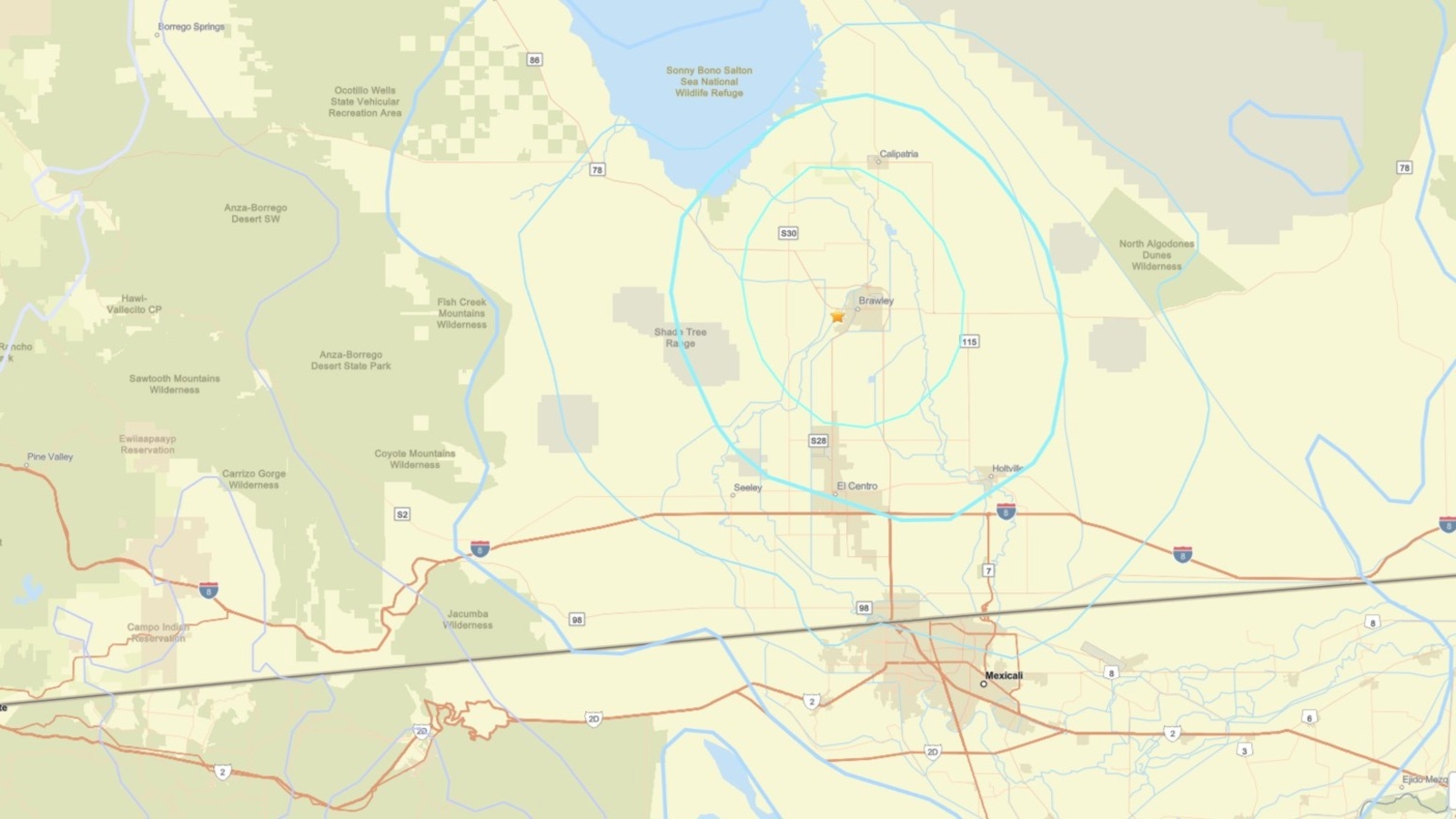

A swarm of more than 150 earthquakes rattled Imperial County near Brawley, California, including a 4.5 magnitude quake at 8:39 p.m. and other sizable tremors of 4.4 and 4.0. No injuries or significant damage were immediately reported, but authorities warned residents to stay alert for aftershocks as activity continued late into the night. The event is consistent with the area's typical seismic behavior, though it raises localized safety and preparedness concerns.

This is a local geophysical event, but the investable angle is less about immediate physical damage and more about the repeated reminder that Southern California’s industrial and utility infrastructure sits on an always-on tail risk premium. In the near term, the market impact is likely confined to sentiment in regional insurers, utilities, and contractors rather than a broad macro read-through, because the current evidence points to low acute loss severity. The second-order issue is that even “no damage” swarms tend to reprice preparedness spending, resilience capex, and insurance renewal assumptions over the next 1-4 quarters.

The most interesting asymmetry is in companies with concentrated exposure to California property books or critical infrastructure exposure. For insurers and reinsurers, the event itself is not the problem; the problem is what it does to underwriting discipline if swarm activity becomes persistent and drives more frequent near-miss claims, policy non-renewals, and reinsurance cost inflation into 2025 renewal cycles. For utilities, telecom, and water infrastructure names, the market often underestimates the optionality of grid hardening, backup power, and asset inspections, which can support incremental capex but also compress near-term margins.

The contrarian read is that this is more likely to be a procurement and resilience revenue catalyst than a destruction event. If aftershocks stay modest, contractors, sensor/monitoring vendors, emergency communications providers, and retrofit-focused engineering firms can benefit without a broad disaster headline. The risk case is a higher-magnitude follow-on quake over the next days to weeks; that would flip the trade from capex upside to loss-driven downside for California-exposed financials and infrastructure operators.

From a portfolio perspective, the edge is to fade complacency in property-exposed balance sheets while expressing a small long in resilience beneficiaries. The setup is not about chasing an immediate “disaster trade,” but about positioning for slower-moving premium, inspection, and retrofit budgets that can flow for months after the event if the swarm persists.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15