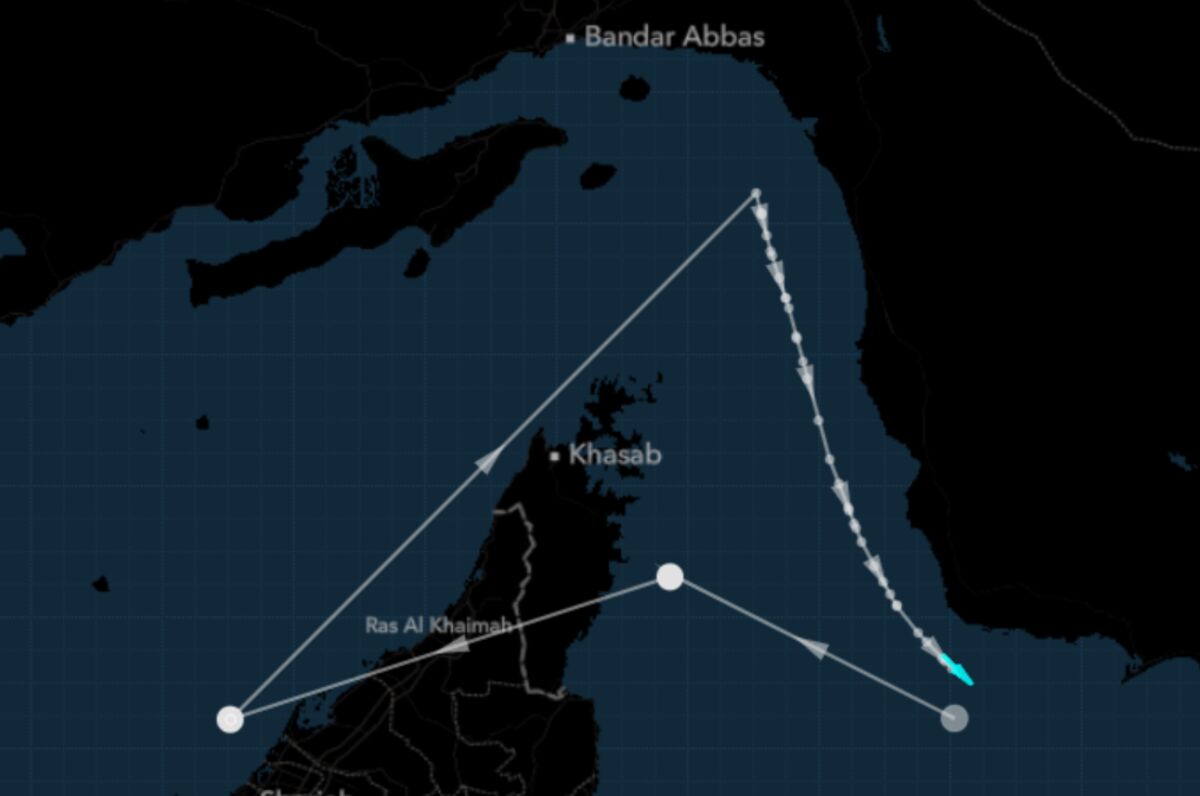

A vessel identifying as LNG carrier Jamal exited the Strait of Hormuz despite records indicating the same tanker was beached at an Indian demolition yard and being broken up in October. The episode suggests identity spoofing or reuse of identities to transit Hormuz amid the Middle East war, raising shipping security and insurance concerns. Immediate market impact is limited, but the tactic increases operational and supply-chain transparency risks for LNG logistics and insurers.

The evolving use of false identities and ad-hoc routing is enlarging the ‘friction tax’ on Middle East seaborne energy flows: expect persistent upward pressure on war‑risk and hull & machinery premiums (order-of-magnitude moves, e.g., +50–200% in past regional flare-ups) and higher spot charter rates for specialized LNG/clean product tonnage over the coming weeks. That friction translates quickly into per-voyage cost increases — rerouting around chokepoints or adding convoy requirements can add single‑voyage fuel and time costs that compound across a 3–6 month contracting window, squeezing thin-margin refiners and freight‑rate sensitive operators first.

Second‑order winners are owners of modern LNG carriers and flexible transshipment assets able to capture scarcity rents and shorter-haul exporters who can pivot supply (e.g., US Gulf/Atlantic suppliers) — they avoid extended detours and can press premium spot charters. Losers include short‑haul container and conventional tanker operators that lack LNG‑grade or ice‑class flexibility, commodity processors reliant on tight delivery windows (chemical, fertilizer), and banks with concentrated legacy shipping loans facing covenant pressure if earnings slip for two consecutive quarters. Compliance and KYC costs for charterers and financiers will rise meaningfully, favoring larger counterparties with scale to absorb AML/sanctions overhead.

Key tail risks and catalysts: in days-to-weeks, naval incidents or formal sanctions enforcement could spike premiums and force temporary route closures; in 1–6 months, systemic rerouting and contract re-pricing occur and could be partially reversed if a diplomatic de‑escalation or multinational escort arrangement is announced. A full prolonged closure of a major choke point remains a low‑probability, high‑impact event that would shock oil and LNG spreads (30–50% moves in extreme scenarios) and break typical hedging correlations.

Implementation should focus on capturing scarcity rents and asymmetry: long selective LNG owners/exporters and short freight‑sensitive container/tanker names or buy protection via options on oil/energy equities. Position sizing should assume elevated event risk and include tight, time‑based exits (3–9 months) tied to visible changes in war‑risk premiums or naval posture.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00