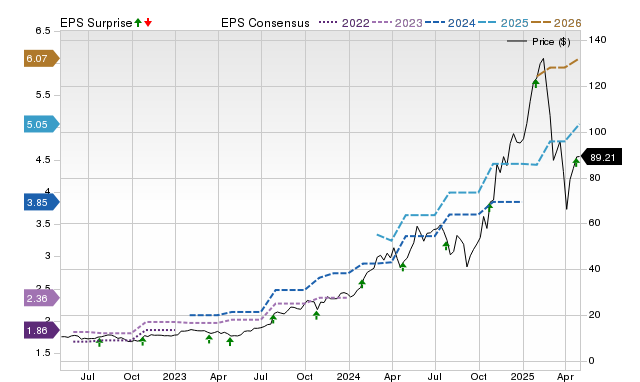

Celestica (CLS) is anticipated to report robust Q2 2025 results on July 28, with consensus estimates projecting EPS of $1.24, a 36.3% year-over-year increase, on revenues of $2.65 billion, up 11% year-over-year. The company holds a positive Zacks Earnings ESP of +0.81% and a Zacks Rank #2 (Buy), a combination that strongly indicates Celestica is highly likely to surpass consensus EPS estimates, consistent with its record of beating expectations in three of the last four quarters. This outlook positions Celestica as a compelling earnings-beat candidate, potentially influencing its near-term stock performance.

Celestica (CLS) is approaching its Q2 2025 earnings report with strong growth expectations, as consensus estimates project an 11% year-over-year revenue increase to $2.65 billion and a 36.3% rise in EPS to $1.24. Quantitative indicators suggest a high probability that the company will surpass these estimates. Specifically, Celestica holds a positive Zacks Earnings ESP of +0.81%, indicating that the most recent analyst estimates are more bullish than the standing consensus. This, combined with a Zacks Rank of #2 (Buy), creates a scenario that has historically preceded an earnings beat nearly 70% of the time. This positive outlook is further supported by the company's track record of exceeding EPS estimates in three of the last four quarters, including an 8.11% surprise in the most recent period. While the consensus estimate has remained unchanged over the last 30 days, the positive ESP implies that the latest analyst revisions reflect improving business conditions. The ultimate sustainability of any post-earnings stock movement will, however, heavily depend on management's forward-looking guidance and commentary during the earnings call.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment