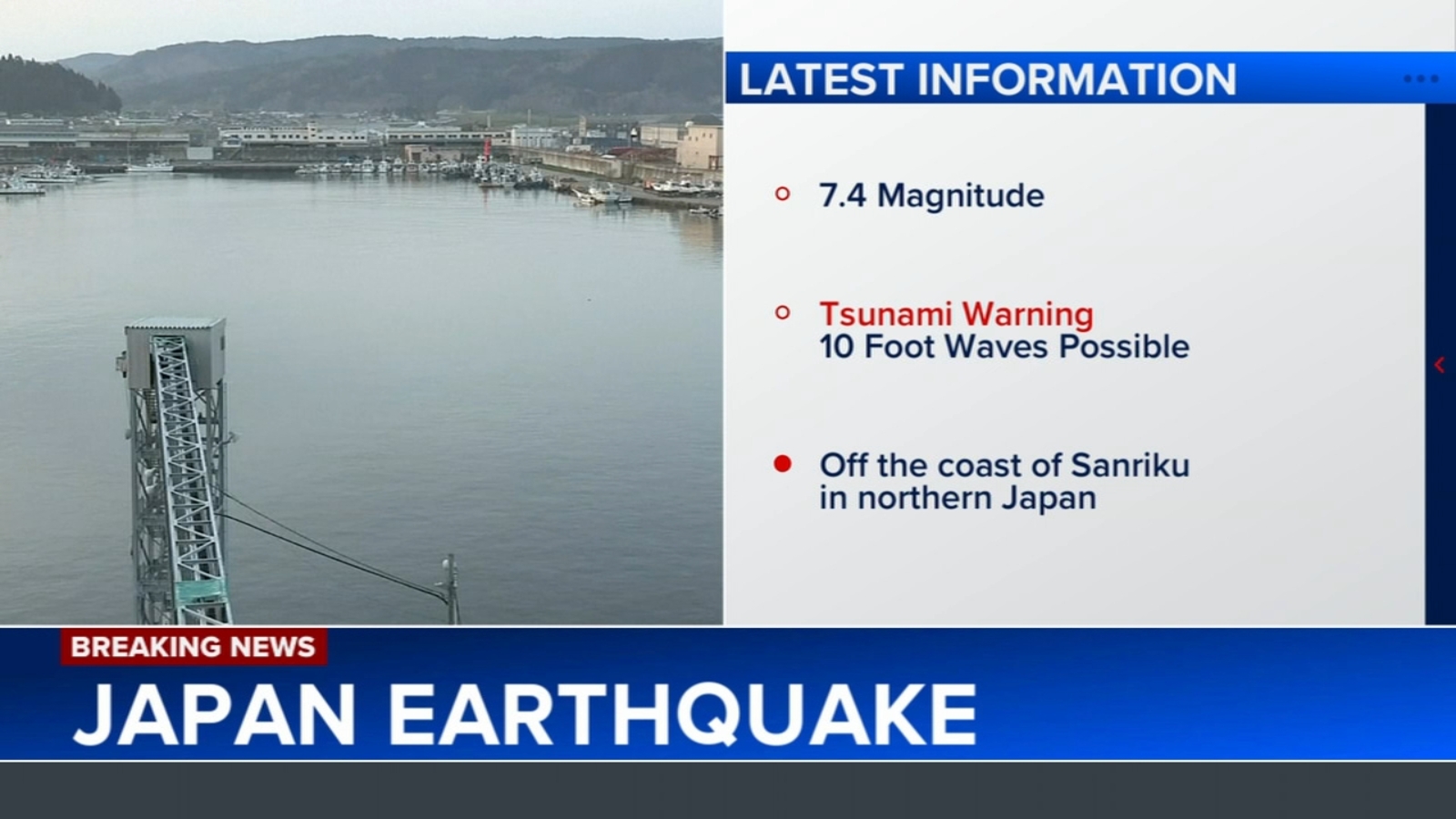

A preliminary magnitude 7.5 earthquake struck off northern Japan at around 4:53 p.m. local time, triggering tsunami alerts and evacuation advisories across Iwate, Aomori, southeastern Hokkaido, and parts of Miyagi and Fukushima. A tsunami of about 80 cm was detected at Kuji port, with authorities warning waves could reach up to 3 meters and urging residents to move to higher ground. The event raises immediate risk to local infrastructure and safety, though the article does not yet report major damage or casualties.

This is a volatility event first and a macro event second. The immediate market focus should be on the “systems” exposed by a severe offshore quake: port throughput, coastal logistics, rail/road interruptions, and power reliability. Even when physical damage is limited, the second-order hit comes from precautionary shutdowns and inspection delays, which can create a 1-3 day dislocation in regional supply chains and a much larger hit to sentiment around Japan cyclical exposure.

The biggest embedded risk is not the initial quake, but the aftershock window and any escalation in evacuation scope. A meaningful surprise would be a move from advisory to broader mandatory evacuations or any evidence of infrastructure damage near critical industrial corridors; that would extend disruption from days into weeks and force corporates to revise output assumptions. The market usually underprices the tail that follows a “manageable” tsunami alert: temporary closure of ports, suspended factory shifts, and rerouting costs that hit margins before earnings revisions show up.

The contrarian angle is that the selloff in Japan-specific risk assets may be too broad if the event remains localized. Japan’s industrial base has spent years hardening disaster response, so the equity impact may concentrate in logistics, insurers, and utilities rather than the wider market. If damage stays light, the better expression is to fade panic in exporters with diversified global revenue while avoiding highly levered domestic-cycle names tied to northern supply chains.

The nuclear angle is a long-tail sentiment overhang rather than an immediate operational thesis. Even without direct plant damage, any mention of Fukushima in the market narrative can reawaken premium into utilities and reactivate risk aversion around coastal power assets. That effect can persist longer than physical disruption, especially if foreign investors reduce Japan exposure mechanically for several sessions.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35