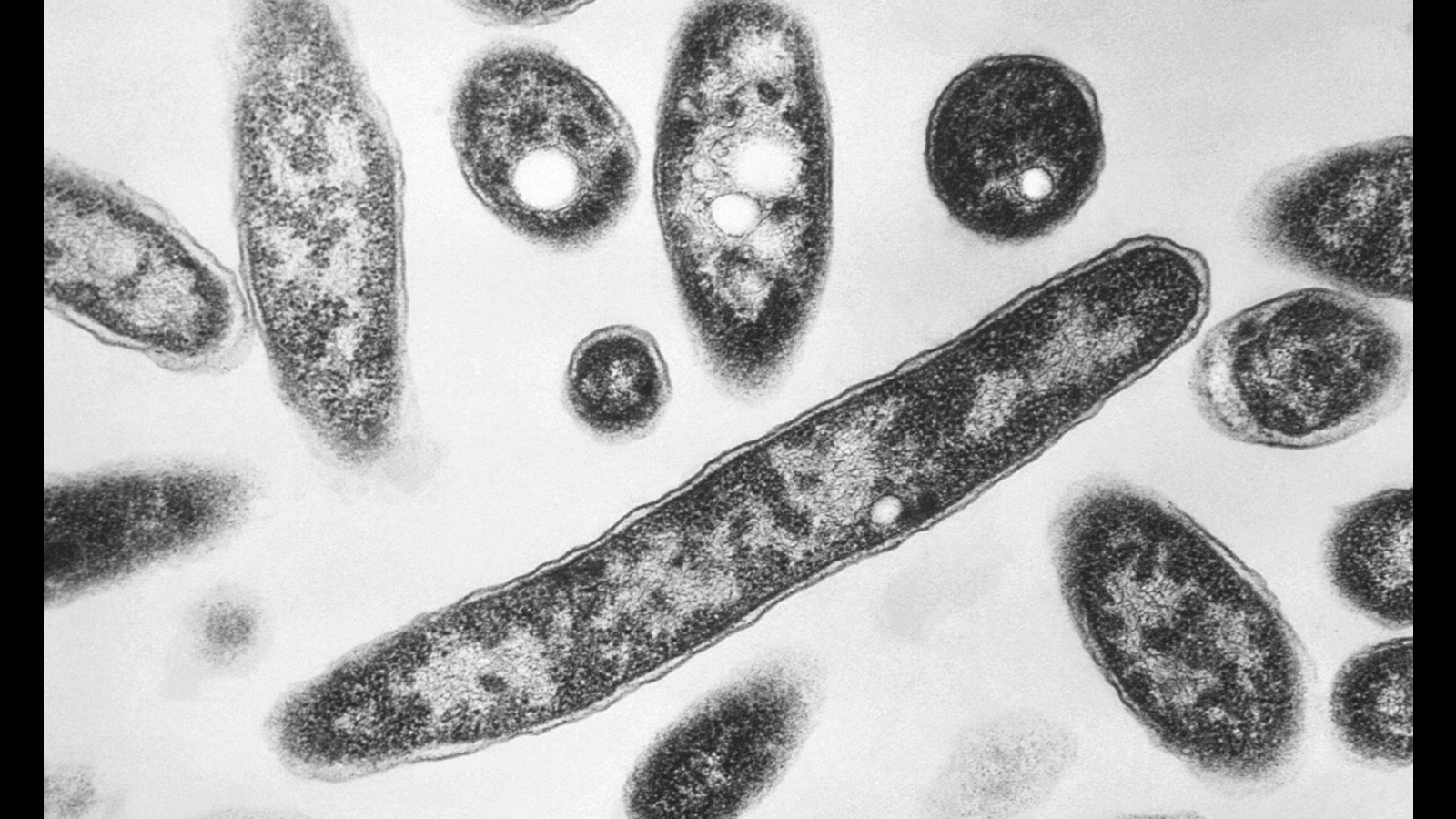

North Carolina reported 310 Legionnaires' disease cases in 2025, up from 201 cases in 2024, underscoring a worsening public health issue. Officials are urging residents, businesses, and health care facilities to increase water-system maintenance and prevention measures to limit Legionella growth. The article is informational and health-focused, with limited direct market impact.

This is not a “health scare” trade so much as a slow-burn compliance and capex story. Rising Legionella incidence tends to surface latent underinvestment in water management across commercial real estate, hospitals, senior housing, hotels, and municipal systems, which can create a multi-quarter wave of remediation spend even if headline case counts eventually flatten. The first-order economic winners are firms selling monitoring, filtration, disinfection, and building-water maintenance services; the losers are asset owners with older mechanical systems facing inspection, retrofit, and liability costs.

The second-order risk is legal rather than clinical: once a building is linked to an outbreak, reputational damage and tenant churn can outweigh the direct repair bill. That creates a skewed payoff for insurers and REITs with exposure to older urban assets, especially healthcare-adjacent and hospitality properties where water systems are complex and utilization is high. A modest uptick in cases is enough to keep property managers in “check-and-spend” mode, which is constructive for recurring-revenue service providers even if it is not yet visible in top-line guidance.

This is likely a months-long theme, not a days-long headline. The real catalyst is a major cluster tied to a recognizable venue class—hotel, nursing facility, or hospital—which would accelerate municipal scrutiny and trigger broader building-code enforcement. Conversely, a mild winter, lower cooling-tower usage, or aggressive local remediation could cap the upside quickly, so the trade should be expressed in names with recurring inspection demand rather than pure event-driven outbreak beneficiaries.

The contrarian view is that the market may overestimate the breadth of the economic impact. Most of the spend is defensive maintenance that is already budgeted, and many public health headlines fade before they affect occupancy or travel demand. The best setup is therefore not a macro short on “health fears,” but a relative-value long in water-treatment/compliance service providers versus exposed property or municipal maintenance budgets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.20