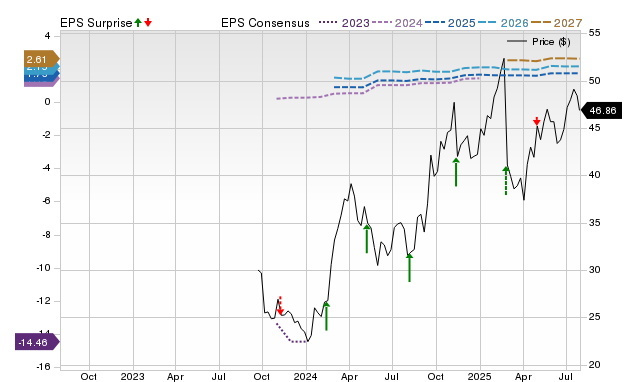

Maplebear (CART), the Instacart operator, is projected to report Q3 2025 earnings of $0.50 per share, a 19.1% year-over-year increase, on revenues of $934.4 million, up 9.7%. Despite a recent 1.01% upward revision in consensus EPS estimates, the company's Zacks Earnings ESP of -0.16% combined with a Zacks Rank #3 suggests a low probability of an earnings beat, making it an uncompelling candidate for a positive surprise ahead of its November 10 release, despite having surpassed estimates in three of the last four quarters.

Maplebear (CART), the Instacart operator, is projected to report Q3 2025 earnings of $0.50 per share, representing a 19.1% year-over-year increase, alongside revenues of $934.4 million, up 9.7%. The consensus EPS estimate has seen a modest 1.01% upward revision over the past 30 days, indicating some positive analyst sentiment leading into the November 10 release. Despite the positive revision, Maplebear's Zacks Earnings ESP stands at -0.16%, with the Most Accurate Estimate being lower than the consensus, suggesting recent bearishness among analysts regarding earnings prospects. Combined with a Zacks Rank #3 (Hold), this configuration makes a conclusive prediction of an earnings beat difficult, as highlighted by the model's predictive limitations for negative ESP readings. Historically, CART has demonstrated a strong track record, surpassing consensus EPS estimates in three of the last four quarters, including a 5.13% surprise in the previous quarter. However, the current negative Earnings ESP indicates that, based on this proprietary model, Maplebear is not considered a compelling candidate for an earnings beat in the upcoming report, despite its growth projections.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

-0.10

Ticker Sentiment