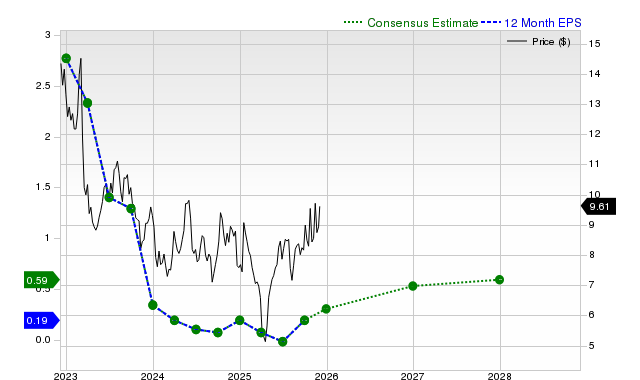

Zacks highlights chemical maker LSB (ticker LXU) after analysts raised estimates, awarding the stock a Zacks Rank #2 (Buy). The Zacks Consensus expects $0.18 EPS for the current quarter (up 157.1% y/y) with the 30-day consensus rising 102.33% after one upward revision, and $0.36 EPS for the full year (up 56.5% y/y) with the consensus up 62.15%. The stock has gained roughly 14.5% over the past four weeks as estimate revisions have driven investor optimism and could support further near-term upside.

Market structure: LXU (LSB/LXU) looks to be the short-cycle chemical/nitrogen beneficiary of positive analyst revisions; direct winners are mid-cap nitrogen/industrial chemical producers with flexible feedstock costs, while large-cap commoditized peers and downstream commodity buyers face margin pressure if input-driven pricing resets. Rising consensus EPS (+60–100% revisions cited) typically compresses implied yields and draws momentum flows; expect near-term rotational inflows into LXU and related small-cap chemicals at the expense of broad materials ETFs (XLB). Cross-asset: natural gas and ammonia prices are the key drivers — a sustained Henry Hub < $3.50/MMBtu over 60 days would likely add +10–20% to LXU operating margins; higher rates would cap cyclicals and increase discount rates on forward EPS upgrades. Risk assessment: Tail risks include a plant outage or environmental/regulatory restriction that can erase revised earnings (historical outages create >30% quarterly EPS hits), and a sudden rebound in natural gas > $4.50/MMBtu that narrows nitrogen spreads. Time horizons split: immediate (days) dominated by momentum and options flows around any earnings print; 1–3 months driven by seasonal agricultural demand and gas trends; 3–12+ months by capital spending, new capacity, or structural fertilizer demand. Hidden dependencies: analyst upgrades may be herd-driven and concentrated (one or two shops), so revisions can reverse quickly if guidance misses; second-order effect is short-covering that exaggerates moves. Trade implications: Favor a staged, asymmetric long in LXU: initial 1–2% position, add to 3–4% on pullback to -10% from current price or on another +20% consensus EPS upgrade in 30 days. Use options to control risk: buy 3–6 month bull-call spreads (buy ATM, sell +25% OTM) to cap cost if implied vol rises pre-earnings; alternatively sell covered calls against core stake to monetize immediate momentum. Relative trades: pair long LXU vs short CF (CF) or XLB when natural gas > $4.00, because LXU's small-cap optionality outperforms when inputs fall but underperforms when inputs spike. Contrarian angles: The market is likely underpricing input-sensitivity and concentration of analyst optimism — the 14.5% four-week gain may be overdone if revisions come from a single shop or if guidance is cautious. Historical parallels: fertilizer/chemical rallies (2021–22) reversed sharply when gas spiked or outages occurred; expect >25% intrayear volatility. Unintended consequence: bullish flows can attract opportunistic short sellers and create squeeze dynamics; require stop-loss discipline (set at -12% from entry) and re-evaluate after next quarterly report or if Henry Hub moves +/-25% from current baseline.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment