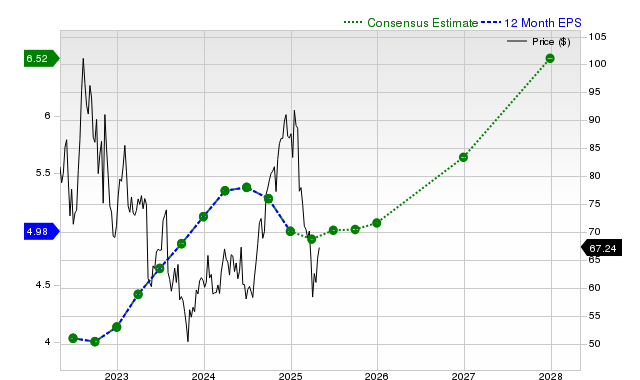

PayPal (PYPL) shares have outperformed the S&P 500 and its industry over the past month, driven by positive earnings estimate revisions; the current quarter EPS is projected to increase 7.6% year-over-year, with the Zacks Consensus Estimate rising 8.3% over the last 30 days. Revenue growth is expected to be more modest, with a 2.9% increase for the current quarter and 3.2% for the current fiscal year. Despite positive earnings revisions and a Value Style Score of B indicating undervaluation relative to peers, PayPal holds a Zacks Rank #3, suggesting near-term performance in line with the broader market.

PayPal Holdings, Inc. (PYPL) has recently demonstrated notable stock performance, with shares returning +7.6% over the past month, thereby outperforming the Zacks S&P 500 composite's +5.2% change and the Zacks Financial Transaction Services industry's +4.2% gain. This upward movement appears significantly influenced by positive revisions in earnings estimates. For the current quarter, PayPal is projected to achieve earnings of $1.28 per share, marking a +7.6% year-over-year increase, and the Zacks Consensus Estimate for this period has risen by +8.3% over the last 30 days. Looking at the broader fiscal year, the consensus earnings estimate of $5.08 for the current year indicates a +9.3% change from the prior year, with this estimate having increased by +2% in the last month. For the next fiscal year, an EPS of $5.66 is anticipated, representing an +11.3% increase, with a +1.2% upward revision in the past month. In contrast, PayPal's projected revenue growth is more modest; the consensus sales estimate for the current quarter is $8.12 billion, a +2.9% year-over-year increase, while current and next fiscal year revenue estimates indicate changes of +3.2% and +6.5%, respectively. Reviewing its last reported results, PayPal posted revenues of $7.79 billion, a +1.2% year-over-year change, which was a slight miss of -0.22% against the Zacks Consensus Estimate. However, its EPS of $1.33 for the same period represented a significant +15.65% beat, and the company has surpassed consensus EPS estimates in each of the trailing four quarters. Despite these strong earnings beats and a Zacks Value Style Score of B, indicating it trades at a discount to its peers, PayPal carries a Zacks Rank #3 (Hold), suggesting its near-term performance may align with the broader market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment