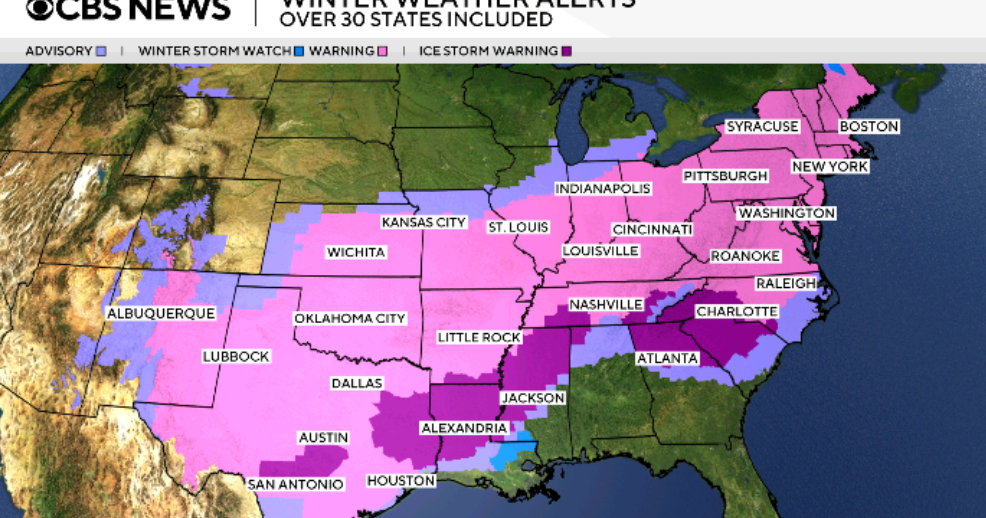

A massive winter storm threatens more than 230 million Americans across 35 states with up to two feet of snow in parts of Kentucky and Virginia and 12–18 inches possible in major cities like New York and Boston; ice accumulations up to 1 inch are forecast across southern states. Nineteen states plus DC have declared emergencies, at least 10 states activated National Guards, FEMA has pre-positioned meals, water, blankets and generators, and over 47 million people are under extreme cold warnings — risks that imply near-term disruptions to power networks, logistics, travel and localized spikes in energy demand and insurance claims.

Market structure: Winners in the next 0–8 weeks are suppliers of heating fuels (natural gas, heating oil), generator/equipment OEMs and rental firms, home-improvement retailers, and power-market participants that can supply capacity during outages; losers are airlines, short-haul logistics, regional retailers without e‑commerce, and insurers exposed to property/auto claims. Ice >0.25" materially increases outage probability and >0.5" is “catastrophic”; expect localized power-price spikes (ISO/SPP/PJM) and a 10–30% uptick in regional gas burn during peak cold hours, pressuring prompt gas balances and spot prices. Risk assessment: Immediate (days) risks are transport disruption and transient spikes in nat‑gas and diesel; short-term (weeks–months) risks include insurance loss accruals, debt/equity volatility at small utilities, and supply-chain delays for heavy equipment; long-term (quarters–years) could see accelerated grid hardening regulation and capex. Tail scenarios: prolonged multi-week outages across multiple ISOs causing multi–$bn insured losses and political pressure for large federal resilience funding; contagion paths include municipal revenue stress and contractor capacity shortages. Trade implications: Tactical plays favor long short‑duration natural‑gas exposure, long HD/LOW for emergency HVAC/parts demand, and selective long CAT/AECOM for equipment/repair backlog; short volatility/earnings for airlines (JETS, AAL) and trucking (FDX) around the next 2–4 weeks. Use options to time risk: 4–8 week UNG call spreads and 1–3 week JETS puts to express asymmetric outcomes while limiting capital at risk. Contrarian angles: The market may underprice multi‑quarter beneficiaries of resilience spending — engineering/utility O&M/line contractors (ACM, AEP) could outperform if federal/state rebuilding programs >$5–10bn arrive. Insurers’ stock drops may be overdone if losses stay within historical winter-storm bands; conversely, small regulated utilities with weak balance sheets could face step-up financing costs and credit stress, creating selective short opportunities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45