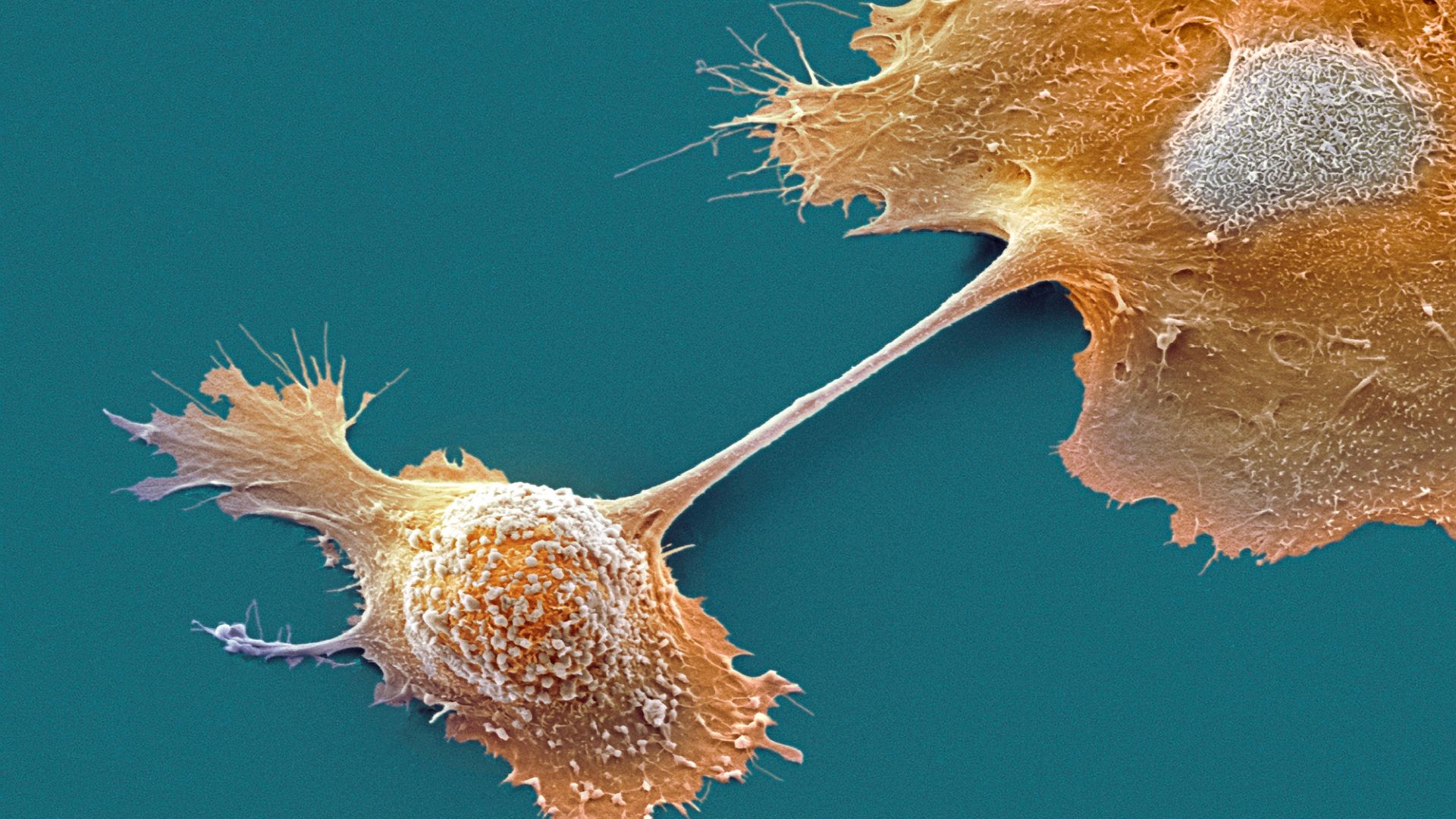

An experimental pancreatic cancer drug, elraglusib, doubled one-year survival to 42% versus 22% with chemotherapy alone in a randomized phase 2 trial of 286 patients. Median overall survival improved to 10.1 months from 7.2 months, though the treatment did not extend progression-free survival. The result is a meaningful clinical signal for advanced pancreatic cancer and could support further development or combination trials, but it is not yet a market-moving event.

This is a signal on mechanism-first oncology rather than a clean single-name catalyst. If the phase 2 result is reproducible, the biggest economic winner is not the drug asset alone but the broader “microenvironment-modulation” platform: it can extend the commercial life of chemotherapy backbones and potentially create combination optionality for checkpoint inhibitors and KRAS-targeted regimens that have struggled in pancreatic cancer. That shifts value toward companies with complementary assets, trial infrastructure, and enough capital to run rapid combination studies.

The second-order effect is competitive pressure on late-stage pancreatic programs that are built around incremental chemo optimization. A credible survival benefit with manageable safety increases the probability that future trial designs will need to include stromal / immune-penetration modifiers as a standard layer, which raises the bar for monotherapy readouts over the next 12–24 months. It also makes academic-origin assets more investable, because the bottleneck here appears to be tissue delivery and biology, not discovery novelty.

The contrarian read is that the market may over-interpret a survival win while underweighting the absence of progression-free benefit. That usually means the next phase of upside depends on better patient selection, longer exposure, or combination protocols — all of which are slower, more failure-prone, and likely to create a 6–18 month data gap after the initial enthusiasm. If subsequent studies fail to show an earlier disease-control signal, the asset can still be labeled a palliative survival add-on rather than a platform-defining breakthrough.

Near-term, this is more a catalyst for biotech sentiment and combo-therapy baskets than a direct tradable public-equity event. The relevant watchpoint is whether a larger partner steps in and whether the program broadens into tumor types where stromal barriers are also a binding constraint; if that happens, the valuation re-rate could be more about platform optionality than pancreatic cancer alone.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.72