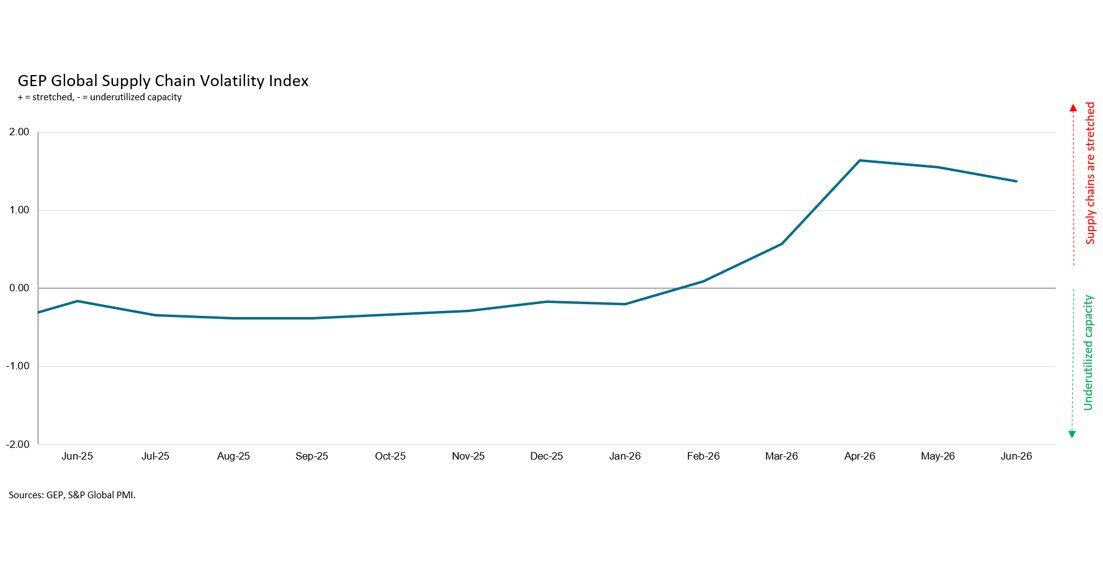

GEP’s Global Supply Chain Volatility Index showed supply-chain pressures staying elevated in June despite lower oil prices, with manufacturers reporting shortages/backlogs at the highest levels since late 2022. The index fell to 1.95 in Asia (from 2.96) and to 1.17 in North America (from 1.69), but businesses continued safety stockpiling—remaining at the highest level since Jan 2023—while European input demand weakened. Overall, the data points to continued bottlenecks into at least Q3 as companies buy raw materials/commodities ahead of expected further disruption.

The near-term read-through is better for upstream pricing power than for broad industrial earnings. When manufacturers rebuild buffers, the first beneficiaries are commodities, specialty chemicals, packaging, and freight expedites; the hidden loser is anyone carrying low inventory turns and fixed-price delivery commitments, because working-capital intensity rises before revenue does. Europe looks like the weak link: retrenchment there argues for a continuing relative-growth gap versus North America/Asia rather than a clean global reflation trade.

The bigger second-order effect is that stockpiling pulls demand forward. That supports volumes into late Q3, but it also raises the odds of a demand air pocket in Q4 if lead times normalize and procurement managers unwind buffers. If the underlying shortage gauge keeps falling while transport costs stay subdued, the market should fade the inflation narrative and rotate from commodity beta toward quality/cash-flow names.

SPGI is a modest winner only insofar as its data products look more valuable in a volatile regime; the P&L impact is likely incremental, not thesis-changing. The contrarian view is that the market may overestimate how bullish this is for cyclicals: elevated backlogs can look like demand strength, but if they are mostly supply-constrained, margins can still compress via premium freight, overtime, and expediting even as reported orders hold up. The thesis breaks if the next monthly read shows a sharp drop in shortages/backlogs or if companies explicitly guide inventory destocking and lower purchase orders.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment