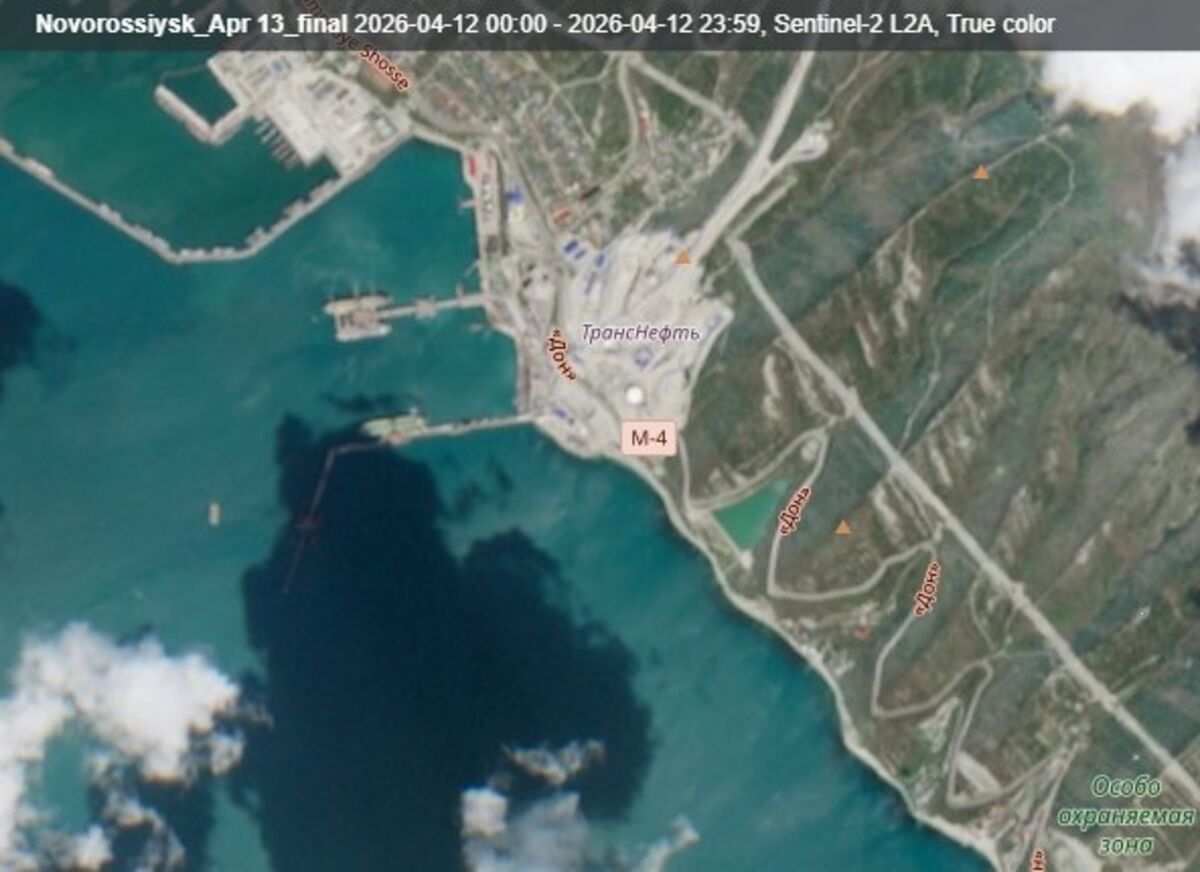

Russia’s biggest Black Sea crude export terminal in Novorossiysk remains partially offline, with berths 1 and 1a still empty after Ukrainian drone attacks last week. The disruption is limiting loadings of Suezmax and Aframax tankers at Transneft’s Sheskharis terminal, creating a near-term supply bottleneck for Russian crude exports. The issue has direct implications for energy flows and shipping logistics, though the broader market impact depends on how long the outage lasts.

The immediate market implication is not the headline loss of barrels, but the quality of barrels being removed from the system. When the large Suezmax/Aframax slots stay offline, the disruption disproportionately constrains flexible export flows and raises the probability that displaced crude either piles into floating storage or is forced onto smaller, more expensive logistics channels. That tends to widen regional differentials before it moves flat price, because traders first price vessel scarcity and destination flexibility rather than outright supply loss. The second-order effect is that this is a margin shock for the entire arb chain: shipowners with clean spare tonnage gain, while Russian export optimization weakens because every additional day of berth impairment increases demurrage, makes cargo scheduling less reliable, and compresses the seller’s ability to defend volume. Over a 1-3 week horizon, that is supportive for seaborne crude benchmarks and for refiners that can source alternative grades, but over 1-3 months the bigger trade is the re-routing premium into Atlantic Basin supply chains and higher insurance/war-risk costs for Black Sea liftings. The market may be underestimating how quickly a “limited outage” can turn into a persistent logistical discount if buyers begin to treat the port as operationally fragile. The real risk is not a permanent outage but a repeated stop-start regime, which is worse for price discovery because it creates intermittent supply shocks without clear resolution. If repairs are fast and loadings normalize, the move fades; if there is another strike or evidence of persistent terminal vulnerability, expect a sharper repricing in freight, regional crude spreads, and Russian export discounts rather than a sustained spike in Brent. From a contrarian angle, this may be less bullish for outright oil than consensus expects if the market is already long geopolitical risk and global demand is softening. In that scenario, the cleaner expression is relative: long freight and supply-chain beneficiaries, short the most exposed Russian-linked discount compressors, and avoid chasing spot crude unless confirmation appears in actual loadings and tanker fixtures.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35