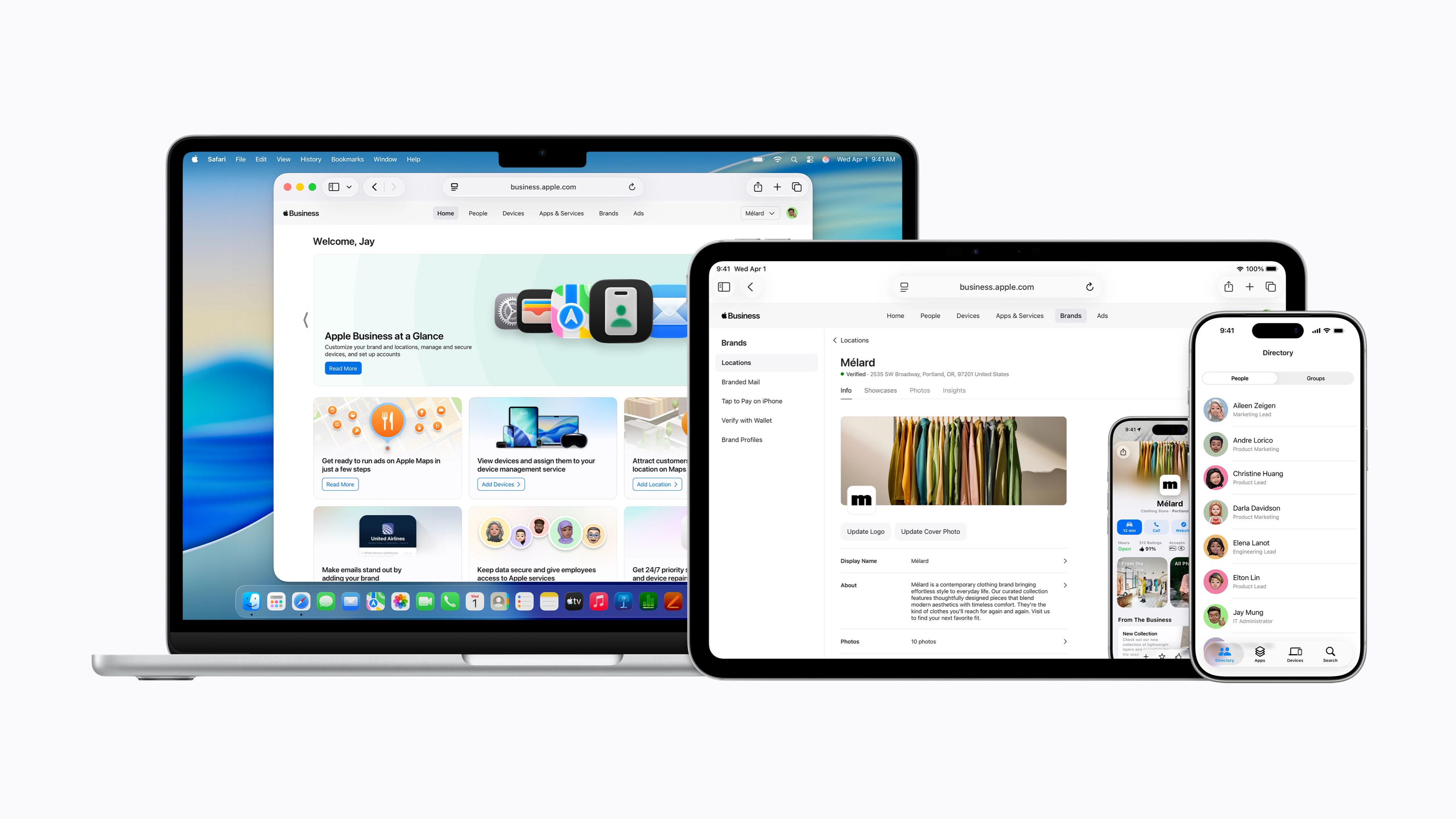

Apple launched its new unified Apple Business platform, consolidating Apple Business Essentials, Apple Business Manager, and Apple Business Connect into a single free service for businesses in over 200 countries and regions. The platform adds centralized MDM, zero-touch deployment via Blueprints, managed Apple Accounts, and branded customer-engagement tools, while monetization can come from optional storage, AppleCare+, and Maps ads. Apple is also discontinuing the legacy business products as the new portal and companion app roll out on iOS 26, iPadOS 26, and macOS 26.

This is less a “new product” story than a distribution and monetization consolidation play. By collapsing fragmented SMB/workplace tools into one surface, Apple should raise attach rates for paid storage, support, and device enrollment while lowering churn versus point solutions from smaller IT vendors. The bigger second-order effect is that Apple is moving up the stack from hardware monetization into recurring admin workflows, which increases switching costs for enterprises that have already standardized on iPhones and Macs.

The most important competitive consequence is pressure on endpoint management and SMB IT vendors that rely on Apple-adjacent workflows, not just on the enterprise suites Apple is replacing internally. Zero-touch provisioning plus identity integrations make the platform more “good enough” for mid-market customers that previously would have paid for third-party device management; that can compress pricing power across the long tail of Apple-focused MDM providers. On the ad side, local search inventory inside Maps is a higher-margin, incrementally underappreciated layer that could become a meaningful services contributor if Apple can prove intent quality, but launch scope is narrow enough that this is a 6-12 month test rather than a near-term revenue inflection.

The key risk is execution friction from OS gating and product migration: any enterprise rollout that forces upgrades can slow adoption for 1-2 quarters and create support noise, especially among conservative IT buyers. There is also a subtle privacy brand risk: bundling directory, comms, and ads into one enterprise-branded layer could trigger scrutiny if customers perceive a blurring between management tooling and advertising surfaces. If uptake is strong, the real upside is not Maps ads alone but higher ecosystem retention and a modest lift to services ARPU over 2-3 years.

Consensus may be underestimating how sticky this makes Apple in SMBs while overestimating the immediate ad monetization. The near-term P&L effect is likely small, but the strategic effect on lifetime value per device is meaningful because it deepens admin dependency without adding material complexity. That supports a slow-burn multiple argument for AAPL, especially if services growth re-accelerates without requiring hardware unit surprises.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.34

Ticker Sentiment