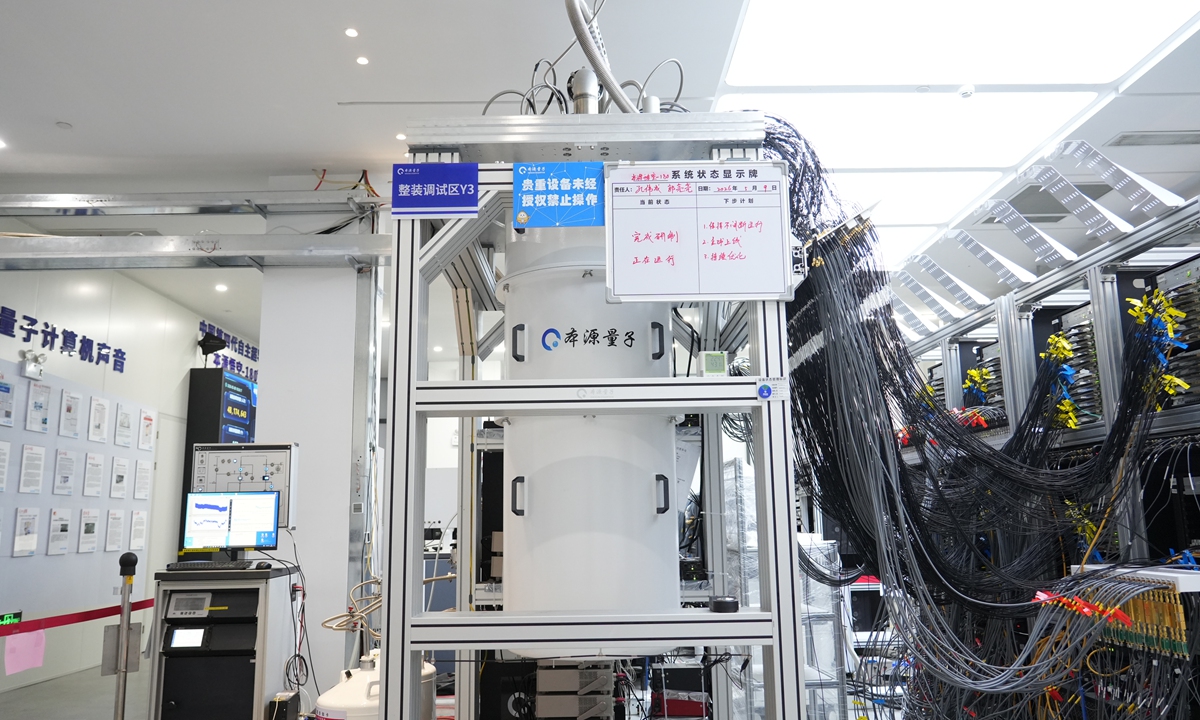

Origin Quantum's fourth-generation 'Origin Wukong-180' superconducting quantum computer is now online, featuring a single-core 180-qubit chip and 100-qubit-level computing capability under a single-chip architecture. The system's four core subsystems were independently developed, and it is now accepting quantum computing tasks globally, extending China's self-developed quantum computing stack further into AI applications. The update is strategically positive for the company and China's quantum computing ecosystem, though the immediate market impact is likely limited.

This is less a pure compute story than a state-backed ecosystem move: the important signal is not that one more quantum machine is online, but that China is now trying to industrialize access, tooling, and workflow integration around sovereign quantum capacity. That shifts the competitive battleground from qubit count to developer adoption, orchestration software, and API distribution, which should disproportionately benefit domestic quantum middleware, controls, and AI-infrastructure names rather than hardware alone.

The second-order effect is pressure on Western quantum incumbents and cloud platforms in the long run, but not because this machine is economically superior today. The near-term moat is actually on the supply side: measurement/control electronics, dilution refrigeration, cryogenic components, and quantum OS layers become the bottleneck, so any incremental demand will ripple into domestic hardware localization efforts. If China can demonstrate repeatable task throughput and low-latency access, it could compress the premium Western vendors get from being the only practical remote-access option for enterprises and universities.

The market is likely underestimating how much of this is an AI distribution play disguised as a quantum headline. The real catalyst over the next 6-12 months is whether quantum-AI tools move from demo to workflow embedment in enterprise tooling; if so, the value accrues to companies owning model orchestration, runtime, and task routing, not to raw quantum compute capacity. Conversely, if utilization is mostly symbolic or research-grade, the tradeable impact fades quickly and the stock of optimism will mean-revert.

Contrarian view: the consensus may be over-indexing on qubit count and underweighting error rates, job mix, and cost-per-solved-task. A larger chip with poor fidelity can actually slow adoption if it raises support complexity without improving useful quantum volume, so the execution risk is high and the time horizon to monetization is likely measured in years, not quarters. The better trade is to own the picks-and-shovels of AI/quantum workflow enablement while fading any broad read-through that China has achieved a commercially decisive quantum breakthrough.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55