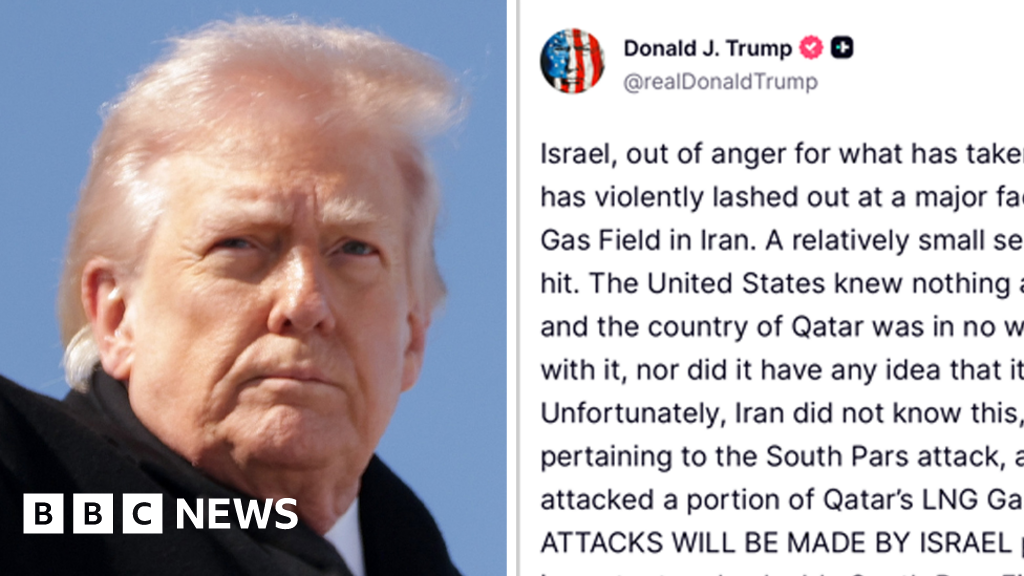

An Israeli strike on the South Pars gas field and Iran's retaliatory strike on a Qatari energy complex have sparked a renewed spike in energy prices and heightened supply risk in global LNG markets. President Trump's public denial of prior US knowledge, coupled with threats to 'massively blow up' South Pars and restrictions on further Israeli strikes, underline coordination frictions and amplify geopolitical uncertainty. Expect elevated oil and gas price volatility and increased political risk for Netanyahu (domestic support) and Trump (potential midterm fallout).

Ambiguity in public coordination between Washington and Jerusalem is itself a market mover: if strikes are perceived as unilateral or poorly signalled, misattribution risk rises and premiums on regional energy and maritime risk will stay elevated for weeks. Expect a two-tier price response — an immediate spot/forward knee in LNG and freight (days–weeks) and a longer-duration risk premium for replacement capacity and insurance (3–12 months) because rebuild of offshore gas infrastructure is capital- and time-intensive.

Second-order winners will be companies that capture upside from wider Asian LNG-JKM spreads (export terminals, tankers, insurance) and defence suppliers that can be contracted quickly; losers include European and US-born gas-intensive industrials (fertilizers, petrochemicals) facing feedstock margin squeeze. The domestic political angle (US election calendar) is a real volatility dampener: the US administration’s rhetorical escalation increases tail-risk pricing but also limits sustained kinetic campaigns, so most of the price move is likely front-loaded.

Catalysts to watch: (1) confirmed physical damage assessments to South Pars (48–96 hours for market reaction), (2) changes in Qatar cargo nominations and re-routing announcements (1–4 weeks), and (3) any US strike authorization or formal deconfliction note with Israel (days–weeks). A contrarian case: markets may be overpricing a multi-year supply shock — physical repair and diplomatic backchannels typically restore much of production within 3–12 months, so medium-term realignment could mean sharp roll-down in forward LNG/freight premia once damage is quantified.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30