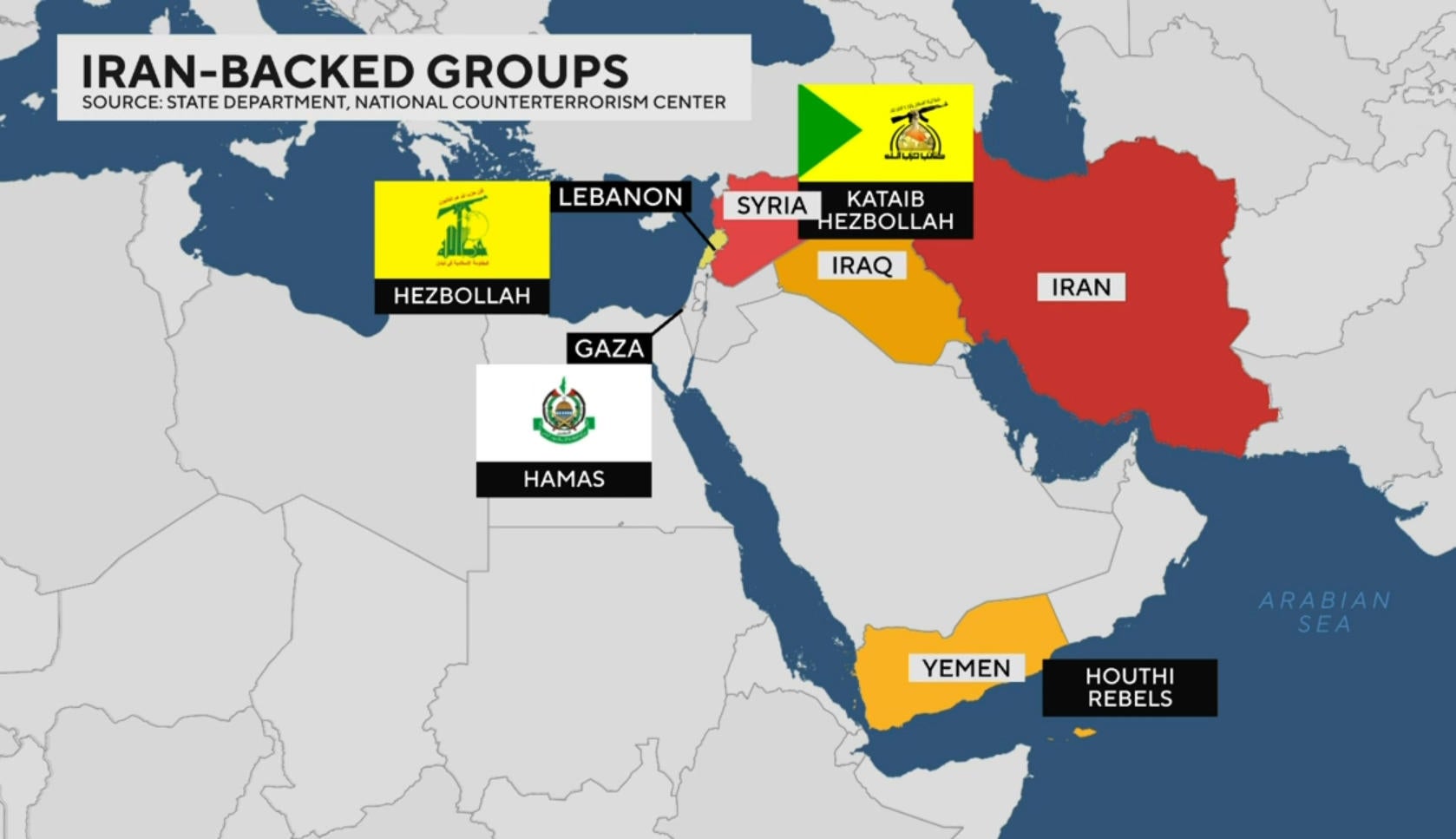

Oil rallied on renewed ceasefire uncertainty—US crude rose ~3.1% to $97.33/b and Brent climbed ~2% to around $98/b (oil roughly +40% since US/Israel launched the war on Iran). Asian equities softened (MSCI Asia ex-Japan -0.7%, South Korea -0.4%, China blue chips -0.6%), and US futures slipped, reflecting elevated risk-off positioning. Geopolitical risk remains elevated: Trump threatened large-scale attacks if Iran violates terms, Iran is enforcing transit protocols/alternative routes through the Strait of Hormuz, and Israeli-Hezbollah exchanges continue, increasing the risk of broader supply shocks. Maintain defensive positioning, monitor Strait transit disruptions and outcomes of the Islamabad talks for directional market moves.

Market prices are pricing a persistent Gulf risk premium driven by chokepoint friction, reinsurance repricing, and route dilation rather than a pure inventory shock; that amplifies energy producer margins and charter rates even if physical barrels remain near-term available via alternate logistics. Expect volatility to cluster in short windows around diplomatic updates — 48–72 hour spikes — with a second-order drag on global manufacturing and container throughput as rerouting adds 7–14 day transit slippage to schedules and raises bunker burn. Winners: upstream producers (rapid cash-flow capture), midstream/tankers (higher TCEs), and defense/intelligence suppliers that sell ISR and munitions sustainment. Losers: airlines and surface logistics operators facing higher fuel and insurance costs, EM importers with tight FX reserves, and refiners exposed to specific crude slates whose replacement grades cost materially more; note fertilizer and agro exporters are likely to see margin compression as freight and gas-linked feedstock costs rise. Tail risks are asymmetric: escalation to a de facto chokepoint closure or a major strike campaign produces a multi-week oil tail that can push Brent well above current risk premia, while a verified, rapid demining plus SPR/strategic diplomacy could erase the premium in 2–6 weeks. Monitor three binary catalysts on the horizon: (1) credible mine-clearance verification, (2) insured war-risk corridor reopenings and (3) SPR/strategic commercial releases — any one can collapse the risk premium quickly. Portfolio implication: bias short-duration, convex exposures to energy/defense and avoid long-duration cyclicals exposed to discretionary consumer travel and EM import bills. Size tactical option structures to capture directional spikes while using pair trades to neutralize macro beta and limit drawdowns if de-escalation occurs unexpectedly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.65

Ticker Sentiment