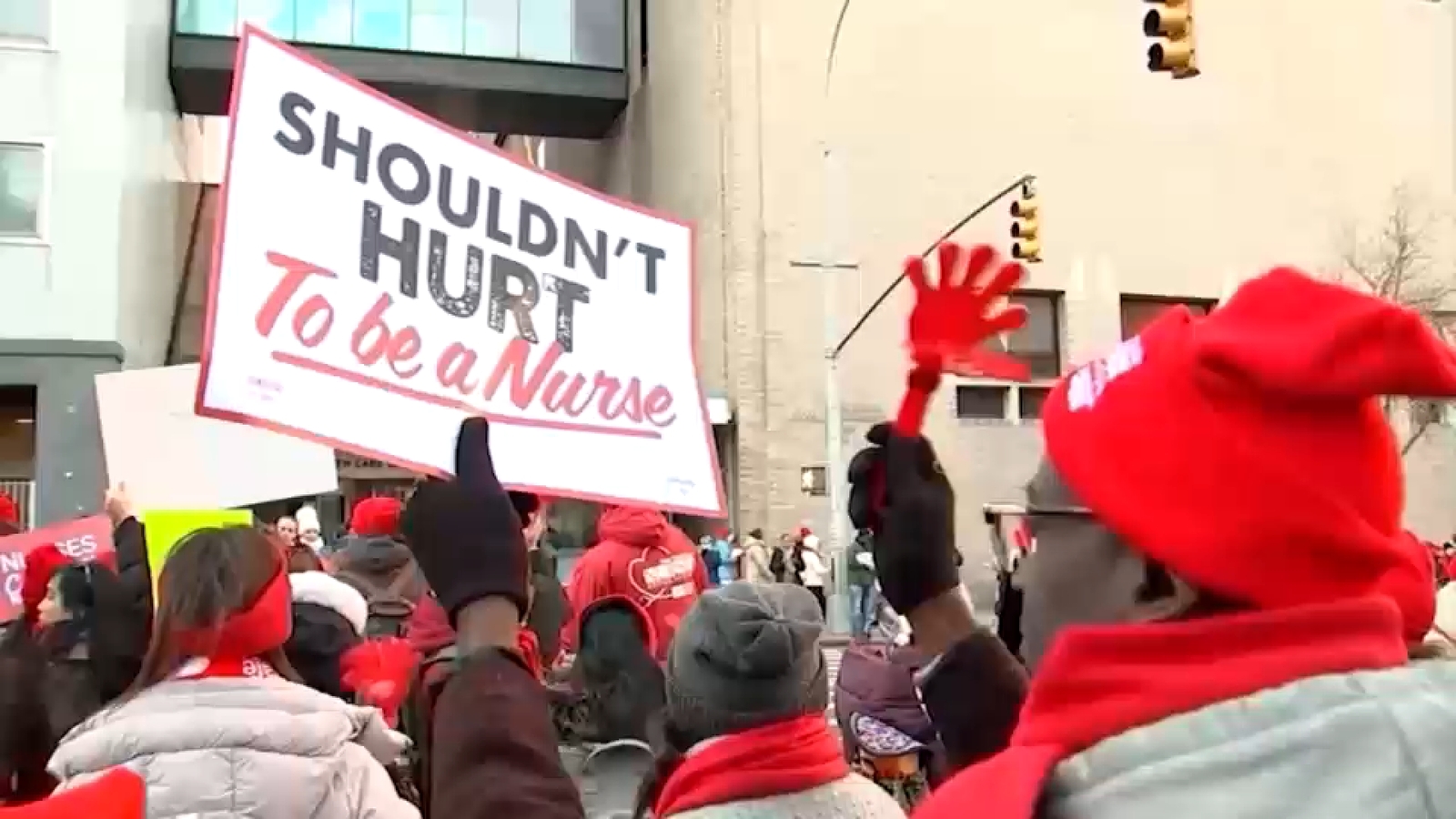

New York Presbyterian nurses voted overwhelmingly to ratify a new contract, ending a 41-day strike and returning the final group of striking nurses to work next week; the agreement includes the hospital system's first contract protections addressing artificial intelligence. Thousands of nurses at Montefiore and Mount Sinai are already back on the job, reducing operational disruption risk for major NYC hospital systems; the development is likely to have minimal direct market impact but signals that labor deals in healthcare may increasingly include AI-related provisions.

Market structure: The ratified 41-day NY nurses strike with AI protections is a positive shock to staffing vendors and temp RN markets (expect incremental RN temp-rate uplifts of ~5–10% for the next 1–3 months). Hospital operators face margin pressure — model a 1–3% EBITDA hit if wage increases spread systemically — while pure-play healthcare AI adoption may be delayed or repriced pending contract language. Competitive dynamics favor third-party staffing (elastic supply) and human-in-the-loop AI vendors that can certify safeguards; price discovery will occur over 30–90 days as contracts roll through other systems. Risk assessment: Tail risks include contagion (strikes at 2+ major systems within 90 days) driving sustained operating disruptions and possible state/federal legislation codifying AI workplace limits (6–24 months). Short-term (days–weeks) operational normalization is likely; medium-term (3–12 months) sees potential union leverage replication; long-term (1–3 years) AI still materially accretive but with higher compliance costs. Hidden dependencies: payor contract terms and CMS reimbursement responses could shift cost burden to insurers/providers; watch NLRB/NY labor filings and CMS guidance in the next 30–90 days as catalysts. Trade implications: Express the view by going long staffing services and hedging hospital operator exposure — staffing revenue should reprice faster than hospitals can cut costs. Use options to cap cost: buy call spreads on staffing agency AMN for 3 months to capture a 5–12% move, and buy 6-month put spreads on large hospital operators to hedge 4–8% EPS downside from wage inflation. Rotate modestly into human-in-the-loop healthcare AI software names and away from capital-intensive hospital REITs until wage pass-through clarity emerges. Contrarian angle: The market may overstate long-term negative impact on AI vendors — protections are likely to be procedural (transparency, human sign-off) not outright bans, so do not reflexively short NVDA/ORCL; historical labor settlements typically create transient margin hits (recouped in 6–12 months via rate increases). Unintended consequence: tighter contractual AI controls create a premium for explainable-AI vendors and compliance tooling; look for small-cap specialists to re-rate if they win certification/validation contracts within 6–12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00