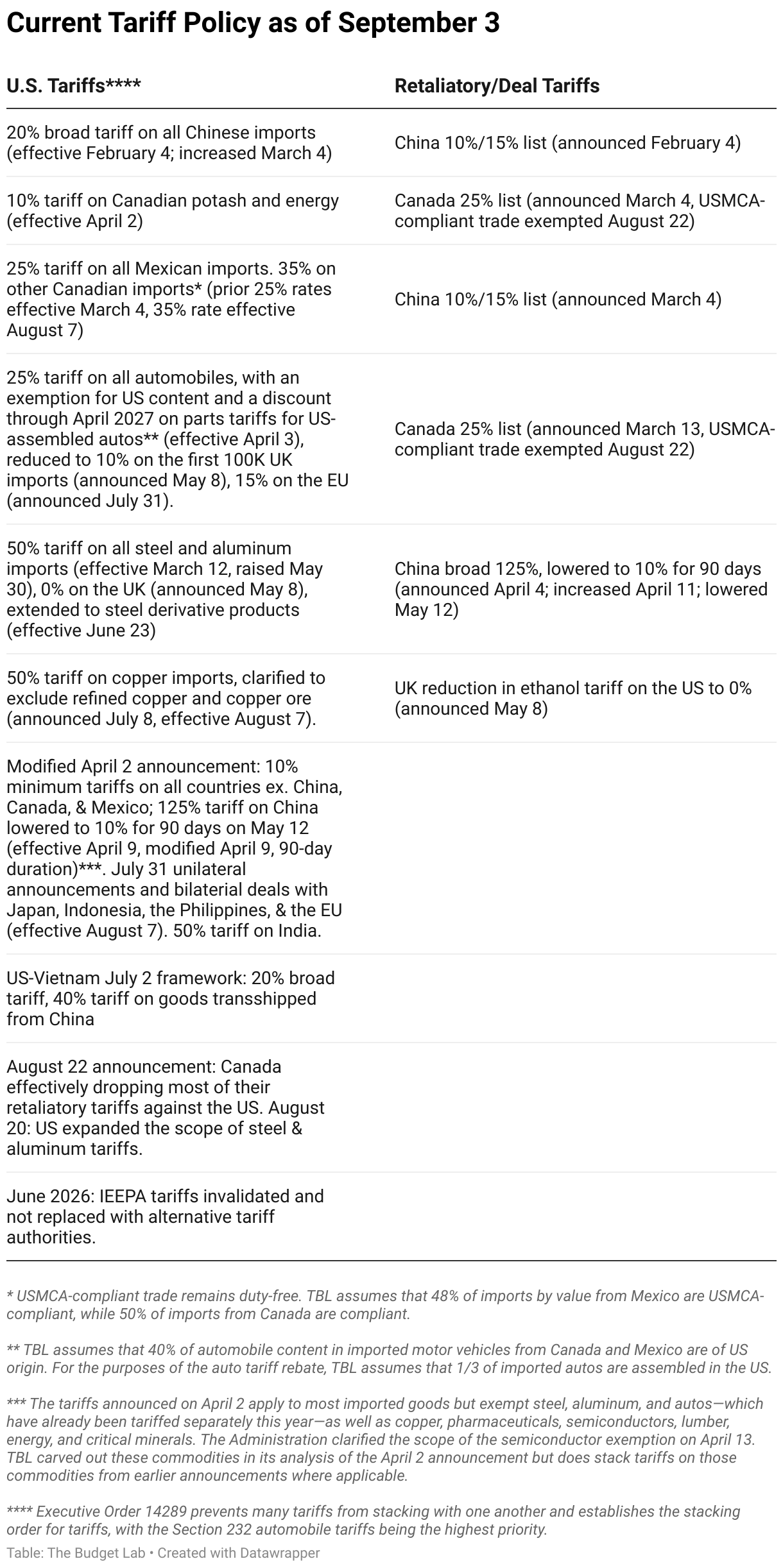

A recent analysis projects that current U.S. tariffs implemented in 2025, if maintained, would result in an average effective tariff rate of 17.4%—the highest since 1935—leading to a 1.7% price level increase, an average $2,300 household income loss, and a persistently 0.4% smaller U.S. economy long-term. However, if International Emergency Economic Powers Act (IEEPA) tariffs are invalidated, the report estimates these impacts would be substantially mitigated, with price levels rising only 0.5% ($663 household loss) and the long-run economy being 0.1% smaller. This analysis underscores the significant economic and fiscal implications of ongoing trade policy and the potential mitigating effect of judicial challenges.

The current U.S. tariff policy, if maintained, presents a significant stagflationary risk to the economy, according to a September 2025 analysis. The baseline scenario projects an average effective tariff rate of 17.4%, the highest since 1935, which is expected to increase the consumer price level by 1.7% and reduce average household income by $2,300 in 2025. This policy is forecasted to be a drag on real GDP growth by -0.5 percentage points in both 2025 and 2026, leading to a persistently 0.4% smaller economy in the long run and an increase in unemployment of 0.65 percentage points by the end of 2026. Sectoral impacts are mixed, with a 2.7% expansion in manufacturing output more than offset by a 3.8% contraction in construction. However, a key variable is the potential judicial invalidation of tariffs authorized under the International Emergency Economic Powers Act (IEEPA), which constitute 71% of the tariffs imposed. In this alternative scenario, the negative impacts are substantially mitigated: the price level increase would be only 0.5%, the long-term GDP reduction shrinks to 0.1%, and the average effective tariff rate falls to 6.8%. Notably, the commodity impacts shift dramatically between scenarios; the baseline disproportionately hits consumer goods like apparel (+36%) and leather (+37%), whereas the 'No IEEPA' scenario concentrates remaining tariffs on industrial inputs, causing sharp price increases for metals (+52%) and motor vehicles (+21%).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.75