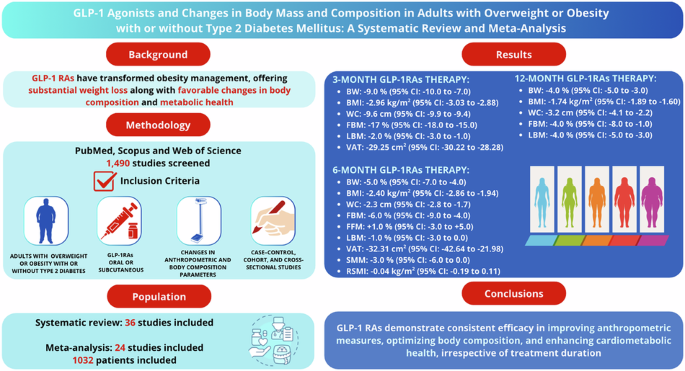

A systematic review/meta-analysis found GLP-1 receptor agonists and dual GLP-1/GIP agonists produced clinically meaningful weight loss in adults with overweight or obesity, with body weight falling about 9% at 3 months, 5% at 6 months, and 4% at 12 months. The benefit was driven mainly by fat mass and visceral adipose tissue reduction, while lean mass losses were modest relative to total weight loss. The study supports GLP-1 drugs as a high-conviction obesity treatment strategy, though efficacy varied by agent and duration.

The important takeaway is not simply that GLP-1s keep taking share; it is that the market is underestimating how quickly the category is moving from “weight-loss” into a chronic body-composition management platform. That broadens the addressable pool from discretionary obesity treatment into chronic disease maintenance, which should support longer duration, lower churn, and more durable prescribing volumes for the category leaders. The second-order winner is likely the drug class with the best persistence and tolerability profile, because the meta signal suggests the early weight-loss curve flattens over time, so retention becomes more valuable than headline efficacy.

The hidden margin implication is that mixed outcomes on lean mass create a built-in service opportunity for adjacent categories: protein supplementation, DEXA/BIA monitoring, digital coaching, and resistance-training-enabled obesity programs. If clinicians start layering these products to protect muscle, the economics of obesity care become more ecosystem-like, favoring companies that can bundle medication with monitoring and adherence tools. That is also a potential wedge for payers to demand outcomes-based contracts, which would pressure weaker agents and discount channels that cannot prove maintenance beyond the first 3-6 months.

From a trading standpoint, the biggest risk is a narrative reversal around “muscle loss” if larger real-world datasets show functional decline rather than just composition changes. That risk is not immediate over days; it is a 3-12 month catalyst set tied to payer coverage reviews, label updates, and clinician behavior shifts. Near term, the more likely market overreaction is still on the upside for best-in-class incretins, but the dispersion should widen between franchises with strong persistence data and those with weaker maintenance curves.

The contrarian view is that the broad obesity trade may be too crowded if investors are paying for peak prescription growth without enough scrutiny on discontinuation, step-therapy friction, and switching. If the class becomes commoditized, the economic rent migrates away from the molecule toward access, adherence, and support infrastructure. That argues for being selective: own the winners with ecosystem control, and fade names exposed to price competition or weaker long-dated persistence.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.30