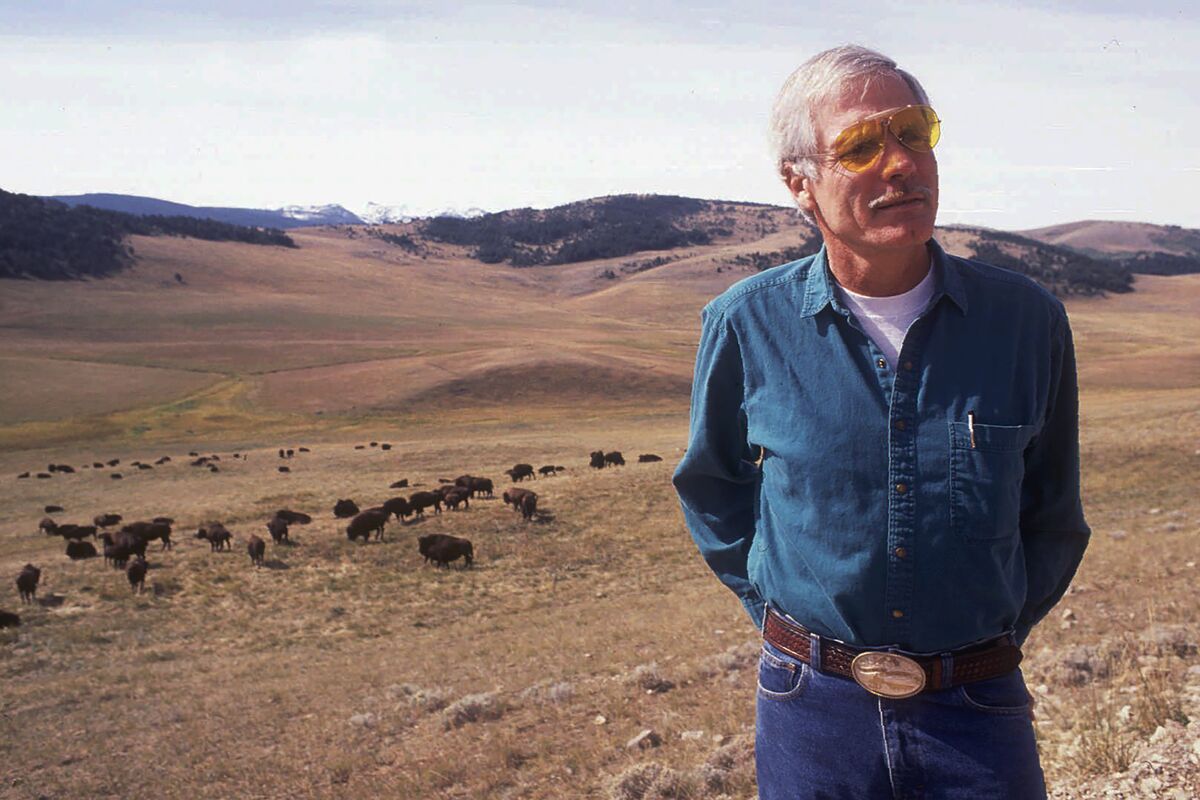

Ted Turner died at age 87, leaving behind 2 million acres of land across the Southeast, Great Plains and West, making him the fourth-largest landowner in the US. His holdings are described as mostly large, contiguous tracts managed to be both economically viable and ecologically sustainable, underscoring a conservation-focused legacy rather than a market-moving business event.

Turner’s land legacy is less a one-off wealth story than a template for the next phase of “real asset” ownership: scale, optionality, and regulatory insulation. Large contiguous tracts with a conservation mandate tend to appreciate differently than fragmented farmland or timberland because they can monetize carbon, hunting leases, water rights, and mitigation credits without requiring development intensity. That favors operators and capital allocators that can underwrite mixed-return land portfolios over pure yield buyers.

The second-order winner is the ecosystem around land stewardship: environmental services firms, timber REITs, ranch aggregators, and conservation-finance platforms. If this model becomes more mainstream, it pushes value from simple acreage ownership toward data, compliance, and project origination — where margins are higher and competitive moats are wider. The loser is the traditional “buy land and wait” playbook, which becomes less attractive if state/federal policy continues to reward verified ecological outcomes rather than passive appreciation.

The main risk is a policy reversal or a dislocation in rural asset values: higher rates, weaker commodity prices, or anti-ESG backlash could compress the value of conservation-linked cash flows over the next 6-18 months. But the deeper catalyst is the opposite — more institutional capital seeking inflation protection with social license, which could re-rate premium land managers and adjacent infrastructure providers over a multi-year horizon. If carbon markets remain illiquid, the thesis stays more narrative than monetizable; if market standards mature, the optionality becomes real cash flow.

Contrarian view: the market may be underpricing the persistence of demand for productive land even in a higher-for-longer rate regime. Unlike office or retail, large rural assets have low replacement supply and can be financed against multiple use cases, so cap-rate expansion may be less severe than consensus expects. The best risk/reward is not to chase headline land prices, but to own the picks-and-shovels that help monetize and certify land utility.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05