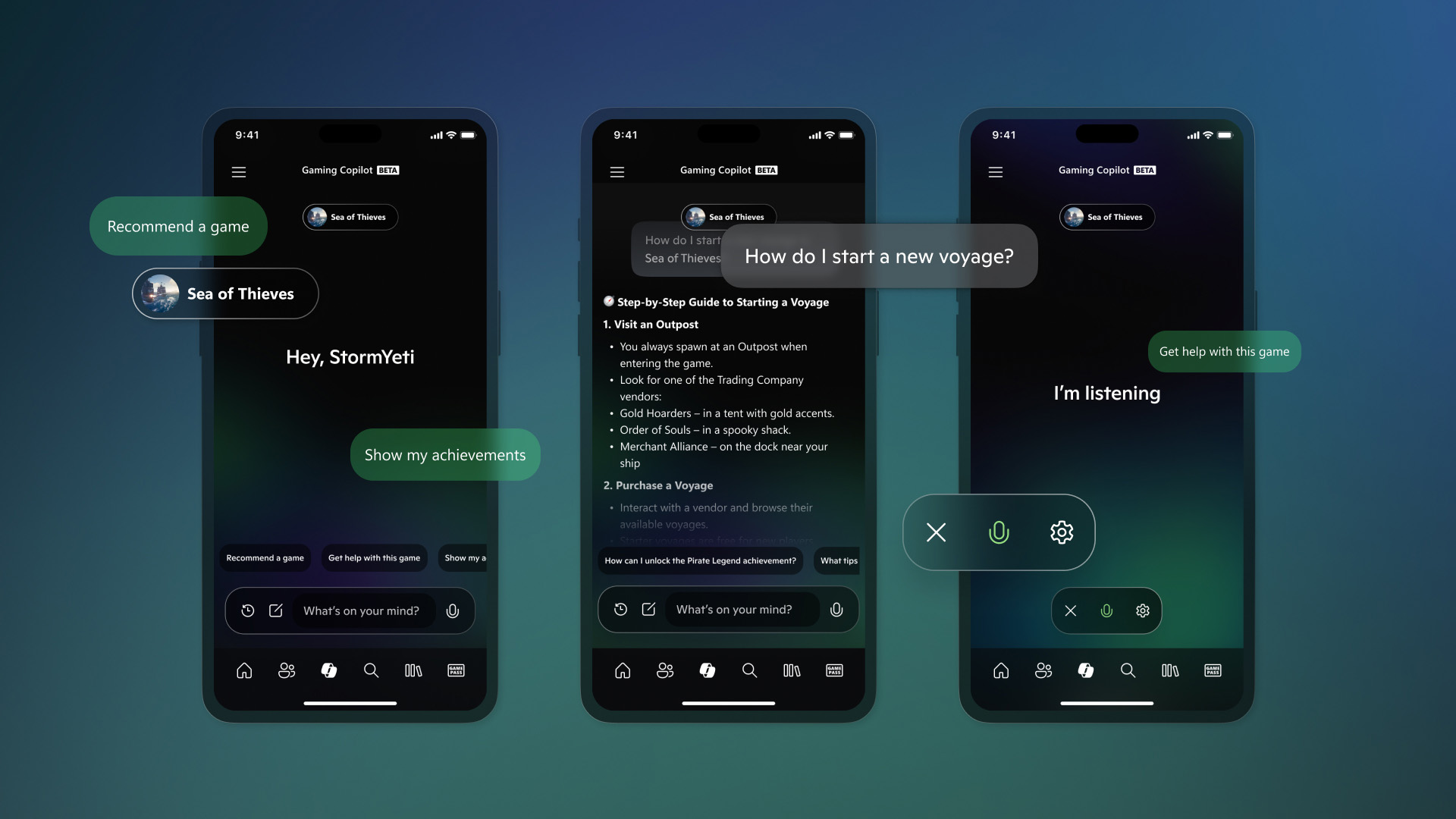

Xbox announced a slate of product and regional expansions aimed at driving engagement across devices: Gaming Copilot (Beta) is now in the Xbox mobile app, Full Screen Experience is rolling out to more Windows 11 handhelds and PCs, and cloud gaming now offers user-selected streaming resolution up to 1440p for select titles. The company expanded Xbox Cloud Gaming to India (its 29th cloud market), extended device support in Brazil and Argentina (including LG TVs and Fire TV devices) and plans broader Xbox app support on Fire TV models, while promoting ecosystem plays—Design Lab engraving promo, new accessories, 1,000+ Xbox Play Anywhere titles and a 1,000+ 'stream your own game' library—which collectively aim to increase user retention and addressable platform reach.

Market structure: Microsoft (Xbox) and platform partners (Amazon Fire TV, LG, device OEMs) are direct beneficiaries as cloud expansion and FSE lower friction to play and raise Game Pass TAM — estimate incremental addressable users +5–10% in India/Latin America over 12–24 months. Hardware console incumbents (Sony) face marginal share pressure as subscription/cloud reduces lock‑in; publishers may negotiate higher licensing revenue or push for exclusives, altering content economics. Nvidia and Azure-capacity suppliers see demand tailwinds from increased cloud encoding/rendering needs, tightening GPU supply for data centers in next 6–18 months. Risk assessment: Tail risks include regulatory/antitrust scrutiny of bundling across Azure/Game Pass, or telecom constraints in emerging markets (latency caps) that could blunt adoption — >25% lower streaming quality could reduce conversion by half in those markets. Short-term (days–weeks) impact is minimal; medium-term (3–12 months) depends on subs growth and Amazon device rollout timing (Fire TV app in 2025); long-term (1–3 years) hinges on ARPU improvement vs. incremental capex for servers. Hidden dependencies: local telco partnerships, content licensing costs, and energy/GPU supply — failures here are nonlinear to margin. Trade implications: Favor long MSFT exposure to capture recurring revenue expansion: consider 2–3% portfolio long or 12–18 month call spread (strike ~10–15% OTM) sizing for defined risk; long NVDA (1–2%) for continued data‑center GPU demand, using 6–12 month calls. Modest long AMZN (1%) to play device distribution and Fire TV monetization via a January–Dec 2025 call spread; pair trade: long MSFT vs short SONY (0.5–1%) to express cloud win/loss. Use stop at 12–15% loss and add-on triggers when Game Pass net additions >5% q/q or Azure gaming revenue growth >20% y/y. Contrarian angles: Market underprices execution and cost risks — cloud gaming can be Netflix‑like cash negative for years; investors who buy MSFT at >20x forward P/E assume ARPU uplift materializes. The AMZN Fire TV pickup is likely priced in for Amazon’s broader thesis, so allocation to AMZN should be smaller and event‑driven (device sales or revenue-share disclosures). Historical parallel: media platform expansions often need 2–4 years to monetize; if Game Pass ARPU stagnates for two consecutive quarters, re-evaluate longs and rotate to pure SaaS/AI beneficiaries.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.36

Ticker Sentiment