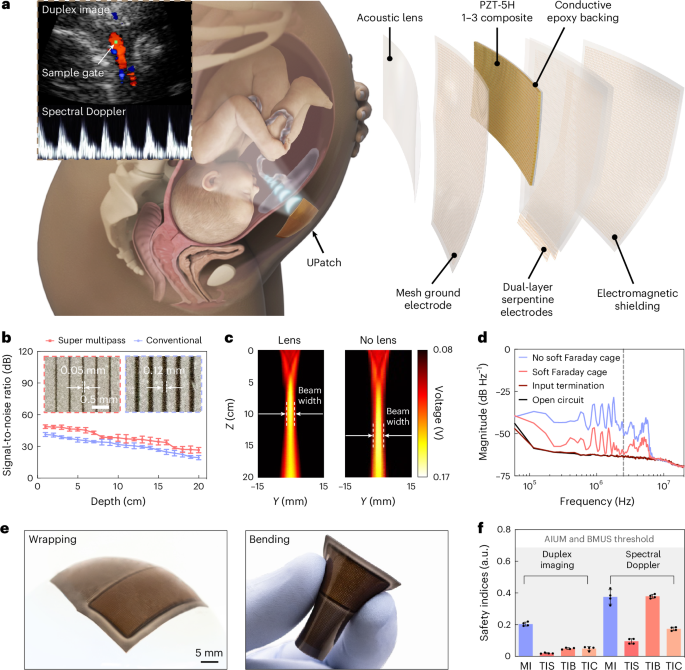

Researchers reported a wearable ultrasound patch (UPatch) that enables continuous, autonomous fetal monitoring and showed good agreement with a handheld clinical ultrasound device in 62 pregnancies. In continuous monitoring of 52 pregnant women, the system aligned with stratified perinatal conditions including healthy pregnancies and high-risk groups such as small for gestational age, large for gestational age, gestational diabetes, preeclampsia, and gestational hypertension. The technology could expand prenatal-care capabilities if further developed into a fully wireless system, but near-term market impact appears limited.

This is a classic enabling-technology read for GE Healthcare rather than an immediate revenue step-function. The near-term value is not in direct device displacement, but in legitimizing a new category where hospital-grade ultrasound shifts from episodic diagnostics to continuous monitoring; that expands the install base around probes, ultrasound carts, software, and workflow integration rather than cannibalizing it. In other words, the wedge is more likely to create incremental utilization and data services than to replace incumbent imaging capital spending. The second-order effect is a moat shift toward algorithmic tracking, signal processing, and regulatory integration. If autonomous fetal monitoring proves out, the differentiator becomes not transducer hardware alone but the ability to fuse imaging, motion compensation, and clinician-facing alerting into a validated workflow; that favors companies with existing regulatory, service, and distribution infrastructure. The likely losers are small, hardware-only wearables and point-solution fetal monitoring vendors that lack a path to reimbursement, QA, and clinical adoption at scale. The market may be underestimating the timeline to monetization. This is still early clinical validation, so the commercial inflection is measured in years, not quarters, and the main reversal risks are reimbursement ambiguity, maternal safety scrutiny, and false-alarm burden in high-risk pregnancies. A failure mode would be if the device works technically but cannot outperform existing Doppler/CTG pathways on triage efficiency, because then adoption stalls at tertiary centers rather than moving into routine prenatal care. Contrarian angle: the bigger opportunity may be adjacent to obstetrics, not directly in prenatal monitoring. Continuous ultrasound plus autonomous tracking is a platform capability that can spill into anesthesia, ICU, and ambulatory monitoring where motion tolerance and wireless form factors matter, which is a much larger TAM than the initial niche. If investors focus only on fetal care, they may miss the optionality in software-defined ultrasound workflows that can be reused across multiple clinical settings.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment