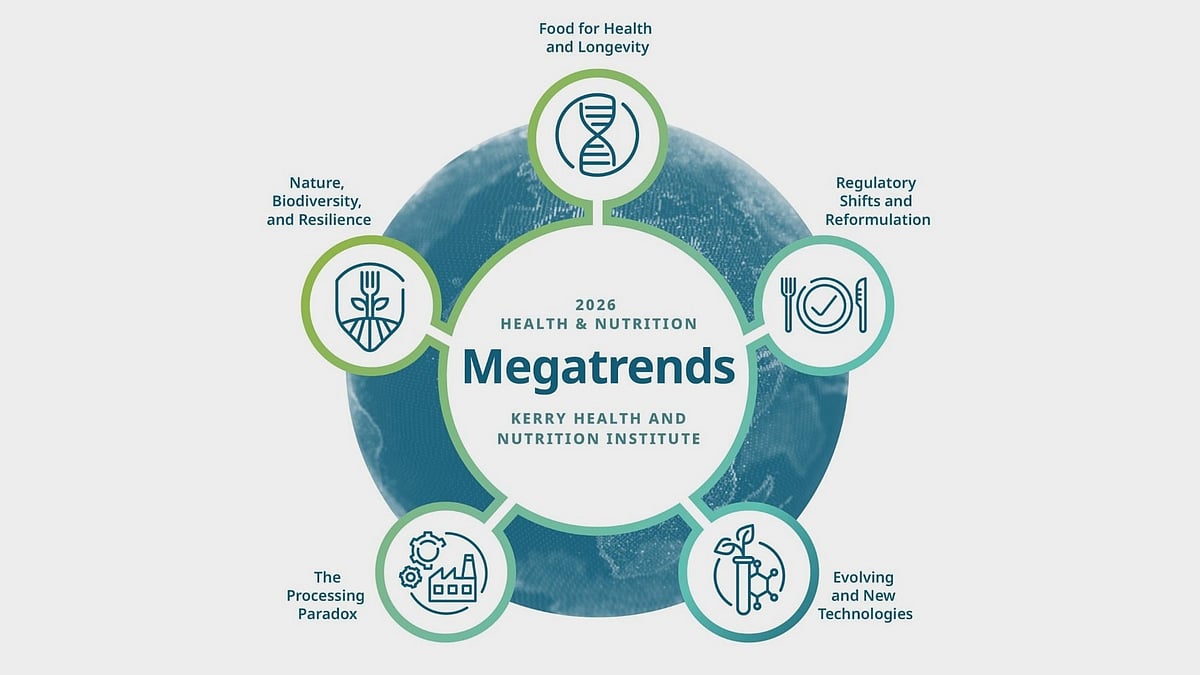

Kerry Health & Nutrition Institute released its 2026 Health and Nutrition Megatrends highlighting five drivers reshaping food systems: nutrition for health and longevity (noting one in six people projected to be over 60 by 2030), regulatory-driven reformulation (front-of-pack labelling, sugar/sodium targets), rapid adoption of AI/biotechnology and advanced bioprocessing (precision fermentation, enzyme engineering), the processing paradox balancing convenience and nutrition, and nature-positive supply chains (regenerative agriculture, upcycling). The trends point to investment and product opportunities across functional foods, personalised nutrition, reformulation technologies and resilient/ sustainable sourcing that food, ingredient and biotech investors should monitor.

Market structure: Winners will be specialty ingredients, flavors and precision-fermentation-capable processors that capture premium margins (e.g., IFF, Givaudan, Ingredion, ADM) while commodity sugar and legacy high-sodium/sugar branded foods face demand erosion and reformulation cost pressure. Expect 100–300 bps of gross-margin reallocation over 12–36 months toward nimble ingredient specialists and biotech partners as retailers and regulators force reformulation and transparency. Cross-asset: sugar and bulk sweetener prices likely see downward pressure (3–15% over 6–18 months) while capex-led firms may issue debt, modestly steepening some food-sector credit spreads. Risk assessment: Tail risks include aggressive regulatory mandates (10–20% composition targets within 24 months) that can impose 1–3% EBITDA hits on slow adapters, and biotechnology scale-up failures that wipe equity value for small-cap foodtech. Immediate (days) catalysts are retailer labeling/assortment moves; short-term (3–12 months) is reformulation execution; long-term (2–5 years) is adoption of precision fermentation and biodiversity supply chains. Hidden dependencies: enzyme/IP access, contract-manufacturer capacity and ingredient bottlenecks can create second-order margin shocks. Trade implications: Direct plays — establish 2–3% long positions in IFF and ADM for ingredient/fermentation exposure and 1% long in Ginkgo (DNA) via 9–12 month ATM calls to capture biotech adoption; short 1–2% positions in legacy snack names with heavy sugar/sodium exposure (K, GIS) using 6–12 month puts as hedge. Pair trade — long Givaudan (GIVN.SW) vs short Kellogg (K) size 1–1.5% each, 12‑18 month horizon; rotate portfolio +4–6% weight into specialty ingredients/biotech from staples over next quarter. Entry window: 0–6 weeks; exit on +25–40% move, or on regulatory announcement reversing thesis. Contrarian angles: Consensus underestimates processing nuance — many processed products will gain market share if reformulated affordably, so large-cap staples that can execute reformulation (Nestle, PepsiCo) may be underpriced versus small foodtech hype names. Historical parallel: trans-fat reformulation rewarded incumbents who invested R&D; the overhyped small-cap fermentation names priced for perfect scaling are vulnerable to dilution and execution risk. Unintended consequence: aggressive sugar substitutes/regulators backlash could shift demand back to natural-ingredient winners, creating volatile rotation opportunities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35