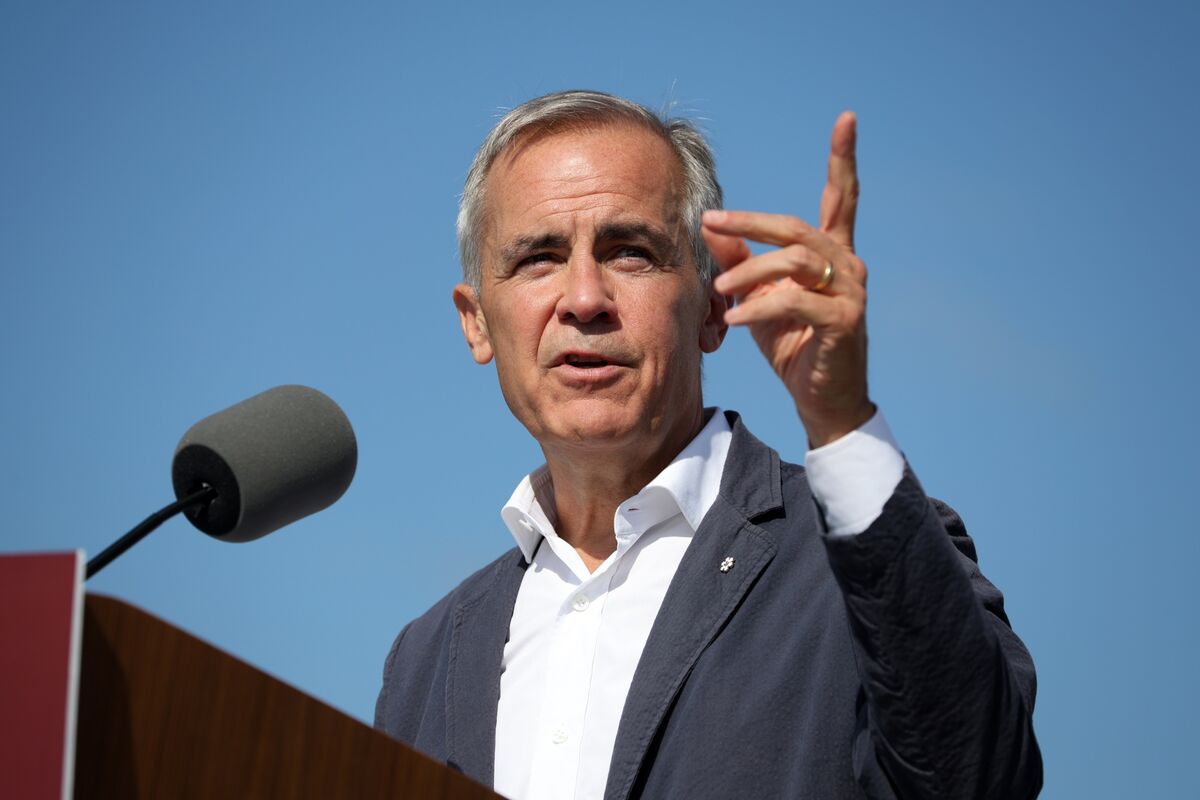

Canadian Prime Minister Mark Carney is urging Western allies to swiftly impose secondary sanctions on Russia to significantly increase pressure on President Putin. Carney has personally advocated for these measures in discussions with allies, deeming it possible that the Trump administration and European countries will eventually adopt them, indicating a potential escalation in economic strategies against Russia.

Canadian Prime Minister Mark Carney is actively advocating for the swift imposition of secondary sanctions on Russia, a move that would represent a significant escalation of economic pressure. His statement, which carries a hawkish tone, indicates he has personally pushed for this policy in discussions with allies, including the Trump administration and European nations. The assessment that such measures are "possible" elevates this beyond mere rhetoric, introducing a tangible geopolitical risk with a moderately high market impact potential. Unlike primary sanctions, secondary sanctions would target third-party entities conducting business with Russia, threatening to create broader disruptions in global trade and finance and significantly increasing pressure on President Putin's government.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately negative

Sentiment Score

-0.50