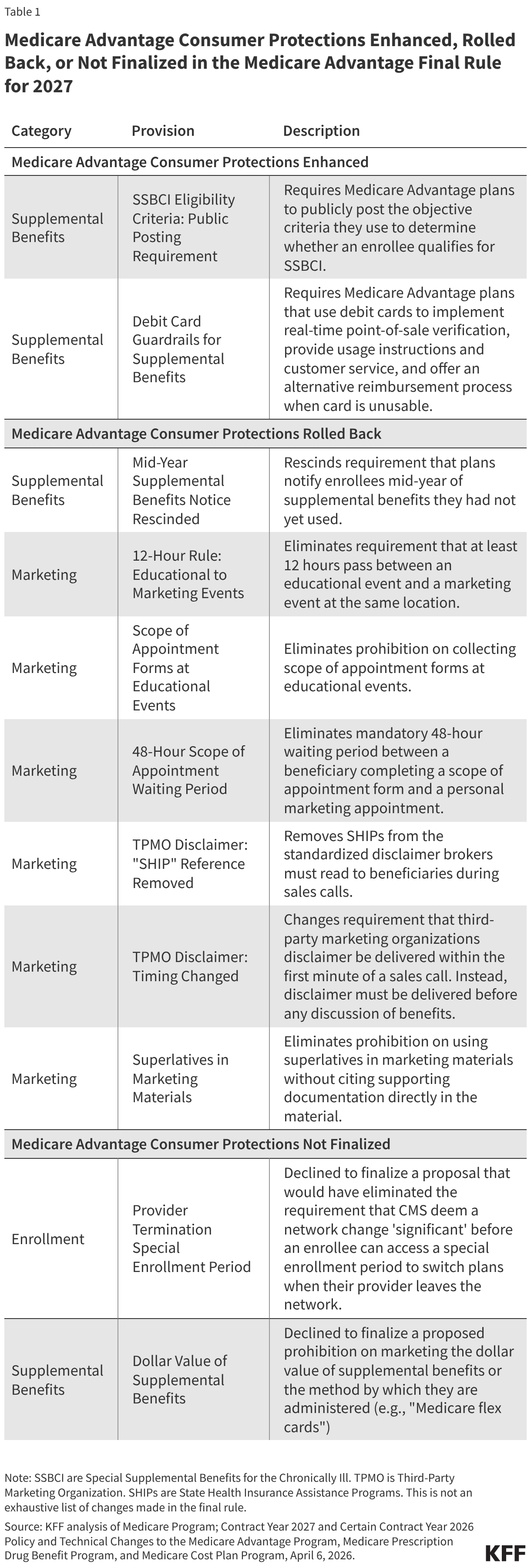

CMS finalized the 2027 Medicare Advantage rule with a mixed set of changes: it enhances transparency for SSBCI eligibility and adds guardrails for debit cards, but rolls back mid-year supplemental benefit notices and several marketing restrictions. The agency also removed SHIPs from required broker call resources and declined to finalize a special enrollment period expansion tied to provider terminations. The rule is consequential for Medicare Advantage insurers and brokers, but the direct market impact is more regulatory than immediate financial.

The near-term economic winner is not the consumer, but the distribution layer inside Medicare Advantage: carriers and broker channels gain more latitude to steer enrollment while the operational burden shifts onto members who must self-navigate a more fragmented benefit architecture. That tends to favor the scale players with the largest broker networks, strongest call-center infrastructure, and the best ability to translate opaque supplemental benefits into perceived plan value. Smaller plans are exposed because they lose one of the few differentiation tools they could use to compete without matching the ad budgets of the nationals.

The bigger second-order effect is that this rule likely increases the advertising efficiency of “extra benefit” claims while reducing the friction that previously suppressed aggressive sales conversion. That should support the economics of third-party lead gen, call-center outsourcing, and comparison-shopping ecosystems over the next 6-18 months, but it also increases the risk of complaint-driven remediation later if enrollments prove low-quality. If that happens, the backlash will arrive with a lag: first through state AG scrutiny and CMS enforcement, then through higher churn and lower persistency for plans leaning hardest on benefit-heavy messaging.

The most interesting contrarian angle is that loosening protections may actually improve near-term enrollment mix for the most sophisticated carriers by reducing compliance overhead and allowing more precise segmentation, even as it looks consumer-negative on its face. The market may be underestimating how much of MA economics is driven by distribution discipline rather than pure benefit generosity. The offsetting risk is reputational: a single headline cycle around misleading marketing or debit-card misuse could quickly reverse the benefit of the rollback and force another tightening round in the next rulemaking cycle.

From a timing standpoint, this is a months-to-years story, not a day trade: the 2027 effective dates create a runway for carriers and brokers to retool scripts and campaigns, while any enforcement response would likely emerge only after utilization and complaint data accumulate. The best setups are those with asymmetric upside to MA enrollment growth but limited downside if the consumer-protection pendulum swings back.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05

Ticker Sentiment