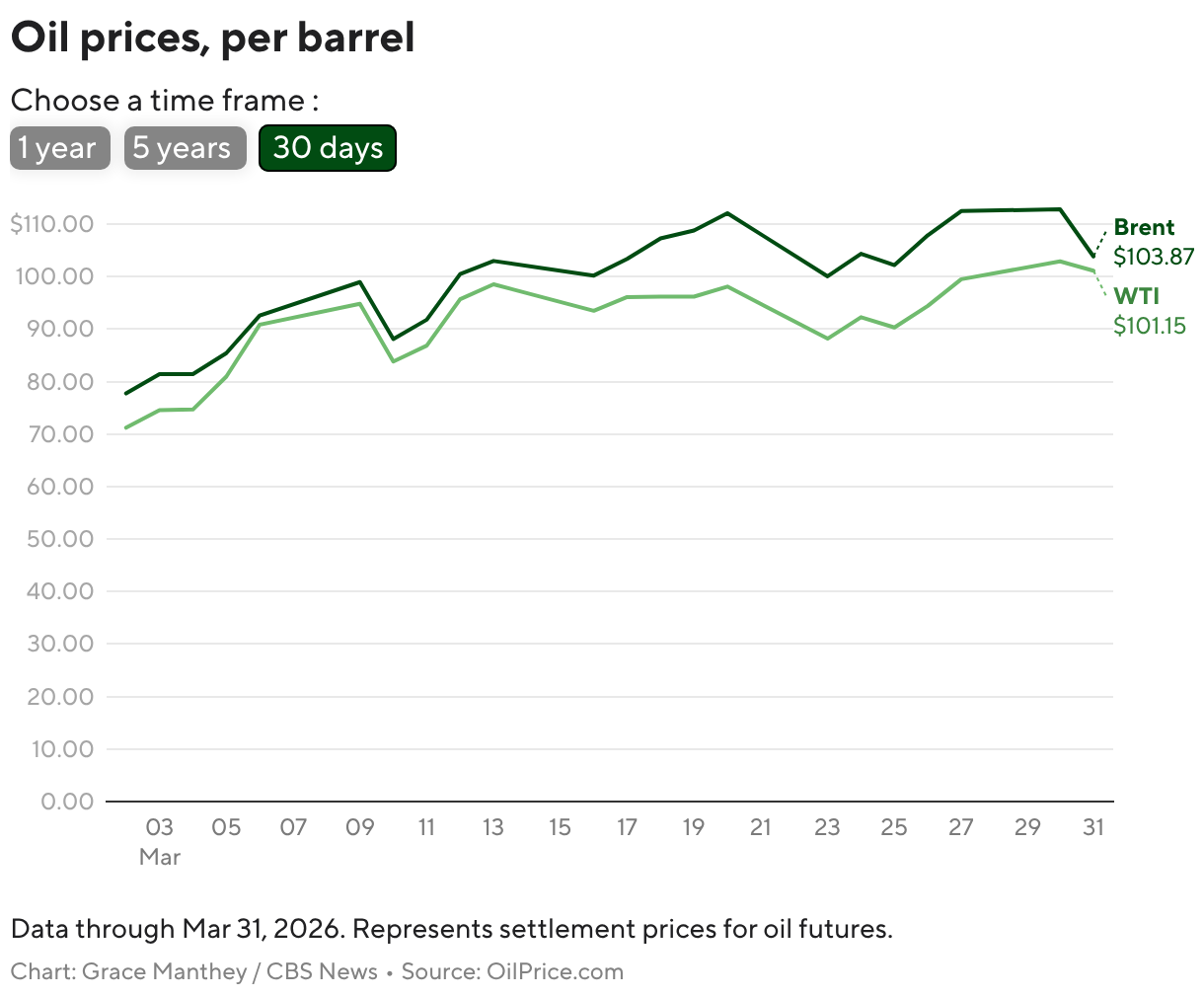

Oil surged—Brent +7.7% to $109/bbl and U.S. crude +11.9% to $111.81—while the S&P 500 closed up 0.1% at 6,583, Nasdaq +0.2% and the Dow fell 61 pts (-0.1%). Markets reacted to President Trump's Middle East update and reports Iran and Oman are coordinating oversight of the Strait of Hormuz, which Oxford Economics says remains effectively closed and could keep global supplies disrupted through April. Analysts warn of much higher oil scenarios ($150–$200/bbl) and rising U.S. gasoline (average $4.08/gal), leaving equities volatile but supported by resilient corporate earnings and investor FOMO.

A sustained energy-supply shock manifests less as a single-day move and more as a multi-month tax on logistics and working capital: higher freight lanes, elevated marine insurance, and lengthened transit times force firms to hold more inventory and reduce inventory turns. That combination creates a concentrated margin hit for midcap consumer and industrial companies with just-in-time supply chains — expect 2–4 quarters of revenue timing noise and 200–400bp gross margin pressure for the most exposed cohorts before procurement cycles normalize. Market microstructure amplifies episode volatility. Dealers’ short-gamma + retail “fear-of-missing-out” creates intraday reflex rallies that can look like durable bottoms, drawing capital flows into fee-for-flow franchises (exchanges, retail brokers) while simultaneously stretching valuations on cyclical, low-quality shorts. Exchange operators capture a disproportionate share of episodic trading revenue — a transient 10%+ rise in ADV converts to a persistent revenue catch-up over the subsequent quarter as derivatives clearing and listed options volumes reprice. Key catalysts that would reverse the current premium are diplomatic corridor formation, material SPR or strategic sales beyond comms, or a visible improvement in shipping throughput; each operates on a different clock (days for a diplomatic headline, weeks for SPR actions to mechanically ease spreads, months for inventory rebalancing). The bigger tail is a protracted commodity shock that forces demand destruction and multiple compression across cyclicals — that’s a months-to-year outcome, not an intraday shock. The consensus underestimates the persistence of higher logistics costs and overestimates the speed with which consumers absorb price shocks without behavior change. That makes “durable revenue-capture” businesses (exchanges, retail platforms with high take-rates) asymmetric beneficiaries versus cyclicals that look cheap but can see margin erosion and permanent market-share shifts if customers accelerate substitution.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment