/India buying patterns of Venezuelan oil can neutralize U.S. pressure; judicial seizure precedent increases legal/regulatory uncertainty for all shipowners. Trade implications: favors long defense (LMT, RTX, LHX) and long energy infrastructure insurers/reinsurers while short select tanker equities (EURN, FRO, NAT) and freight ETFs. Use options to express asymmetric views: buy 3-month call spreads on XLE or WTI futures if Brent >$85, and buy puts on concentrated tanker names to limit idiosyncratic risk. Sector rotation: reduce pure-play tanker exposure and increase allocations to defense and energy midstream (XLE, ENB) by 1–3% each over 4–12 weeks. Contrarian angles: consensus believes seizures won’t move oil prices — that underestimates concentrated vulnerability of ‘shadow fleet’ routes; if further seizures remove 200–400 kb/d of seaborne capacity for 60+ days, tanker rates and crude differentials will reprice sharply. The market may be over-discounting permanent supply loss; cheapest mispricing is longer-dated protection (6–12 month) on tanker equity downside and long volatility in maritime insurance names rather than spot oil long exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35