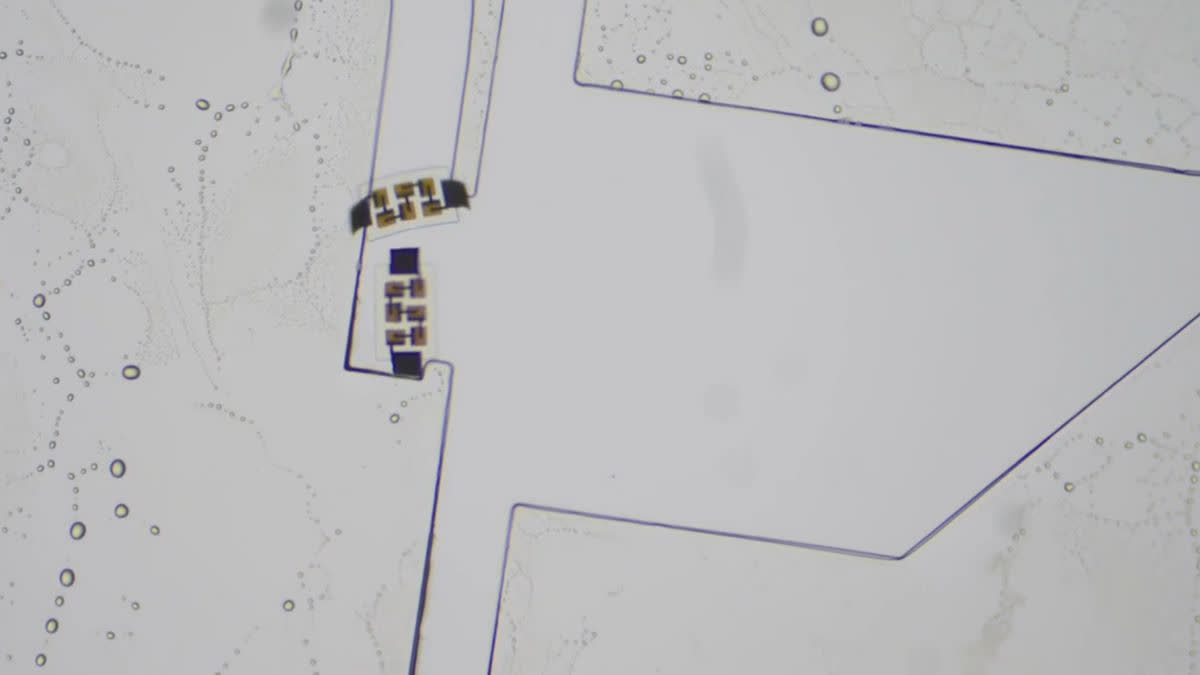

Researchers at the University of Pennsylvania and the University of Michigan have created the world's smallest fully programmable autonomous swimming robots (200 x 300 x 50 µm) that are light-powered, can sense temperature to within ~0.33°C, and travel up to ~300 µm/s. The devices integrate ultra-low‑power electronics (processors reduced >1000x power), tiny solar panels, and electrokinetic propulsion, enabling months-long operation and individual addressing; the technology could enable microscale cell monitoring and bespoke microsystems, with future versions potentially adding sensors, speed and programmability for commercial biotech and device applications.

Market structure: this breakthrough shifts demand toward precision microfabrication, low‑power analog ASICs and micro‑PV/packaging suppliers rather than large surgical‑robot incumbents. Winners in the near term are semiconductor equipment (photolithography, thin‑film deposition), MEMS fabs and low‑power analog chipmakers; losers are marginal — legacy macro‑robotics and general clinical service providers that rely on current, bulkier tooling. Expect pricing power for specialized tools to rise 10–30% over 12–24 months if commercialisation proceeds, tightening supply for sub‑100µm assembly capacity. Risk assessment: tail risks include rapid regulatory clampdowns (biosecurity/FDA) or an IP/legal blockage from university spinouts; assign a 5–15% probability within 24 months. Short term (days–months): negligible market reaction; medium (6–18 months): R&D partnerships, grant awards and pilot deals will matter; long term (2–5 years): clinical/industrial adoption if yield, biocompatibility and packaging scale. Hidden dependencies: access to specialty fabs, yield improvements and biocompatible materials — each can add 2–4 years to commercial timelines. Trade implications: direct plays are suppliers to advanced fabs and low‑power analog designers. Prefer capital‑equipment exposure (AMAT/LRCX/ASML/TSM) and Analog Devices/Texas Instruments for chip content; use ETFs (SOXX) for diversified exposure. Use defined‑risk option spreads to express convexity around 6–18 month technical milestones (papers, DARPA/NIH grants, first commercial pilot). Contrarian angles: consensus will overhype immediate medical disruption; commercialization is likely 2–5 years, not weeks. Historically (MEMS, microfluidics) lab breakthroughs produced long‑tail wins for niche suppliers rather than big incumbents — expect selective winners, not broad sector rallies. Unintended consequences: increased regulation, export controls or defense interest could concentrate value in a few gated suppliers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.28