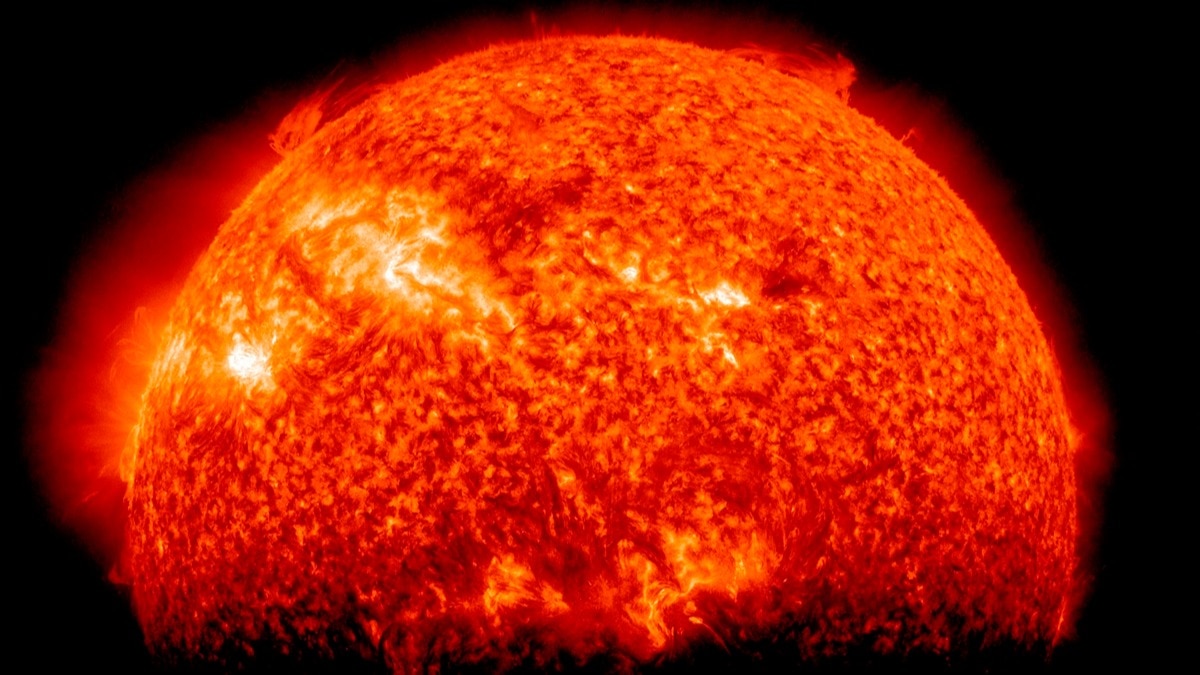

NOAA forecasts a coronal mass ejection (CME) arriving late Jan. 2 that could trigger a G2 (moderate) geomagnetic storm through Jan. 3, capable of inducing voltage irregularities in power systems and degrading high‑latitude radio and navigation signals. Scientists warn the active Solar Cycle 25 may sustain similar space‑weather bursts through much of 2026, posing intermittent risks to satellite operations and airline communications on polar routes while offering an observational opportunity for real‑time study.

Market structure: A G2 storm is operationally moderate but the signal is structural — repeated 2026 space‑weather events raise expected utility and satellite operator capex. Winners: grid‑hardening OEMs (ABB, ETN, GE), defense/space contractors (LHX, NOC, LMT) and copper producers; losers: airlines with polar routing concentration (AAL, DAL) and smaller GEO satellite owners with aging fleets. Expect 5–15% incremental CAPEX cycle for transmission and transformer replacement across 12–24 months if 1–2 additional storms produce outages. Competitive dynamics & supply/demand: Large OEMs and defense primes gain pricing power as governments and utilities seek vetted vendors; small suppliers face capacity bottlenecks (transformer lead times already 9–18 months), pressuring prices and margins. Satellite operators will face replacement and insurance costs, tightening free cash flow by an estimated mid‑single digits for vulnerable players over 2026. Cross‑asset: copper and industrials rally (mid‑single digit upside), modest safe‑haven FX flows into USD/JPY on outages, and short‑dated implied volatility in aerospace and utilities will spike 10–30% around events. Risk assessment & catalysts: Tail risk (Carrington‑class) remains low (<1% annual during peak) but catastrophic; regulatory catalysts (NERC/FERC mandates, FAA polar‑route guidance, insurer rate increases) within 90–180 days would accelerate capex and re‑rate winners. Hidden dependencies include long transformer lead times, reinsurer capacity, and satellite manufacturing bottlenecks which can amplify winners’ margins. Monitor filings/orders from NERC/FERC, FAA advisories, and insurer loss notices as 0–90 day catalysts. Trading environment: Near term (days) expect idiosyncratic swings in airlines and small cap satellites; short‑dated protection is cheap pre‑event but becomes expensive post‑shock. Medium term (3–12 months) favors LHX/NOC and ABB/ETN equities or call spreads; commodities (copper miners) are a tactical 6–24 month thematic. Position sizing should be modest (1–3% per idea) until regulatory signals confirm sustained capex increases.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.10