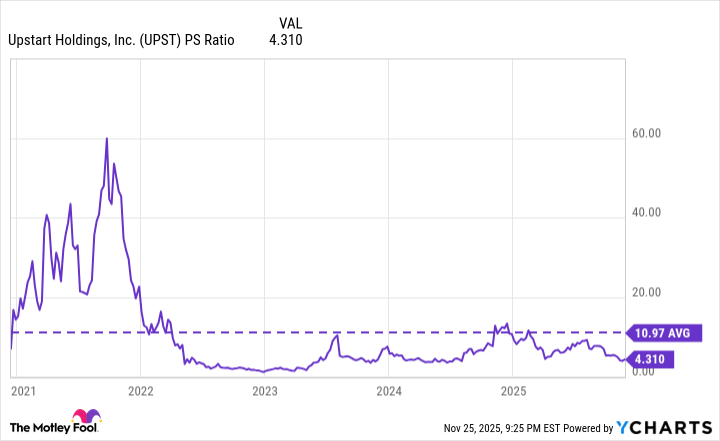

Upstart reported strong third-quarter results with $277 million in revenue (up 71% YoY), $31.8 million GAAP net income versus a $6.7 million loss a year earlier, and $71 million adjusted EBITDA (up 26% YoY); originations surged 128% YoY to 428,056 and 91% of applications were processed autonomously by its AI. Management noted a more conservative approval rate of 20.6% (down from 23.9% sequentially) which produced a modest revenue miss versus guidance, but analysts tracked by The Wall Street Journal carry an average $55.14 price target (implying ~32% upside) and a high target of $80 (91% upside); the company is expanding into auto and HELOC lending and cites a multi‑trillion-dollar total addressable market.

Market structure: Upstart (UPST) is a direct beneficiary as banks, credit unions and fintechs outsource decisioning — expect Upstart to capture share from legacy scoring (FICO) over 3–5 years if its approval/IRR advantages persist. Winners: UPST, partner banks that securitize more efficient origination flows, cloud/ML vendors; losers: legacy score vendors (FICO) and manual underwriting desks. Faster automated approvals increase supply of consumer and auto loans into markets, likely raising ABS issuance by +10–30% over 12–24 months if originations sustain the current run-rate. Risk assessment: Key tail risks are regulatory intervention (CFPB fair-lending audit or explainability mandate) and model regime shift in a sharp macro downturn that increases loss severities >200–300 bps versus current stress assumptions. Immediate (days) risks: earnings/approval-rate misses; short-term (weeks–months): funding/ABS demand volatility; long-term (years): sustained adoption or legal restriction. Hidden dependency: funding concentration via warehouse lines and securitization investors — a pullback could compress originations faster than credit performance indicates. Trade implications: Direct: establish a modest long in UPST using instruments that limit downside (call spreads or 6–9 month LEAPS) to target a rerating to P/S ~8–11 if revenue growth stays >40% YoY; pair: long UPST vs. short FICO (ticker FICO) to express secular share shift. Options: buy 6–9 month UPST 1–2 call spreads (strike selection 20–40% OTM) or sell a backed put spread for yield if willing to own at a 30% discount. Rotate 3–6% of risk budget into fintech/ABS exposure and trim traditional bank credit exposure by 1–2%. Contrarian angles: Consensus underestimates funding and regulatory friction — adoption may be non-linear: wins with mid-tier banks but slower uptake among large banks and international markets. Market may be underpricing credit-cycle sensitivity (UPST benefited in 2022–23, but a 2–3% unemployment shock could materially widen default curves). Historical parallels: credit scoring innovations often take 5–10 years to displace incumbents; downside would be amplified if auditors/regulators force transparent, slower models.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment