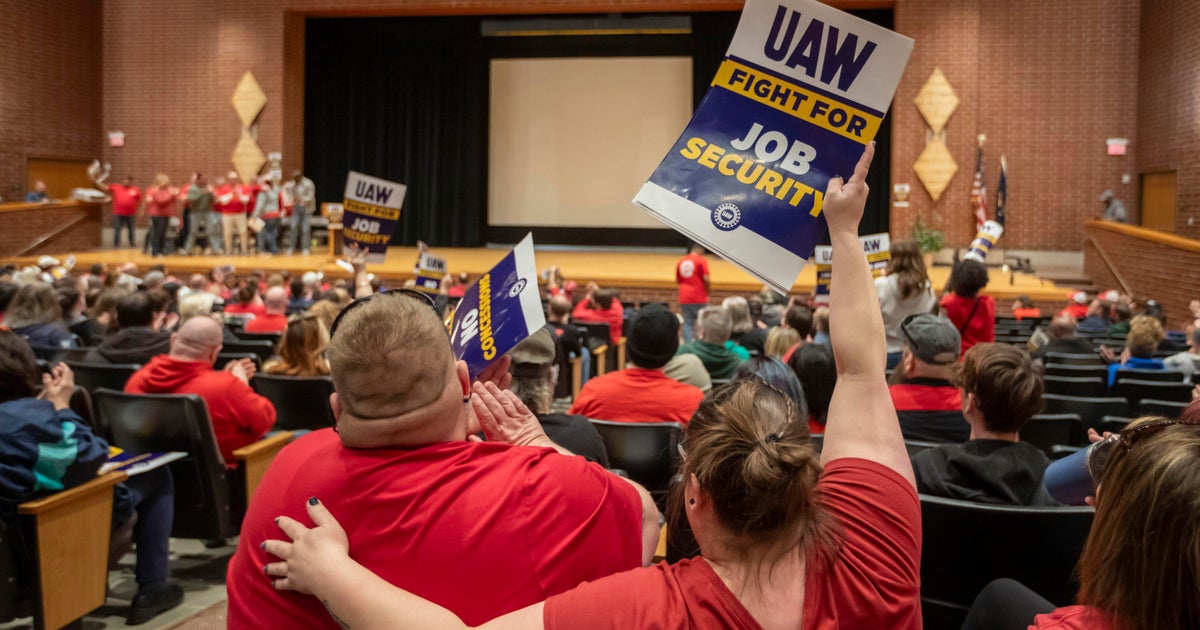

UAW Local 2093 began a strike at American Axle's Three Rivers, Michigan plant at 12:01 a.m. Monday after contracts expired May 31. The union is seeking to restore wages that were cut from as much as $29 an hour in 2008 to $14.50 and now top out at $22 after a five-year progression. The strike creates near-term operational risk for American Axle, a Tier 1 supplier to General Motors, but the news is likely company-specific rather than market-wide.

This is less a GM story than a margin-propagation event for the automotive supply chain. A strike at a Tier 1 axle supplier can create a disproportionate headache for OEMs because low-inventory assembly lines are optimized for continuity, not resilience; even a modest disruption can force temporary build-rate cuts, premium freight, or expedited dual-sourcing, all of which pressure gross margin before headline production numbers move. The market likely underestimates how quickly a localized labor stoppage can spill into sequencing risk for GM programs that depend on just-in-time drivetrain components.

The key second-order effect is bargaining leverage. If American Axle secures materially better wage outcomes, it becomes a reference point for other legacy auto suppliers where wage compression has been normalized for years. That matters because supplier labor is already tight and tooling-intensive businesses have limited room to absorb higher labor costs; any successful reset tends to show up with a lag in supplier quotes, then OEM pricing, then lower unit margins across the chain over the next 1-3 quarters.

For GM, the near-term risk is not direct earnings loss from this specific facility, but operational friction and a more expensive supplier base. The bigger catalyst to watch is duration: a strike measured in days is noise; one that extends into weeks raises the odds of inventory depletion, plant downtime, and negative read-through on supplier labor negotiations elsewhere. If mediation produces a quick settlement, the market may fade the issue, but if the union gets meaningful wage restoration, it strengthens the case for a broader cost reset across North American auto inputs.

Contrarian angle: the equity market may already be too relaxed about supplier labor as a one-off. The real vulnerability is not headline union noise, but the possibility that this becomes the template for multiple small contracts rolling over in a high-inflation wage environment. In that scenario, OEMs and suppliers face a slow but persistent margin squeeze that is harder to model than a clean strike shock, and therefore easier to miss.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35

Ticker Sentiment