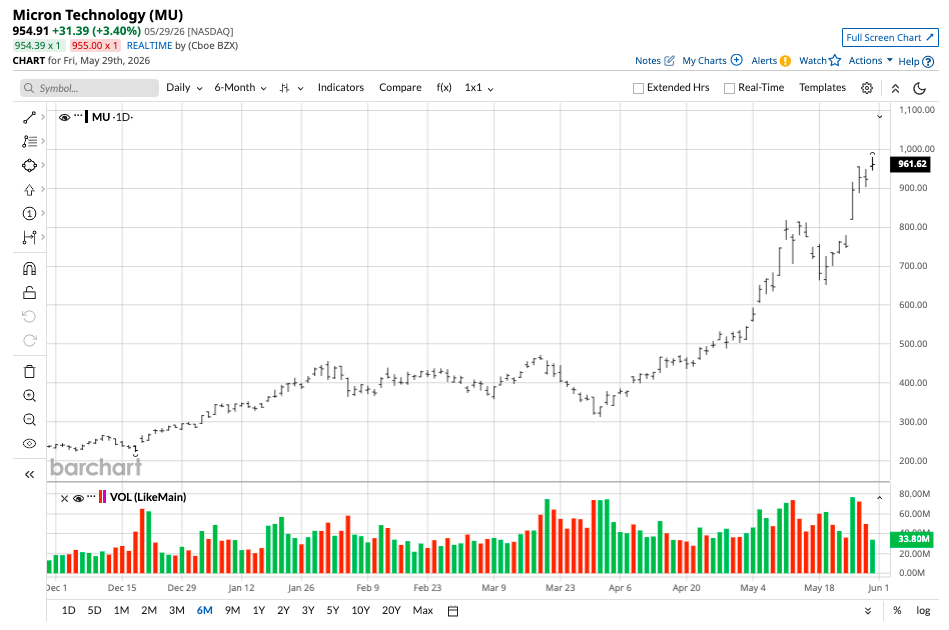

The article argues Micron's $1 trillion valuation is overheated and says investors are wrongly treating it like the next Nvidia. The key concern is that Micron lacks Nvidia’s CUDA-style software moat, making memory chips a commoditized hardware market where Samsung and SK Hynix can eventually pressure pricing and margins. The piece is a cautionary valuation call rather than new operating data, but it may temper sentiment in MU shares.

The key read-through is not a collapse in AI memory demand, but a shift from scarcity pricing to competitive normalization. In this setup, the most fragile part of the recent upside is duration: when capacity additions by the Korean suppliers start to hit the market, incremental pricing power in HBM and server DRAM can compress much faster than revenue growth, which is toxic for a stock priced on near-perfect execution. That makes the trade less about semiconductor demand and more about how long the market can justify peak margins without a moat that prevents substitution.

Second-order winners are likely to be the AI platform buyers, not the memory vendors. If memory pricing eases over the next 6-18 months, hyperscalers should see a modest but meaningful reduction in AI server bill of materials, which improves ROI on incremental model training and inference deployments. That argues for relative support in GOOG and MSFT versus a straight-line continuation in memory names, because cheaper memory can extend capex cycles rather than end them.

The contrarian miss is that the current move may be over-earning from a cycle that still has room, but not enough room to justify a scarcity multiple. Consensus is treating a two-year backlog like a durable franchise; the better framing is that backlog only delays competition, it does not eliminate it. ASML is less exposed to near-term narrative reversal because it monetizes the whole competitive arms race, while the memory producers remain trapped in a commodity-style end market where supply response eventually caps returns.

Near term, the stock can still squeeze higher on momentum and analyst upgrades, so the risk is not immediate fundamental breakdown but multiple compression over the next several quarters as supply visibility improves. The most likely reversal trigger is evidence that HBM capacity is normalizing faster than expected or that customers begin dual-sourcing aggressively. If that shows up in guidance, the market can re-rate the group from 'AI scarcity' to 'good cyclical semiconductor.'

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment