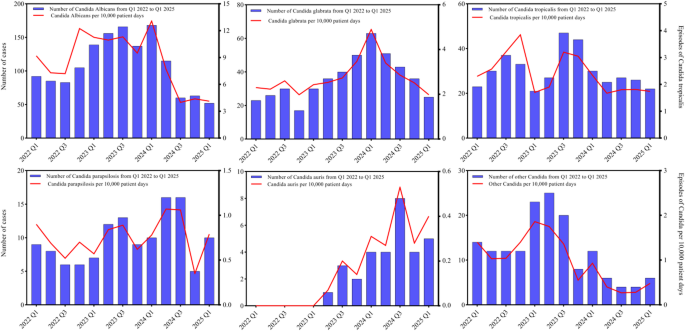

A tertiary hospital in Guangzhou reported 31 clinically significant Candida auris isolates through Q1 2025 amid a national rise to 1,166 cases by end-2024; isolates showed a 77.42% resistance rate to fluconazole and 3.23% to amphotericin B. C. auris patients had a longer median length of stay (17 vs. 12 days) and higher mortality, and multivariable analysis identified ICU admission (OR 1.502), hypertension (OR 1.476), immunosuppression (OR 1.179) and indwelling devices (OR 1.265) as independent risk factors. Implications include higher hospital resource use, pressure on infection-control and diagnostics, and potential demand for effective antifungals and improved surveillance.

Market structure: Acute rise of Candida auris cases (31 isolates at one tertiary center, 1,166 national cases by Dec 2024) benefits diagnostics and infection‑control vendors—PCR/NGS and MALDI‑TOF consumables (Thermo Fisher TMO, Roche RHHBY, bioMérieux BIM.PA) and hospital disinfectant/PPE suppliers (Ecolab ECL, 3M MMM). Hospitals and long‑stay care facilities face higher OPEX (screening + environmental cleaning), compressing operator margins and raising pricing power for suppliers that provide single‑use screening kits and chlorine‑based disinfectants. Incremental demand: expect a regional uplift in diagnostics/disinfectant volumes of ~10–25% over 3–12 months if active screening policies expand. Risk assessment: Tail risks include mandated national screening or procurement tenders (high‑impact: multi‑quarter procurement; probability moderate over 6–12 months) and outbreak‑driven ward closures that cause revenue shocks for hospital operators. Short term (days–weeks) sees localized screening volume spikes; 1–6 months covers procurement and inventory restocking; 1–3 years affects guideline shifts and antifungal R&D funding. Hidden dependencies: commercial AFST overcalling amphotericin resistance (SYO) can misdirect treatment and purchasing; chlorine supply/logistics and PPE capex are second‑order constraints. Key catalysts: CDC/EUCAST breakpoint updates, large hospital system tenders, regional outbreak reports. Trade implications: Direct actionable plays—overweight diagnostics and disinfectants: initiate 1.5–3% positions in TMO and ECL to capture 6–12 month procurement cycles; use 9–12 month call spreads to limit capital and capture asymmetric upside if mandates arrive. Relative trade: long diagnostics (TMO or RHHBY) vs short HCA Healthcare (HCA) 1% to express margin divergence over 3–9 months. Entry window: deploy into weakness within 2–8 weeks; trim 30–50% on signs of mandate reversals or quarterly guidance beats. Contrarian angles: Consensus may overestimate permanent demand — historical parallels (MRSA/VRE) show initial procurement spikes then reversion to baseline in 12–24 months as protocols standardize and cheaper screening emerges. Reaction could be underdone for specialty disinfectant makers (ECL) but overdone for hospital operator doom; unintended consequence: aggressive chlorine use accelerates capex cycles for equipment replacement, benefiting medical device firms (e.g., Stryker SYK) — consider small tactical exposure there as a hedge.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35