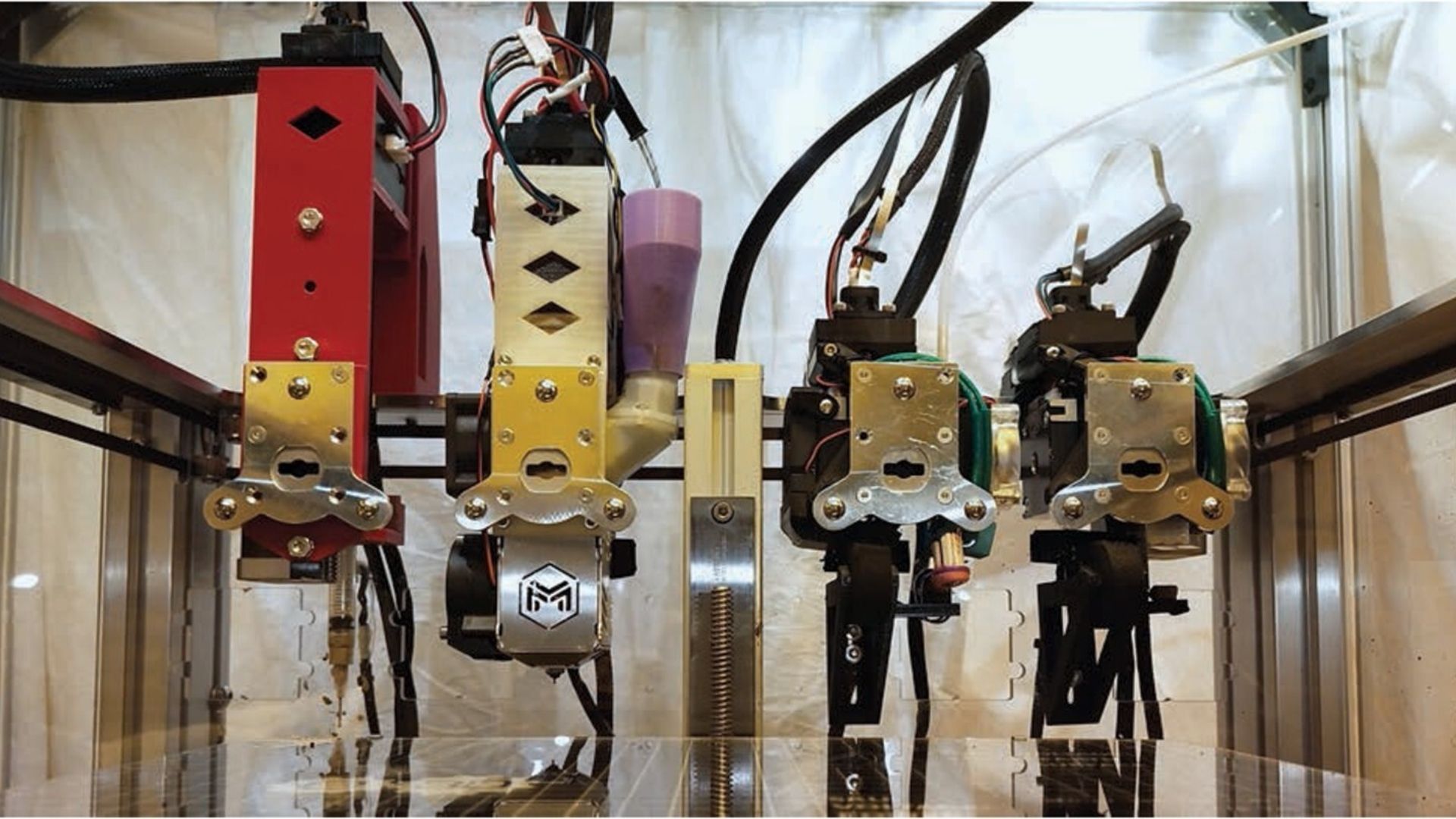

MIT researchers developed a multi-extruder 3D printer that can produce a fully functional linear electric motor in about three hours using five material types (dielectric, conductive, soft magnetic, hard magnetic, flexible), requiring only post-print magnetization. The printed motor reportedly matches or exceeds traditionally manufactured equivalents while costing roughly $0.50 in materials and reducing prototype lead times from weeks or months to a day, implying potential to localize spare-part production and reduce reliance on global supply chains — a disruptive, though early-stage, efficiency and cost signal for manufacturers and supply-chain exposed firms.

Market structure: Multimaterial, multi-extruder printing lowers fixed-cost barrier for custom electric motors and niche legacy-replacement parts; winners are 3D-print hardware/software suppliers (SSYS, DDD, DM, HPQ, PRLB) and specialty feedstock/ink providers that can scale formulations for conductive and magnetic materials. Incumbent high-volume motor manufacturers (e.g., Nidec, RRX, BWA) face limited near-term revenue risk because mass production economics still favor stamping/winding at >10k units, but pricing power on prototypes, aftermarket spares, and defense/remote operations can shift within 2–5 years. Risk assessment: Tail risks include IP wars (rapid patent filings), product-safety/regulatory bans in safety-critical systems, and supply-side concentration of magnetic inks; a single high-profile failure could stall adoption for 12+ months. Near-term (0–6 months) adoption is pilot-driven; short-to-mid (6–24 months) will see enterprise pilots and service-provider uptake; long-term (2–7 years) could enable local manufacturing hubs and meaningfully reduce lead times/costs for low-to-mid volume engines. Trade implications: Tilt overweight to pure-play AM hardware and materials with proven multi-material capability (SSYS, DDD, DM, PRLB) and software IP; hedge with selective shorts in aftermarket-bearing, low-margin motor suppliers exposed to replacement-part erosion (small-cap vendors and non-diversified EMS). Use options to express convexity around catalysts (pilot wins, patents, OEM qualifications) in the 3–12 month window. Contrarian angle: Market underestimates service-layer monetization—on-demand printing networks and consumables could be high-margin SaaS/recurring-revenue plays; conversely, the hype may be overdone if thermal/mechanical longevity limits applications, leaving winners as materials licensors and print-farm operators rather than printer OEMs. Historical parallel: desktop CNC/printing waves where hardware commoditized and materials/software captured margins within 3–6 years.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.35