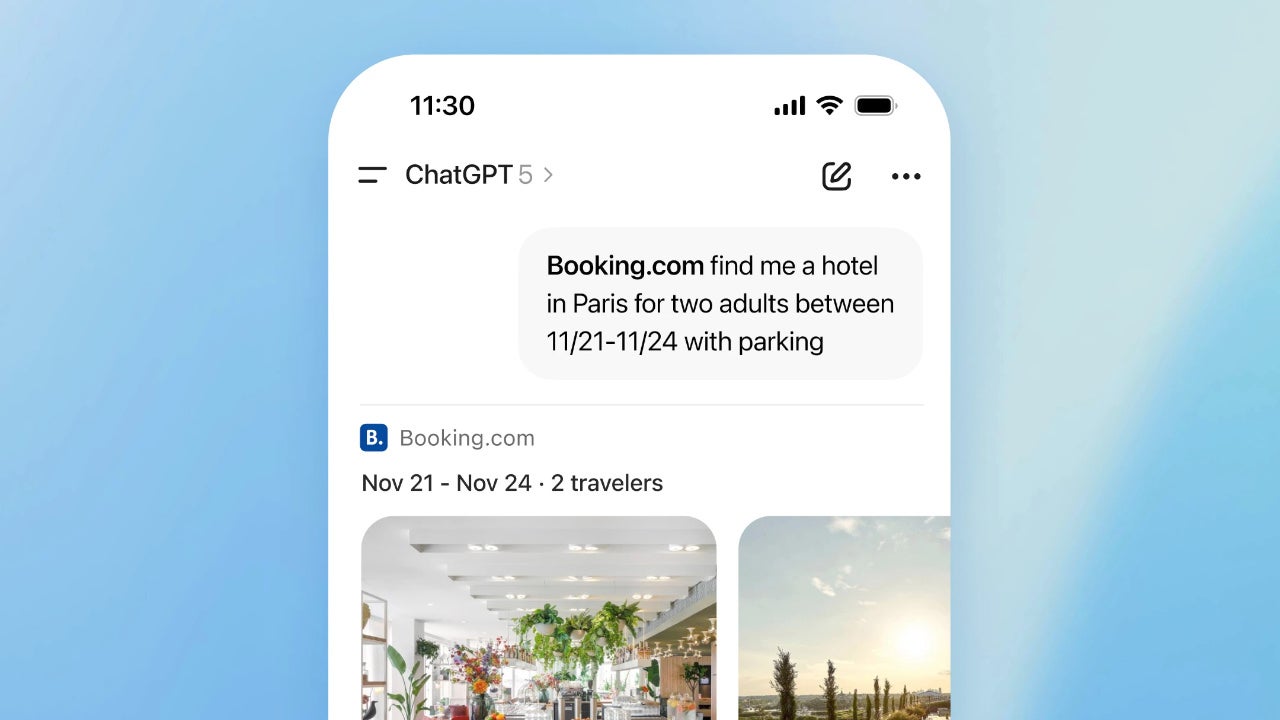

OpenAI has rolled out an in-chat App Store and an Apps SDK (beta) that lets users discover, install and invoke third-party services directly within ChatGPT via a tools menu or @mentions, converting previous 'connectors' into native apps (examples include Spotify, Adobe Photoshop, Zillow, Canva and DoorDash). The platform exposes what data can be shared and shows privacy policies, allows users to disconnect apps instantly, and signals contextual app suggestions—positioning ChatGPT as an operational platform rather than a pure text generator. For investors, the move expands monetization and developer ecosystem opportunities while raising platform-competition and data-privacy considerations that could influence partners, incumbents and startup activity in the AI application stack.

Market structure: OpenAI’s in-chat App Store accelerates platform aggregation: native conversational UX will shift user journeys from standalone apps to API-backed actions. Direct beneficiaries are high-engagement consumer apps with commerce hooks (SPOT, DASH) that can capture incremental MAU/GMV; legacy storage/sync plays (DBX) face neutral-to-negative pressure if they remain utility-only. Expect a 1–3% uplift in engagement-driven revenue for integrated consumer apps within 3–12 months; pricing power for proprietary apps may rise as placement/SDK fees emerge. Risk assessment: Tail risks include regulatory intervention on bundling/privacy (FTC/EC probes within 6–18 months), major data breach from SDK misuse, or partner pushback over revenue share; low-probability but >10% systemic impact on valuations. Near-term (days–weeks) volatility around partnership announcements; short-term (1–6 months) monetization signals from developer adoption; long-term (≥2 years) platform economics could reprice multiples across consumer software. Hidden dependency: monetization depends on contract terms and end-user consent flows—OpenAI policy shifts can rapidly change economics. Trade implications: Favor exposure to SPOT and DASH to capture engagement -> revenue conversion; use time-limited option structures to limit capital while capturing asymmetric upside (3–9 month call spreads). Hedge legacy SaaS/utility names (DBX) via puts or pair trades. Reallocate 3–6% net from broad software beta into consumer API-exposed names and reduce pure-play UI/SaaS cyclicals by similar magnitude. Contrarian angles: Market may underprice regulatory and revenue-share risk—Apple/Google App Store precedent shows winners can face fee/regulation backlash that compresses take-rates. Conversely, consensus may underappreciate rapid GTM leverage: if developer adoption exceeds 1,000 apps in 90 days, platform effects could compound faster than multiples imply. Unintended consequence: commoditization of app interfaces could hurt smaller indie apps even as marquee partners gain disproportionate capture.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment