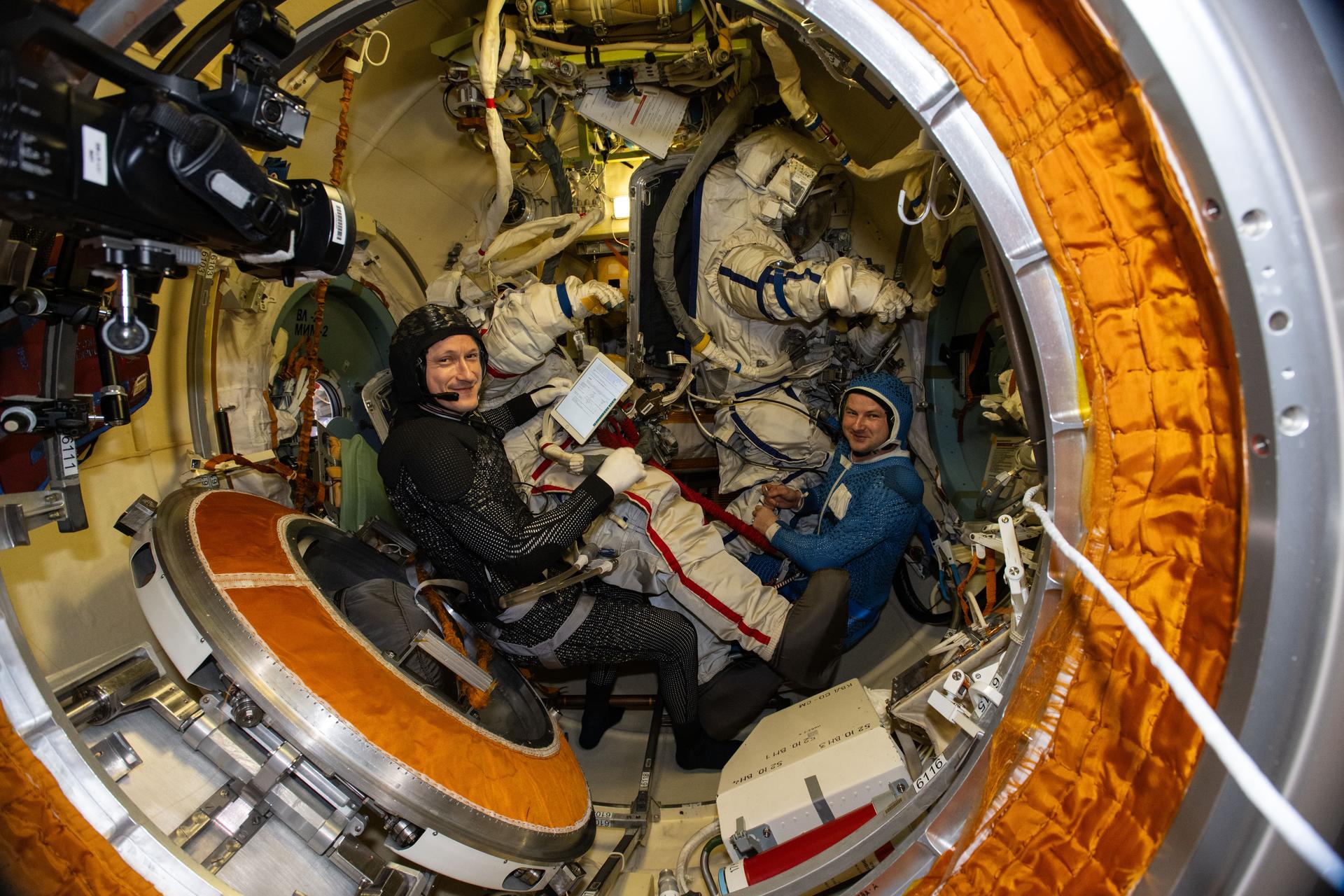

Two Roscosmos cosmonauts are scheduled to conduct a roughly five-hour spacewalk at about 10:15 a.m. EDT to retrieve two science experiments and install a solar-radiation measurement device outside the International Space Station. The work includes servicing experiments on the Poisk, Nauka, and Zvezda modules and, if time allows, photographing a Progress 94 cargo spacecraft antenna that failed to deploy in March. The event is routine station maintenance and science operations with minimal market impact.

This is a small but useful read-through on where space-industry capital is concentrating: not launch hype, but on-orbit servicing, robotics, and microgravity-enabled materials science. The incremental signal is that the space station remains a live testbed for technologies that map directly into dual-use infrastructure and defense applications, especially sensors, autonomous manipulation, and radiation monitoring. That tends to favor the ecosystem around robotics, optics, materials, and mission-enabling subsystems more than the headline launch providers. The second-order winner is the supply chain for space-qualified electronics and sensing hardware. Any success in measuring solar bursts or recovering semiconductor data reinforces demand for radiation-hardened components, photonics, and environmental telemetry, which are higher-margin and harder to commoditize than commodity launch services. Over a 12-24 month horizon, that supports primes and subsystem suppliers with exposure to NASA/DoD procurement rather than pure-play space tourism or launch names that still trade on sentiment. The contrarian angle is that the market often overweights the theatrical aspect of EVA activity and underweights the boring, recurring budget line items: inspection, servicing, data capture, and robotic manipulation. Those are exactly the capabilities that become sticky as agencies shift from one-off missions to sustained orbital infrastructure. If anything, this suggests the real alpha is in companies selling picks-and-shovels for orbital maintenance, not in the most visible space equities. Tail risks are mostly execution and budget timing: any EVA anomaly, delayed experiment retrieval, or hardware failure is a reminder that orbital operations remain fragile and can slow procurement cycles for months. The upside catalyst would be a follow-on announcement that the recovered data is commercially valuable or that the solar-radiation payload feeds into a broader procurement program. In that case, the re-rating could show up first in high-quality defense/space suppliers with backlog visibility rather than in the broader space basket.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05