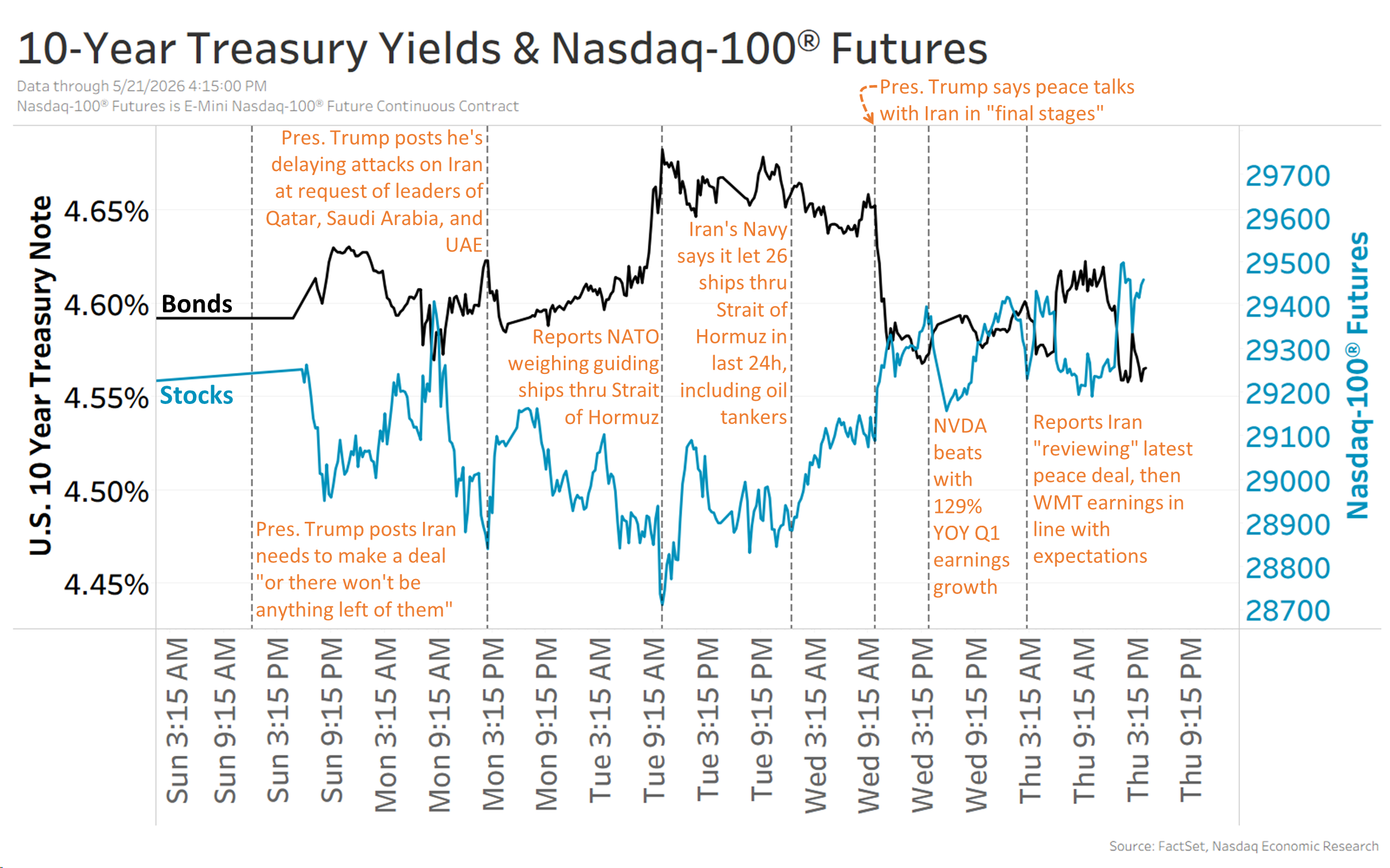

Iran-related de-escalation signals helped push U.S. oil prices back below $100 per barrel from nearly $110 on Tuesday, easing a key market risk. NVDA posted 129% year-over-year earnings growth with Q2 sales projected to nearly double, while WMT delivered 8% YOY growth but left guidance unchanged and flagged pressure from higher fuel prices. The Fed minutes still leaned hawkish on inflation, but markets are pricing rates to stay unchanged longer, with the Nasdaq-100 up 1% and 10-year Treasury yields at 4.55%.

The most important market implication is not the modest pullback in crude itself, but the repricing of tail risk across the entire inflation complex. If shipping lanes remain even partially open, the market will likely fade the headline premium in oil first; however, that still leaves a higher floor for delivered energy costs, which matters more for consumer discretionary margins and inflation breakevens than for headline WTI. The second-order winner is anything with pricing power and short-cycle inventory turns; the loser is the low-end consumer, where fuel acts like a tax and compresses baskets before labor data visibly weakens. NVDA’s post-earnings drift despite blowout growth is a tell that the bar has migrated from growth to durability of forward margins and supply-chain elasticity. In a market where geopolitics is pulling rates and energy in opposite directions, mega-cap duration trades can stall even on excellent prints because investors are now asking whether hyperscale capex can keep compounding if macro volatility widens. That makes semis a relative-quality story, but not an indiscriminate momentum one; names with the cleanest gross margin visibility should keep outperforming, while anything dependent on multiple expansion is vulnerable to a reset. The Fed’s reaction function is the real hidden catalyst. If fuel holds elevated for another 2-4 weeks, policymakers can tolerate slower growth but not a re-anchoring of inflation expectations, which raises the odds that rate cuts stay priced out longer than consensus currently expects. That setup is constructive for the dollar and short duration, but it also means the market may be underestimating how quickly risk assets can re-rate if diplomatic progress fades and energy spikes back through prior highs.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.15

Ticker Sentiment