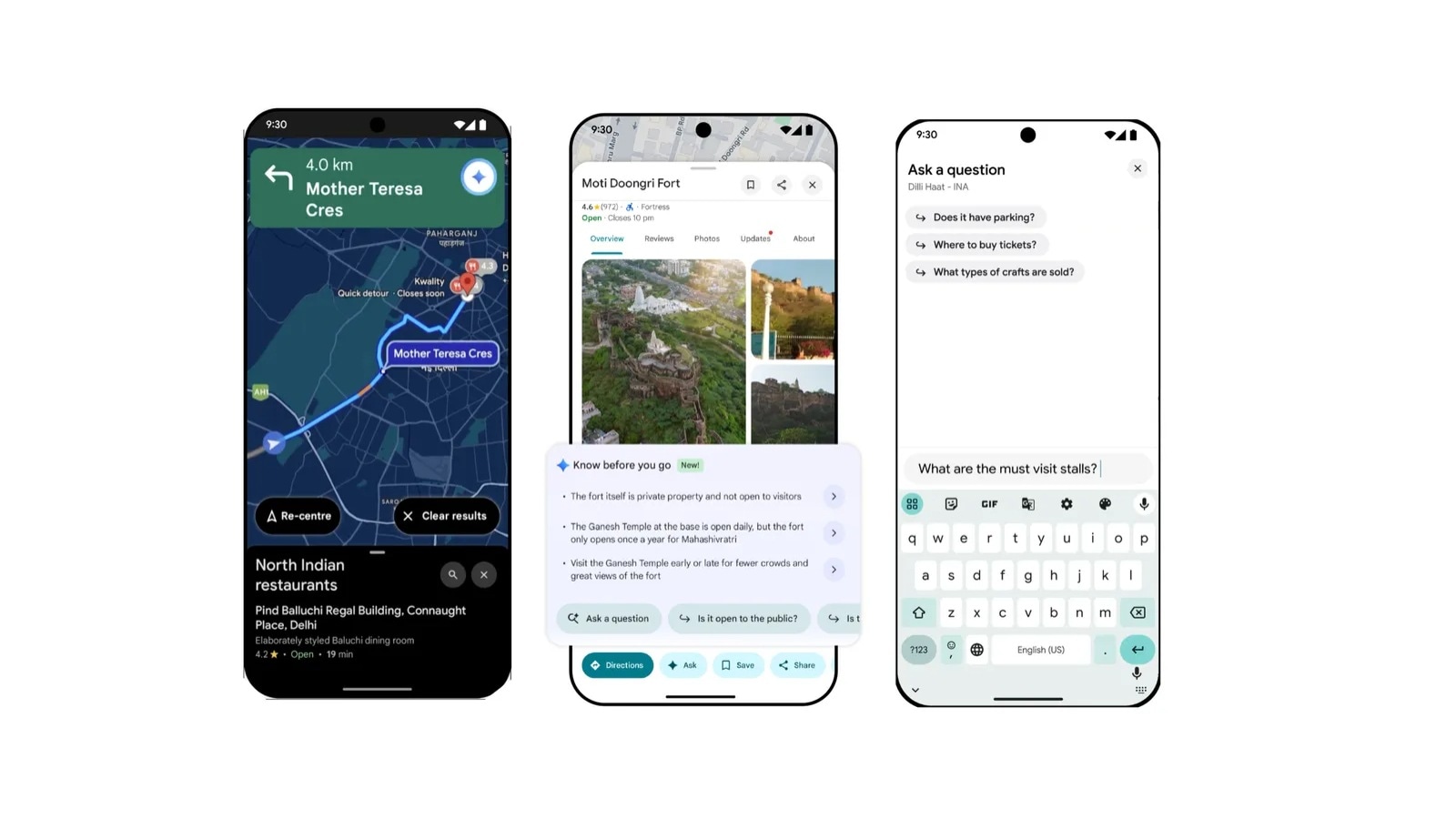

Alphabet has begun rolling out its Gemini AI integration across all Google Maps navigation modes in the U.S., using account-level language and voice preferences to provide contextual, follow-up answers and landmark-based directions. New capabilities include trip-related queries (restaurants, parking, EV chargers, petrol pumps), accident/obstacle reporting from drivers, and richer traffic alerts—features that could boost Maps engagement and utility for driving and multi-modal travel, though no revenue or monetization details were provided and the rollout remains geographically limited.

Market structure: Alphabet (GOOGL) is the clear direct beneficiary — Gemini-powered Maps increases on-device engagement, creates incremental local-ad inventory and upsell paths to Maps-based commerce (food, parking, EV charging). Expect a modest revenue uplift concentrated in local search/Maps ads: roughly 0.5–2% of ad revenue over 12–24 months if Google monetizes prompts; winners also include AMZN (local fulfilment partners) and mobile ad networks. Losers: pure-play map/data vendors (TomTom/TOMDF), legacy standalone GPS hardware (GRMN), and local ad aggregators (YELP) face margin pressure as Google internalizes discovery and transactions. Risk assessment: chief tail risks are regulatory/privacy enforcement (EU/US antitrust or GDPR-style fines up to low-single-digit % of revenue), safety litigation from navigation errors, and adoption drag if users reject voice hotwords. Immediate market moves likely muted; expect first monetization signals in 2–3 quarters and material global rollout impact in 6–12 months. Hidden dependencies include quality of map telemetry, EV charger data partnerships, and OEM agreements (Android Auto/CarPlay parity). Trade implications: tactically favor GOOGL exposure and trim names with direct mapping revenue risk. Consider 1–3% portfolio long GOOGL core position, add a 12–18 month LEAP call-spread 20–30% OTM to lever optionality while capping downside, and establish small short positions in TOMDF (or TOM2.AS) and underweight GRMN (0.5–1% each) as relative shorts. Time entries over the next 2–8 weeks to capture US rollout news and before global expansion announcements; take profits on positive monetization prints (target +20–30%) or cut at -10%. Contrarian angles: consensus underestimates regulatory/monetization friction — Maps enhancements may produce limited ARPU per-minute versus search, so market may be overpricing long-term ad upside. Historical parallel: Google’s Shopping integrations created dominance but also multi-year regulatory costs; here similar dynamics could cap net benefit. Watch for unintended consequences: higher liability, OEM pushback, or Apple (AAPL) accelerating paid Maps features, each of which could compress expected gains.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30