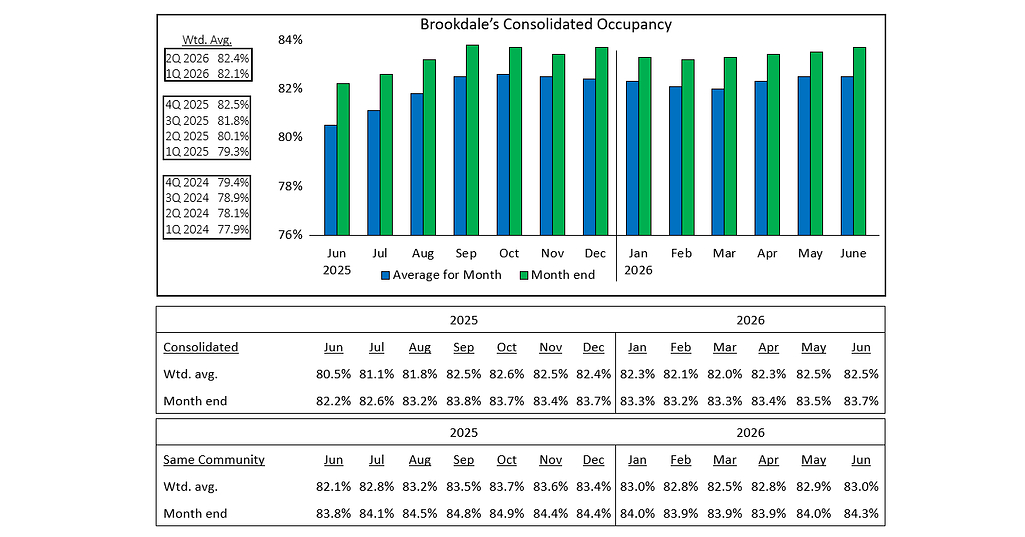

Brookdale Senior Living (BKD) reported June 2026 occupancy as well as Q2 2026 occupancy observations. The article provides no specific occupancy figures or changes versus prior periods, so there is limited incremental information for near-term trading impact.

This is a low-signal update for BKD unless the occupancy trend is accompanied by net price realization and lower concessions. In senior housing, occupancy only matters economically when it absorbs fixed rent, food, and labor overhead; otherwise operators can “buy” census with discounts and erase the EBITDA benefit. The market should therefore focus less on the occupancy print itself and more on whether next quarter’s same-store margin and net move-in mix confirm operating leverage. For competitors and capital providers, the second-order read-through is about pricing discipline. If Brookdale is filling beds via aggressive incentives, that can pressure smaller operators and delay a broader recovery in industry rate growth, which matters more for REIT landlords like WELL, VTR, and NHI than for a single operator headline. If instead occupancy is improving without a concession step-up, BKD has outsized equity torque given its leverage, but that thesis needs verification at earnings, not on a monthly release. The contrarian view is that investors often overpay for any occupancy improvement in this space because the lag from census gains to cash flow is long and noisy. The key falsifier is margin: if next reported quarter shows occupancy up but labor inflation, agency staffing, or move-in incentives keep adjusted EBITDA flat, the stock should not re-rate. Near term, this is more of a watch item than a trade catalyst.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment