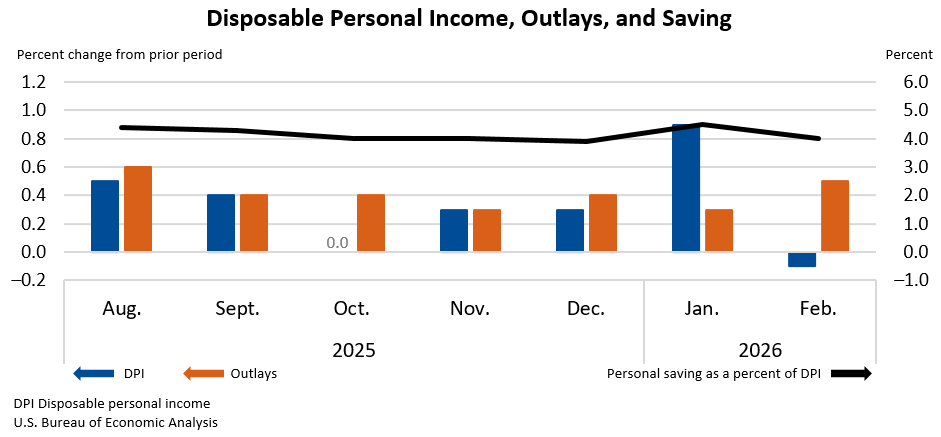

Personal income fell $18.2B (-0.1% m/m) in February 2026 and disposable personal income fell $18.3B (-0.1%). PCE rose $103.2B (+0.5% m/m), split $58.7B goods and $44.5B services, with real PCE up $17.3B (+0.1% m/m). The PCE price index rose 0.4% m/m and 2.8% y/y (core +0.4% m/m, +3.0% y/y); personal saving was $931.5B and the saving rate was 4.0%.

Household cashflow deterioration alongside still-elevated service inflation creates a two-speed consumer: essentials and price-insensitive services hold up while discretionary, especially aspirational and big-ticket categories, face growing strain. That bifurcation boosts demand for value-oriented retail, tightens margins for branded consumer goods, and lengthens working capital cycles as inventories are rebalanced toward lower-margin SKUs. Sticky services inflation materially raises the odds the policy rate stays higher for longer than current market-implied cuts and compresses duration-sensitive asset returns; banks and insurers pick up incremental NIM and float income, while long-duration credits and growth equities become more vulnerable to multiple compression. The BEA’s continued source-data adjustments for hard-to-measure services highlights upside risk to reported inflation surprises coming from the services complex. Second-order supply effects: manufacturers facing weaker discretionary orders will push procurement later into the cycle, benefiting industrials with flexible production and warehousing exposure but hurting just-in-time suppliers; logistics providers that cater to e-commerce value channels should see relatively stable volumes. On the credit side, card issuers will enjoy fee and rate income in the near term but face higher loss provisioning 6–12 months out if wage momentum doesn’t re-accelerate. Key catalysts to watch are incoming payrolls and next two PCE prints (and Fed communications) — a stronger wage/CPI combo would force a repricing of rate-cut expectations and widen spreads; conversely, a clear income rebound would unwind consumer-credit stress narratives and re-rate discretionary risk assets. Tail risks include a faster-than-expected drop in services inflation (technology-driven or regulatory), or a sudden deterioration in consumer credit metrics triggered by regional labor shocks, either of which would reverse multiple skews quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00