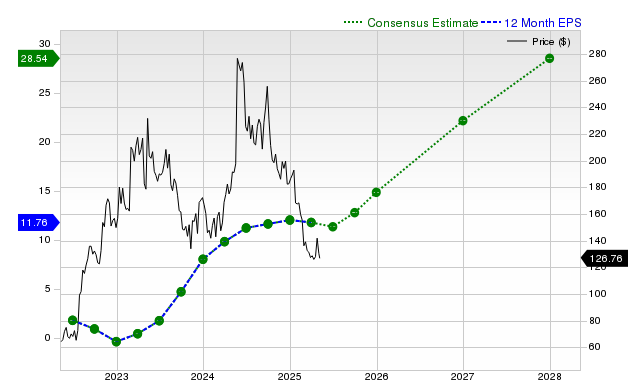

First Solar (FSLR) shares have significantly outperformed, gaining 12.6% over the past month, driven by strong projected earnings and revenue growth, including an anticipated 47.4% year-over-year EPS increase for the current quarter and 74.2% year-over-year revenue growth. Despite these robust fundamentals, Zacks maintains a #3 (Hold) rank for FSLR, suggesting the stock may perform in line with the broader market in the near term, influenced by stable recent earnings estimates and a valuation assessed as on par with peers.

First Solar (FSLR) has demonstrated significant recent momentum, with its shares returning +12.6% over the past month, substantially outperforming both the S&P 500 composite's +3.5% gain and the broader solar industry's +9.3% rise. This performance is underpinned by robust forward-looking consensus estimates, which project remarkable growth. For the current quarter, analysts anticipate a 74.2% year-over-year revenue increase to $1.55 billion and a 47.4% EPS increase to $4.29. The outlook for the current and next fiscal years also remains strong, with expected EPS growth of +26.3% and +52.2%, respectively. However, these bullish forecasts are tempered by several factors. Analyst estimates have remained largely unchanged over the past 30 days, and the company's recent earnings surprise history is inconsistent, having surpassed EPS estimates only once in the last four quarters. Furthermore, the stock carries a Zacks Rank #3 (Hold), suggesting its near-term performance may align with the broader market rather than continue its pronounced outperformance. This is supported by a 'C' grade for valuation, which indicates the stock is trading at par with its peers, implying that the strong growth prospects may already be reflected in the current price.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment